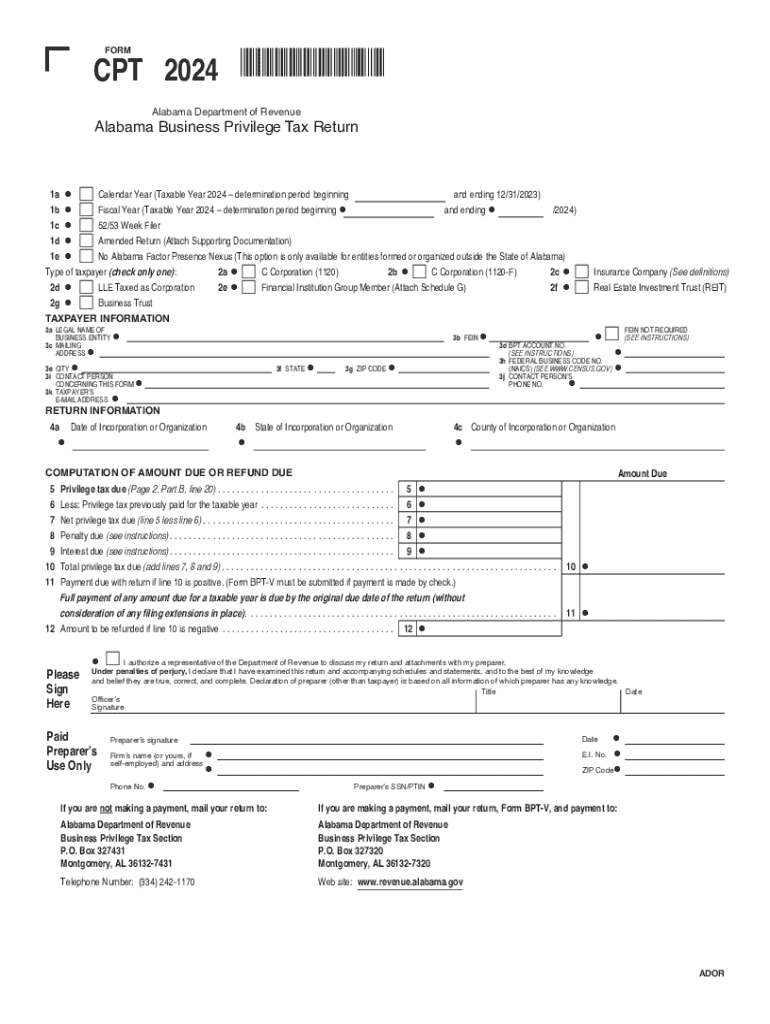

Definition & Meaning

The "1a Calendar Year (Taxable Year 2024 determination period beginning" refers to a specific timeframe used for financial reporting and tax purposes in the United States. This period defines the fiscal year structure that businesses and individuals follow to determine taxable income and calculate tax liabilities. It plays a crucial role in finalizing financial reports and ensuring compliance with the IRS regulations. Understanding this term is pivotal for aligning your accounting practices with federal tax standards, particularly for entities using a calendar year as their fiscal year.

Key Elements of the 1a Calendar Year (Taxable Year 2024 determination period beginning

- Time Frame: The period typically covers from January 1 to December 31, 2024. This standard calendar year is commonly used for reporting income and expenses for tax purposes.

- Purpose: It aligns the reporting of taxable income with federal tax requirements, ensuring consistency in financial accounting and tax filing.

- Application: Widely applied by individual taxpayers, small businesses, and entities that do not have complex financial activities not requiring an alternative fiscal year.

Steps to Complete the 1a Calendar Year (Taxable Year 2024 determination period beginning

- Gather Necessary Documents: This includes income statements, expense records, and previous tax documents.

- Record Financial Transactions: Accurately document all income and expenses incurred within the timeline.

- Calculate Taxable Income: Deduct eligible expenses from the total income to find the taxable income.

- Complete Tax Forms: Utilize forms relevant to your income bracket and business entity.

- Review and Submit: Ensure accuracy in filling out the forms and submit them via the preferred method (e-file or paper mail).

Who Typically Uses the 1a Calendar Year (Taxable Year 2024 determination period beginning

- Individual Taxpayers: Most individual filers use the calendar year to report income and file taxes.

- Small Businesses: Sole proprietors and partnerships often prefer the calendar year as it aligns with personal filing timelines.

- Corporations: Certain corporations opt for the calendar year, making their tax reporting straightforward and synchronized with personal taxes of business owners.

IRS Guidelines

- Compliance: Adherence to IRS regulations requires that taxable income is reported and taxes are paid according to the guidelines set for the 2024 tax year.

- Filing Requirements: Follow IRS guidelines on the specific forms needed for the 2024 tax year and ensure accurate reporting.

- Updates: Be aware of any changes to tax laws and IRS guidelines that may affect your filing for the calendar tax year.

Filing Deadlines / Important Dates

- Regular Filing Deadline: April 15, 2025, is the standard deadline for filing taxes for the fiscal year ending December 31, 2024.

- Extension Requests: Taxpayers needing more time can file for an extension, typically allowing until October 15, 2025, for filing completion.

- Quarterly Payments: Important for businesses and self-employed individuals to meet quarterly estimated tax payment dates to avoid penalties.

Penalties for Non-Compliance

- Late Filing Penalties: If taxes are not filed by the due date, penalties and interest on unpaid taxes will accrue.

- Underpayment Penalties: Failure to pay the correct estimated taxes quarterly may result in financial penalties.

- Missed Deadlines: Missing the extension request deadline can lead to enhanced penalties, making timely filing critical.

Required Documents

- Income Records: Includes W-2s, 1099s, and any other documents showing earnings and income.

- Expense Documentation: Proper documentation of deductible expenses for accurate tax reduction.

- Previous Tax Returns: Necessary for reference and ensuring consistency in financial information across years.

Software Compatibility (TurboTax, QuickBooks, etc.)

- Integrations: Many financial software programs are compatible with IRS tax forms and streamline the filing process.

- Benefits of Use: Software solutions like TurboTax and QuickBooks can simplify data entry and calculation, ensuring accurate results.

Business Entity Types (LLC, Corp, Partnership)

- Entities Using Calendar Year: Certain LLCs and partnerships may benefit from a calendar year to align with the owner's personal filing deadlines.

- Corporate Considerations: Corporations must determine if the calendar year suits their financial reporting and legal requirements.

Examples of Using the 1a Calendar Year (Taxable Year 2024 determination period beginning

- Individual Filers: A taxpayer uses the calendar year to compile all income sources, ensuring no discrepancy or omission in annual earnings.

- Small Business Owner: A sole proprietor aligns their business income reporting with the calendar year to simplify taxes and reduce errors.

- Corporations: Some entities may find using the calendar year beneficial when aligning corporate with individual taxes within annual planning.

Legal Use of the 1a Calendar Year (Taxable Year 2024 determination period beginning

- Tax Compliance: Abides by federal regulations for accurate reflection of income and liabilities during audits.

- Documentation: Legally established records serve as evidence of income and tax compliance for all entities using the calendar year.

State-Specific Rules for the 1a Calendar Year (Taxable Year 2024 determination period beginning

- Variations by State: Some states have unique requirements or benefits attached to using a calendar year for tax purposes.

- Harmonizing Federal and State Filings: Understanding specific state guidelines can help ensure compliance and potentially reduce state tax burdens.