Definition and Meaning

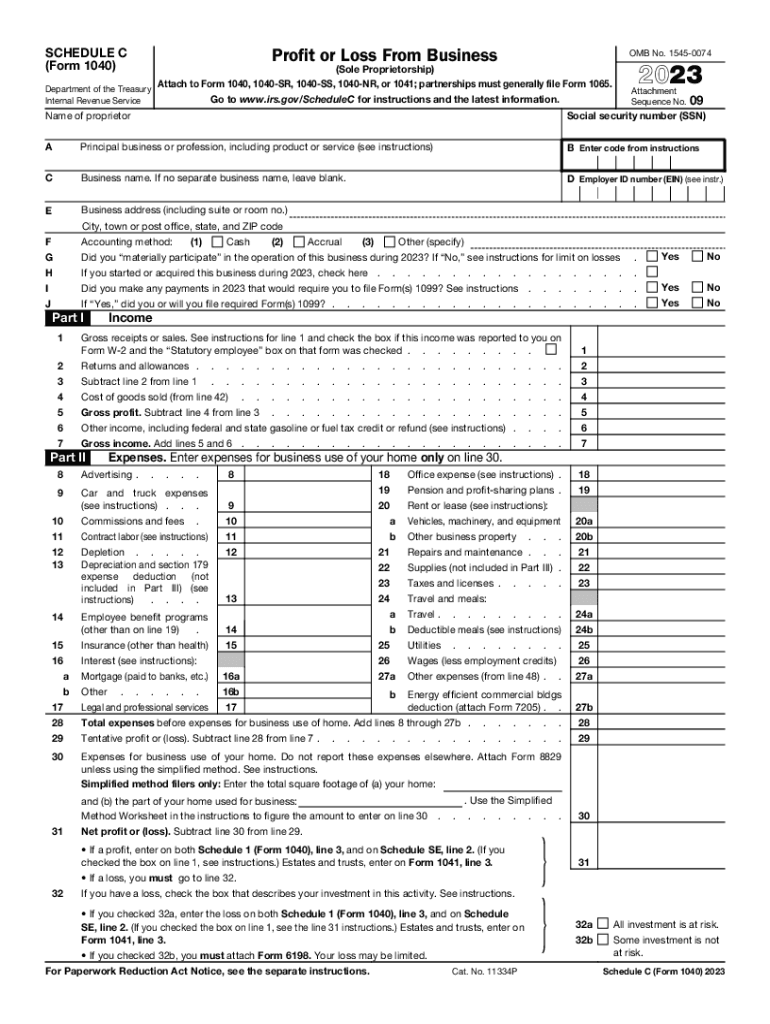

The Form (Profit Loss Statement) is an essential document used by individuals, primarily sole proprietors, to report their business income and expenses to the IRS for the year 2023. This form calculates the net profit or loss from business operations, which directly impacts the individual's taxable income. It includes a detailed breakdown of income earned, deductibles, and operational costs. Understanding this form is crucial for accurate tax reporting and compliance with federal tax regulations.

How to Use the Form (Profit Loss Statement)

The primary function of the Form is to identify the financial results of business activities. Users begin by listing all income sources, such as sales revenues or service fees. Next, they itemize expenses, which can include costs related to supplies, employee wages, and utilities. The net amount, after subtracting expenses from income, indicates the business's profit or loss. This figure is then reported on the individual's tax return to determine tax obligations.

Steps to Complete the Form

- Gather Income Records: Collect all income statements, invoices, and sales receipts.

- Identify Deductible Expenses: List eligible business expenses, like office rent and travel costs.

- Calculate Cost of Goods Sold (COGS): For businesses that produce goods, determine the COGS to deduct from sales revenue.

- Sum Total Income and Expenses: Add up all income and expenses separately.

- Calculate Net Profit or Loss: Subtract total expenses from total income.

- Complete and Attach to Tax Return: Fill out the form with computed details and attach it to Form 1040.

Who Typically Uses the Form (Profit Loss Statement)

Form is most commonly utilized by sole proprietors and self-employed individuals who operate businesses individually, rather than through a corporation or partnership. Freelancers, independent contractors, and gig economy workers also use this form to report business earnings. It supports a wide range of business activities, making it a versatile document for diverse entrepreneurial ventures.

Key Elements of the Form (Profit Loss Statement)

The form encompasses several crucial components, including:

- Income Line Items: Sections detailing various income sources.

- Expense Categories: Classification for deductible expenses, such as advertising, supplies, and repairs.

- Cost of Goods Sold (COGS): An area dedicated to calculating costs associated with producing goods.

- Net Income Calculation: Lines where profit or loss is determined by netting expenses against income.

IRS Guidelines

The IRS provides comprehensive guidelines on how to accurately complete the Form . These guidelines outline:

- Proper documentation required for all reported figures.

- Specification of what constitutes deductible expenses.

- Instructions on the treatment of depreciation and amortization.

- Requirements for maintaining evidence of reported income and expenses.

Adhering to these guidelines helps avoid errors and potential penalties.

Filing Deadlines and Important Dates

The filing deadline for Form aligns with the individual income tax filing deadline, typically April 15th. Extensions may be available, but they usually require filing a request before the original deadline. It's essential for taxpayers to be aware of these timelines to avoid late filing penalties, interest charges, or processing delays.

Penalties for Non-Compliance

Non-compliance with filing requirements, such as failure to file the Form or inaccuracies in reporting, can lead to penalties. These may include:

- Late Filing Penalties: Financial charges for overdue submissions.

- Accuracy-Related Penalties: Fines applied for significant discrepancies in reported figures.

- Interest Charges: Accumulated interest on unpaid tax liabilities.

To mitigate these risks, it is imperative to ensure timely and accurate filing.

Digital vs. Paper Version

Taxpayers have the option to file the Form electronically or through traditional paper submission. Digital filing offers benefits like faster processing times, immediate confirmation of receipt, and reduced risk of errors due to integrated checks. On the other hand, paper submissions may be preferred by those less familiar with digital interfaces. Understanding both methods helps users choose the most appropriate option for their needs.

Software Compatibility

Various tax software programs, including TurboTax and QuickBooks, support the Form , providing tools to streamline the completion process. These software solutions offer:

- Step-by-step guidance to ensure all required sections are accurately filled.

- Automatic calculations, reducing the likelihood of mathematical errors.

- E-filing options for quicker submission and processing.

By leveraging these tools, users can simplify their tax reporting obligations while ensuring precision and compliance.