Definition & Meaning

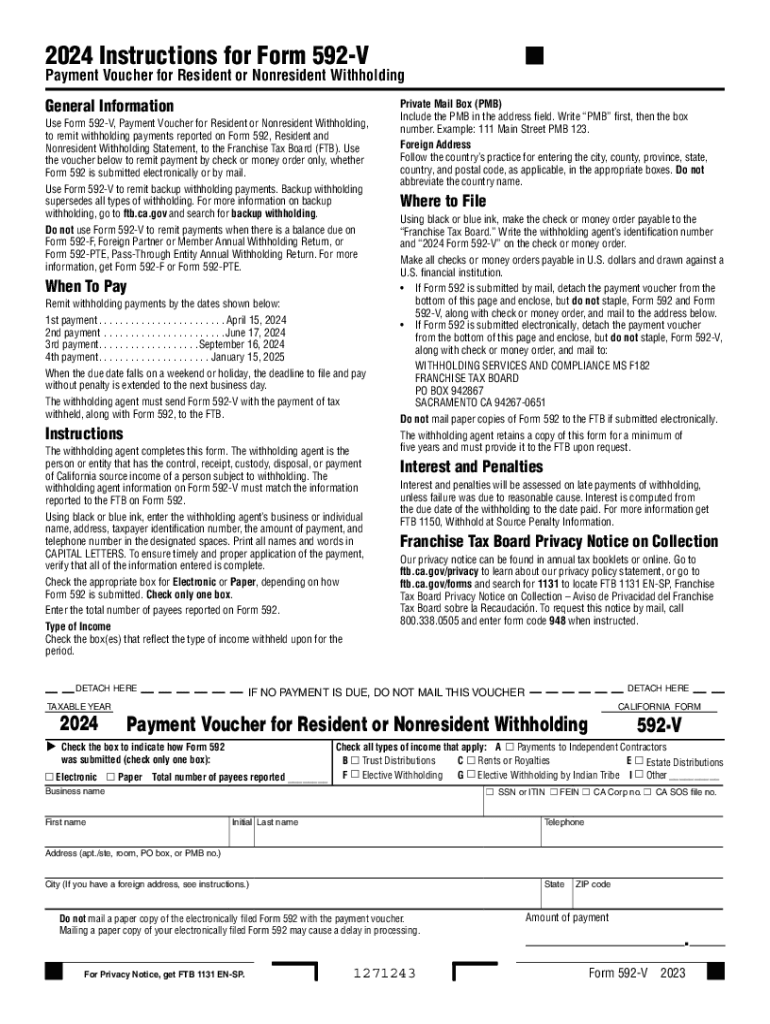

The California FTB Form 592-V, Payment Voucher for Resident or Nonresident Withholding, serves as a means for taxpayers to remit withholding payments to the Franchise Tax Board (FTB). Typically used to accompany Form 592, this document is crucial in correctly executing tax withholding for various types of income, such as payments to independent contractors and partnerships. The voucher ensures that the withholding amount is appropriately credited to the taxpayer's account, preventing discrepancies during reconciliation. The form is especially significant for those earning income within California but residing out-of-state or even internationally, where withholding may differ.

Key Elements of the California FTB Form 592-V

Form 592-V includes several essential components that must be accurately filled out to ensure compliance and accurate tax payments. Key elements include:

- Taxpayer Information: This section requires the completion of personal or business details such as name, address, and taxpayer identification number (TIN). It is crucial for identifying the account to which the payment should be credited.

- Payment Amount: This field is where the precise total of the withholding payment is recorded. Ensuring accuracy here is vital to maintain compliance and avoid future discrepancies.

- Tax Year: Identification of the applicable tax year is necessary to ensure that payments apply to the correct period, thereby aligning with other tax documents and filings.

Each element of the form serves a unique purpose and needs to be completed accurately for the form to fulfill its legal and financial function.

How to Use the California FTB Form 592-V

Using Form 592-V requires understanding both when it's necessary and how it complements other forms. Here's a step-by-step guide:

-

Verify Applicability: Determine if you need to withhold taxes for nonresident payments. Payments could be for services, rent, royalties, or even partnership income sourced from California.

-

Compute Withholding: Accurately calculate the required withholding amount based on California's tax guidelines for nonresident income.

-

Complete Form 592: Before executing Form 592-V, prepare Form 592, detailing the income, withholding amounts, and recipient information.

-

Fill out Form 592-V: Record all necessary details, such as TIN, payment amounts, and tax year on Form 592-V.

-

Submit Payment: Enclose Form 592-V with the withholding payment and submit it to the FTB using the appropriate submission method.

Proper use of Form 592-V ensures compliance with California's tax law, preventing penalties and ensuring accurate accounting of withholdings.

Steps to Complete the California FTB Form 592-V

Successfully completing Form 592-V involves a clear understanding of each section. Here are detailed steps:

-

Gather Information: Before beginning the form, collect all necessary data, such as the taxpayer's contact information, TIN, and withholding details.

-

Prepare Prior Forms: Ensure Forms 592 and other related documents are ready and information is cross-verified for accuracy.

-

Enter Payment Details: Complete the payment section of the form, specifying the correct amount and tax year.

-

Review for Accuracy: Double-check all entered data to ensure accuracy and compliance before submission.

-

Submit with Payment: Attach the completed Form 592-V with the withholding payment and send them to the FTB via an accepted submission method, such as mail or electronic payment.

This step-by-step completion ensures the taxpayer maintains compliance with state tax obligations.

Who Typically Uses the California FTB Form 592-V

Form 592-V is essential for a variety of entities responsible for withholding tax on payments to nonresidents. These include:

- Businesses: Companies operating in California that make payments to out-of-state contractors or service providers.

- Partnerships: Entities distributing income to partners not residing in California.

- Property Managers: Handling rent or royalty payments to nonresident owners.

Individuals and entities involved in transactions necessitating tax withholding will regularly engage with this form to ensure regulatory adherence.

Filing Deadlines / Important Dates

Understanding and adhering to deadlines ensures that filings are timely and avoid penalties:

- Quarterly Deadlines: Payments and submissions for Form 592-V are generally due on the 15th of the month following the close of each quarter (April, July, October, January).

- Year-End Reconciliations: Ensure final payments align with the annual tax filing, often due in alignment with standard state and federal tax deadlines.

Timely filing ensures compliance and minimizes risks associated with late submissions or payments.

Penalties for Non-Compliance

Failure to submit Form 592-V punctually or accurately can lead to penalties. Key considerations include:

-

Late Payment Penalties: Additional fees and interest accrue on payments received after due dates, impacting financial health.

-

Accuracy Penalties: Incorrectly completed forms can lead to further audits and fines if not aligned with reported withholdings and actual payments.

Staying diligent with form submission prevents these punitive measures.

Form Submission Methods (Online / Mail / In-Person)

Taxpayers have multiple options for submitting Form 592-V to the FTB:

-

Online Submission: Using the state’s tax portal for digital submission and payments provides a swift and verifiable method.

-

Mail: Forms can be sent via mail if electronic submission is unavailable, ensuring you retain dated proof of mailing.

-

In-Person: Less common but an option for those who prefer direct handover at official FTB locations.

Choosing the right method depends on individual circumstances, but online submission is becoming increasingly favored for its speed and efficiency.