Definition and Purpose of the Tax Appeals Department of Revenue

The Tax Appeals Department of Revenue plays a crucial role for taxpayers seeking to dispute assessments or decisions made by their state's Department of Revenue. It serves as a formal mechanism for individuals and businesses to challenge perceived inaccuracies or injustices in their tax assessments. This department is integral in ensuring that taxpayers have a fair opportunity to present their case, with the ultimate goal of achieving a resolution that considers both legal standards and individual circumstances.

Tax appeals are particularly relevant in situations where taxpayers believe there has been a misinterpretation of tax laws, incorrect valuations, or errors in calculations impacting their tax liabilities. The department's role is to review such appeals comprehensively, taking into account all relevant laws, evidence presented by the taxpayer, and preceding case laws. Understanding this department's function is essential for taxpayers seeking redress in their tax matters, ensuring their rights are preserved within the tax adjudication process.

How to Use the Tax Appeals Department of Revenue

To effectively use the Tax Appeals Department of Revenue, understanding the procedural framework is key. Begin by identifying the specific issue or decision you wish to contest. This could range from disagreements over assessed income, deductions denied, or penalties imposed. It's important to gather all relevant documentation that supports your position, such as tax returns, assessment notices, and any correspondence with tax authorities.

-

Initiate a Petition: Contact the department to acquire the necessary forms to file an appeal. This often includes completing a petition form and providing a detailed explanation of your appeal's basis.

-

Provide Documentation: Compile and submit supporting evidence that substantiates your claims. This might include financial records, prior tax filings, or expert valuations, depending on the nature of the appeal.

-

Attend Hearings: Be prepared for hearings or meetings where you'll present your case. This interaction allows for the clarification of points and the direct submission of evidence.

By following these steps, taxpayers can navigate the Tax Appeals Department effectively, ensuring their appeals are heard in a structured and fair manner.

Steps to Complete the Tax Appeals Department Form

Having the correct form and completing it accurately is foundational when dealing with the Tax Appeals Department of Revenue. Here is a structured approach to ensure completeness and correctness.

-

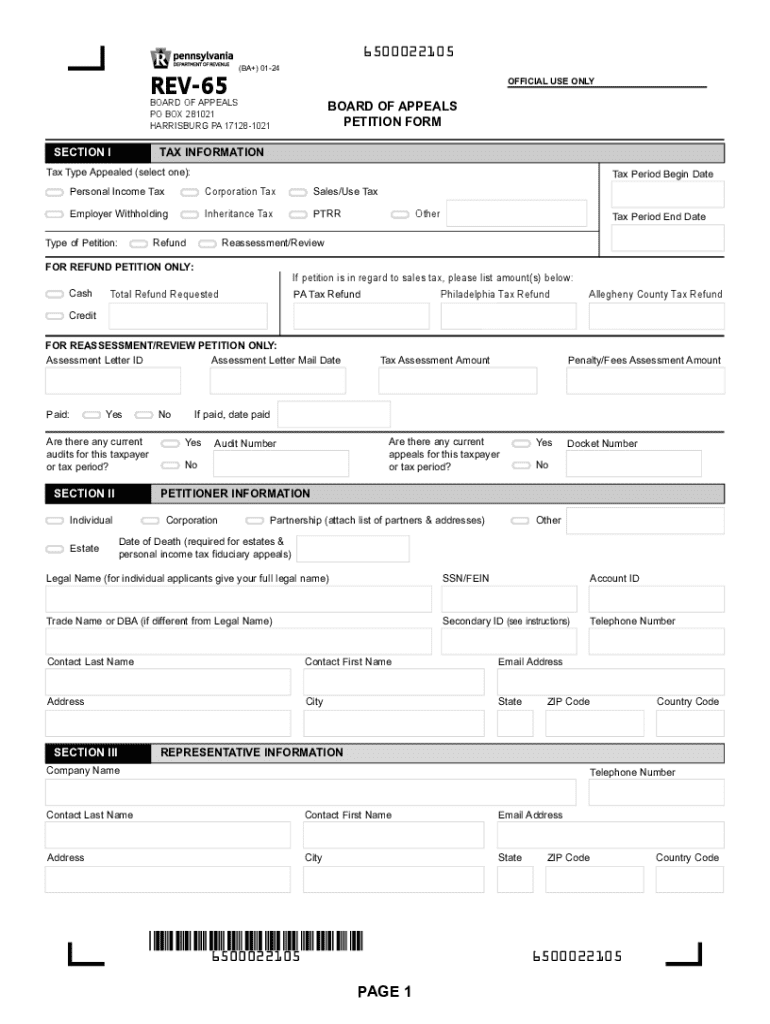

Download the Form: Access the Tax Appeals Department's official website to locate and download the appropriate petition form, often labeled with its unique number, like REV-65 in Pennsylvania.

-

Fill in Personal Information: Provide your personal or business details, ensuring all entries are accurate and correspond exactly to those on your tax documents.

-

Specify the Tax Type and Dispute: Clearly indicate the type of tax involved—such as personal income, corporation, or sales tax—and provide a concise summary of the issue.

-

Attach Supporting Documents: Include all relevant documentation that backs your claim. Make sure these documents are organized and labeled for easy reference.

-

Review for Accuracy: Double-check all filled sections for accuracy to avoid processing delays or rejection.

-

Submit the Form: Depending on the department’s preference, submit the completed form either online, via mail, or in person.

By following this process, you ensure a smooth, efficient submission of your appeal, increasing the likelihood of a favorable and expedited review.

Key Elements of the Tax Appeals Department of Revenue

Several critical components form the framework of the Tax Appeals Department of Revenue, affecting how appeals are processed and resolved.

-

Dispute Details: Clearly articulating the nature of the dispute is crucial, as it guides the department’s focus during investigations or hearings.

-

Documentation Support: The strength of the appeal often hinges on the quality and relevance of the supporting documents provided.

-

Legal Precedents: Understanding previous decisions and legal standards helps in framing arguments that are consistent with established law.

-

Deadline Adherence: Meeting all deadlines for submissions, hearings, or additional requests is vital to maintaining the appeal’s validity and momentum.

Navigating through these elements requires attention and precision, underscoring the need for thorough preparation and knowledge of procedural requirements.

Eligibility Criteria for Filing Appeals

Not all disputes qualify for adjudication by the Tax Appeals Department. Eligibility typically rests on several criteria that taxpayers need to assess before filing.

-

Filing Timeliness: Appeals must be filed within specific time frames post-assessment, which varies by state and tax type.

-

Standing: The taxpayer must have standing, meaning they must be the direct party affected by the tax decision or assessment.

-

Nature of Dispute: Only specific types of disputes are eligible, aligning with the legal definitions of an appealable decision by tax authorities.

-

Completeness of Tax Filing: Sometimes, the taxpayer must have complied with initial filing requirements to qualify for an appeal.

Understanding these eligibility parameters ensures that taxpayers do not expend time and resources on appeals that are unlikely to proceed.

Required Documents for Tax Appeals

Filing a successful appeal often depends heavily on the documentation provided. The specificity and completeness of documents can influence the outcome significantly.

-

Copy of Tax Returns: The most recent tax filings related to the dispute.

-

Assessment Notices: Official documentation from the tax authority detailing the contested decision or assessment.

-

Correspondence: Any communication between the taxpayer and tax authority, providing context and background.

-

Financial Records: These could include income statements, invoices, or receipts that provide evidence supporting the taxpayer's claim.

-

Expert Reports: Evaluations or reports from financial experts or appraisers relevant to the case.

Providing a comprehensive suite of documentation can significantly enhance the credibility of the appeal, facilitating a more favorable judgment.

Form Submission Methods for the Tax Appeals Department of Revenue

Taxpayers can typically submit their appeals using several modes, providing flexibility in catering to different preferences.

-

Online Submission: Increasingly the preferred route, online platforms allow for quick and trackable form submissions.

-

Mail Submission: Submitting via mail remains a viable option, particularly for those who prefer to keep physical copies or lack internet access.

-

In-Person: For more personalized encounters or complex cases, in-person submissions can offer opportunities for immediate feedback or document verification.

Selecting the best submission method depends on the taxpayer’s circumstances and the intricacies of the dispute they are presenting.

Penalties for Non-Compliance with Tax Appeals Procedures

Failure to adhere to the procedural mandates of tax appeals can result in several ramifications for taxpayers:

-

Dismissal of Appeal: Not meeting submission deadlines or requirements can lead to immediate dismissal, forfeiting any chance of redress.

-

Additional Fines or Penalties: Some jurisdictions might impose further financial penalties for submitting frivolous or incomplete appeals.

-

Increased Liability: Without successful appeal resolution, taxpayers may face increased liabilities reflecting the initial assessment.

Understanding these potential penalties underscores the importance of diligent preparation and compliance when filing tax appeals.