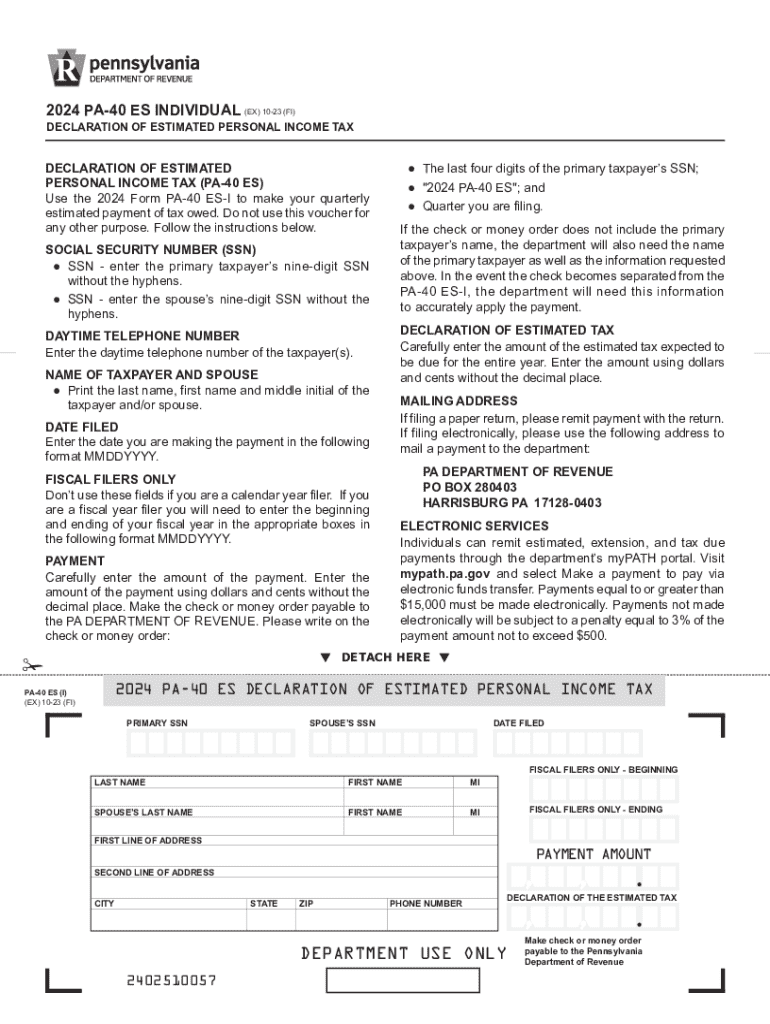

Definition and Meaning

The Declaration of Estimated Personal Income Tax is a crucial document used by taxpayers in the United States to report and submit quarterly estimated tax payments to the government. This form is typically used by individuals who expect to owe at least $1,000 in taxes after subtracting withholding and credits. By providing an estimate of the income tax a person is liable for in a given year, the form helps taxpayers avoid underpayment penalties and ensure compliance with federal and state tax obligations.

How to Use the Declaration of Estimated Personal Income Tax

Taxpayers must carefully fill out the form by estimating their expected income, deductions, and credits for the fiscal year. Here are the steps to utilize the form effectively:

- Estimate your income: Consider all possible income sources, including wages, dividends, and capital gains.

- Deduct eligible expenses: Account for allowable deductions such as retirement contributions, mortgage interest, and medical expenses.

- Calculate tax credits: Identify applicable tax credits like education credits and energy-saving improvements.

- Determine payment amounts: Subtract estimated deductions and credits from the total income to determine the taxable income and compute the estimated tax payable.

By accurately estimating these figures, taxpayers can decide on the appropriate amounts to submit as quarterly payments to meet their tax obligations.

Steps to Complete the Declaration of Estimated Personal Income Tax

Completing the declaration involves several steps. Here's a comprehensive procedure:

- Gather Required Documents: Collect previous tax returns, pay stubs, and other financial statements to estimate income accurately.

- Fill Out Personal Information: Start with providing personal details like name, address, and Social Security number.

- Estimate Income and Deductions: Use financial records to project both income and potential deductions for the year.

- Calculate Total Tax Liability: Apply current tax rates to estimate the total tax obligation.

- Divide Estimated Payments: Break down the total estimated tax into four equal quarterly payments.

- Submit Payments: Use chosen methods to submit payments, ensuring timely compliance with deadlines.

It's crucial to keep track of these steps and maintain copies of all relevant documents for future reference or audits.

Filing Deadlines and Important Dates

Taxpayers need to be aware of the crucial deadlines associated with the Declaration of Estimated Personal Income Tax:

- First Quarter Payment: Due April 15th.

- Second Quarter Payment: Due June 15th.

- Third Quarter Payment: Due September 15th.

- Fourth Quarter Payment: Due January 15th of the following year.

Missing any of these deadlines could result in penalties and interest charges. Planning ahead and setting reminders are effective strategies to avoid such issues.

Required Documents

Having the right documents on hand is essential to accurately prepare the declaration. Essential documents include:

- Previous Year’s Tax Return: Useful for reference to project this year’s liabilities.

- W-2 and 1099 Forms: To report various income sources.

- Investment Statements: For dividends, capital gains, and other investment income.

- Bank Statements: For other sources of income and financial activities.

These documents help ensure that the tax estimates are as precise as possible, minimizing errors and omissions.

IRS Guidelines

The IRS provides specific guidelines to help taxpayers accurately complete the form. These guidelines include instructions on calculating estimated taxes and details about changes in tax law that could affect estimates:

- Tax Rate Changes: Adjustments to the tax brackets may impact tax liability estimates.

- New Deductions or Credits: Stay updated on additional deductions or credits enacted for the given tax year.

- Record Keeping: Maintain records supporting estimates used in the declaration.

Adhering to these guidelines helps avoid mistakes that could lead to additional scrutiny or penalties from the IRS.

Penalties for Non-Compliance

Failure to comply with estimated tax payment requirements may result in several penalties:

- Underpayment Penalty: Applied if owed taxes exceed payments by more than $1,000.

- Late Payment Penalty: Incurred for payments not made by due dates.

- Interest Penalties: Accumulated on unpaid balances, compounding the liability.

Understanding these penalties emphasizes the importance of timely and accurate submission of the declaration.

Examples of Using the Declaration of Estimated Personal Income Tax

Consider a self-employed graphic designer who anticipates earning $80,000 over the year. By estimating expenses of $20,000, she calculates taxable income of $60,000. Using the relevant tax rate, she determines her estimated tax liability and plans her quarterly payments accordingly.

Another example is a retiree drawing income from pensions and investments. By projecting both withdrawal amounts and potential capital gains, he uses the declaration to spread tax payments throughout the year, avoiding the risk of underpayment penalties.

These scenarios illustrate the diverse applications of the declaration in managing tax obligations for various income types and financial situations.