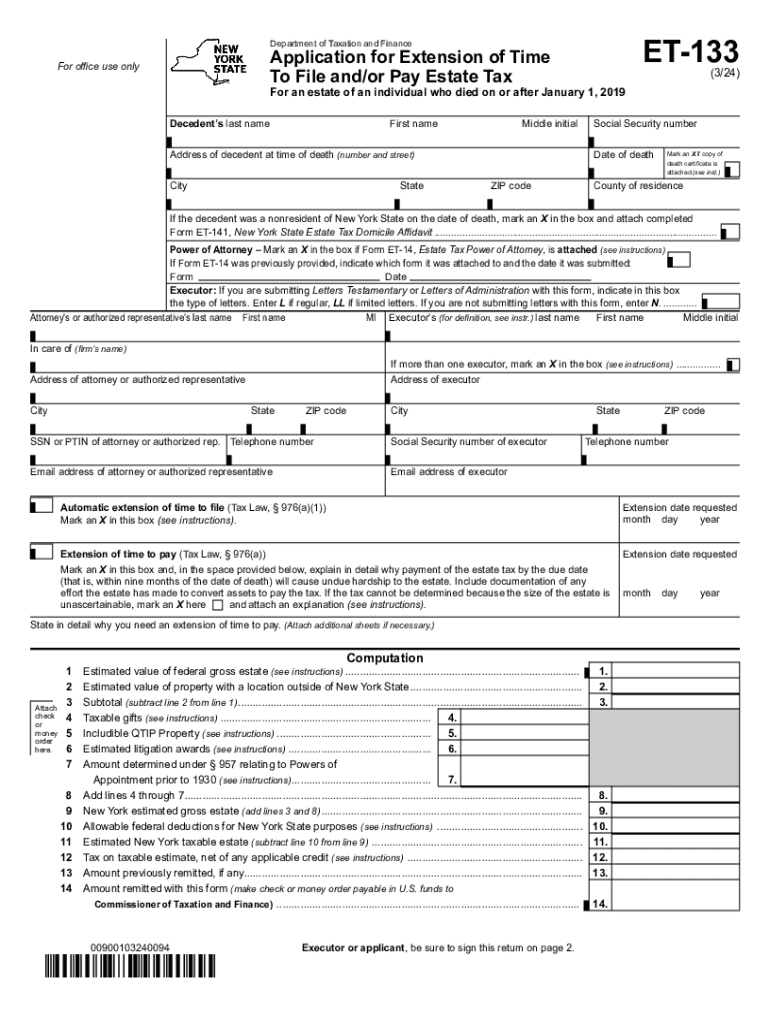

Definition and Purpose of Form ET-133

Form ET-133 serves as an application for individuals in New York seeking an extension of time to file and/or pay estate tax. Specifically, this form is relevant for estates belonging to individuals who passed away on or after January 1, 2019. By submitting this form, executors can request additional time, often due to complexities in managing the deceased's assets or other valid financial constraints. It is essential for both submitting timely and ensuring compliance with New York state tax obligations related to estates.

How to Obtain the Instructions for Form ET-133

To secure the instructions for Form ET-133, executors can access them through the New York Department of Taxation and Finance. This resource is available both online as a downloadable PDF and through request mail. Having these instructions is crucial as they detail the step-by-step process for completing the form, aiding in accurate and complete submissions. Online availability ensures ease of access and the possibility to print multiple copies if necessary.

Steps to Complete the Form ET-133

Completing Form ET-133 involves several essential steps:

-

Gather Necessary Information

- Basic details about the decedent, including date of death and Social Security number.

- Executor information, ensuring legal authority and contact details are up to date.

- Financial statement summaries of the estate to calculate the total estimated estate value.

-

Detailed Financial Calculations

- Accurately compute the taxable estate value, considering all assets and liabilities.

- Justify any extensions through comprehensive explanations on financial constraints.

-

Affirmation and Signature

- Ensure that the executor's signature is included to validate the form.

Completing these steps accurately increases approval chances and facilitates any future inquiries.

Key Elements to Know About Form ET-133

Some primary elements are crucial for a successful submission:

- Executor Information: Legal authority and responsibilities of the executor concerning the estate.

- Decedent Details: Accurate documentation regarding the deceased individual, ensuring accuracy in personal and financial data.

- Financial Overview: Detailed computation of the estate's financial situation, including assets, debts, and tax obligations.

Understanding these elements helps executors address critical requirements, reducing the likelihood of delays or rejections.

Legal Implications and Use

Form ET-133 carries legal significance as it pertains to state tax obligations. When properly executed, it provides an automatic extension, though interest may still accrue on any unpaid tax amounts. Executors must ensure accurate and honest reporting to avoid potential penalties or legal scrutiny. This form acts as a legal bridge, granting additional time under New York's tax laws and allowing for more meticulous estate settlement procedures.

State-Specific Rules Governing Form ET-133

New York has distinctive rules regarding estate tax extensions:

- Filing Timeline: Requests must be filed before the original estate tax return due date.

- Interest on Taxes: Extensions do not waive interest on unpaid taxes accrued post the original due date.

- Required Documentation: Additional supporting documents might be required to substantiate claims, particularly concerning financial hardship or complications.

These rules underline the necessity for compliance specific to New York state regulations regarding estates and taxation.

Who Typically Uses Form ET-133

Primarily, executors or administrators of estates are responsible for completing Form ET-133. These individuals manage estate settlements for deceased persons, ensuring all tax obligations are met. In certain cases, other legally designated individuals, such as lawyers or tax professionals working on behalf of estates, may also fill out the form. Their involvement typically reflects the complexity or size of the estate in question, with larger estates necessitating formal legal and financial expertise.

Penalties for Non-Compliance

Failure to file Form ET-133 or submitting incorrect information can lead to several penalties:

- Late Fees: If the estate tax return isn't filed or paid in time without approval for an extension, late filing penalties apply.

- Interest Accrual: Interest continues to accrue on any unpaid taxes from the original due date, even if the form is filed.

- Legal Action: In severe cases of misrepresentation or fraud, legal consequences can be pursued by New York State authorities.

Understanding these penalties prompts timely and accurate form submissions, ensuring compliance and avoiding costly repercussions.

Filing Deadlines and Important Dates

Understanding key deadlines is vital:

- Original Tax Return Due Date: Nine months after the decedent's date of death.

- Extension Request Deadline: Prior to the original due date.

- Approval Timeline: Requires sufficient processing time, so early submission is advised.

Awareness of these deadlines helps executors manage estate responsibilities effectively, avoiding unnecessary penalties or interest charges.

Required Documents for Form ET-133

Submission requires specific documentation:

- Death Certificate: Official proof of the decedent's passing.

- Estate Valuations: Detailed financial statements supporting the estate's value and tax liability.

- Executor Authorization: Legal documentation confirming the executor's authority.

Having these documents prepared and organized streamlines the extension process, enhancing accuracy and efficiency in form submission.

Form Submission Methods

Form ET-133 can be submitted via different methods:

- Online Submission: Convenient and quick, reducing paper use and ensuring electronic tracking.

- Mail Submission: Traditional approach, useful for including original documentation or additional materials.

Different methods cater to varying needs and preferences, allowing executors to choose the most suitable option for their circumstances.