Definition and Meaning

Form 500, the "Authorization To Disclose Tax Information and Designation of Representative," is a crucial document issued by the North Dakota Office of State Tax Commissioner. It empowers taxpayers to authorize the sharing of their confidential tax information with a designated individual or firm. Additionally, it facilitates the appointment of a representative to handle matters concerning specific taxes. This form plays a vital role in ensuring that taxpayers can efficiently manage their tax affairs by appointing qualified individuals to represent them in dealings with tax authorities.

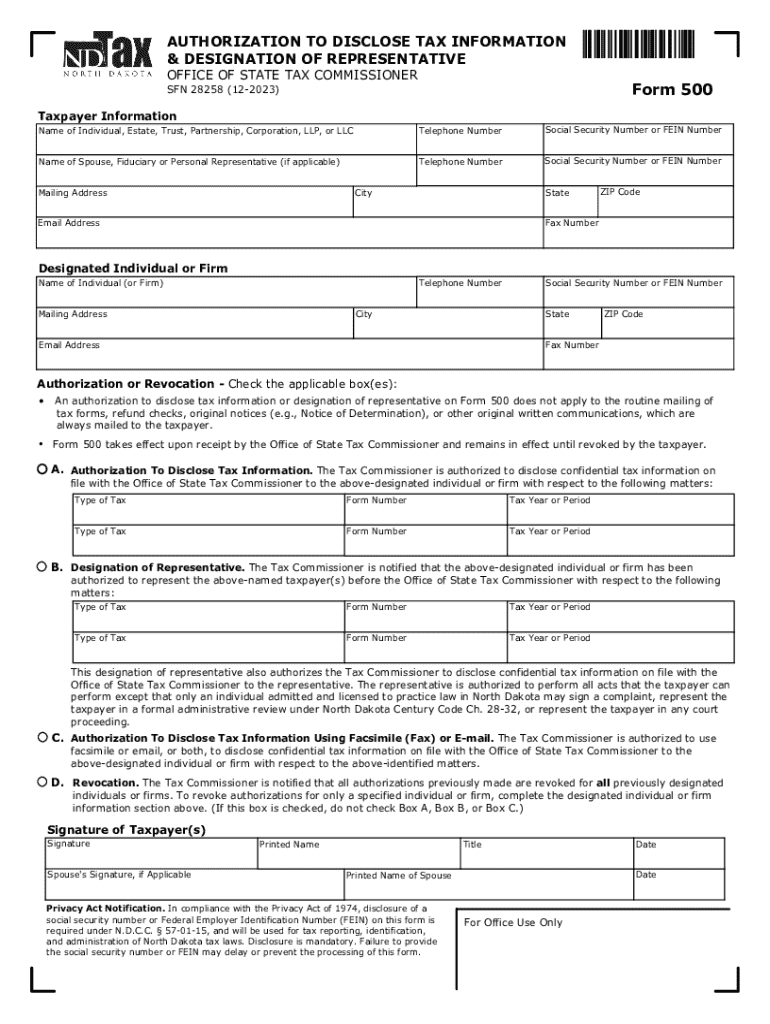

Key Elements of Form 500

Form 500 is composed of several important sections designed to capture the necessary information for authorizing the disclosure of tax information. These sections include:

- Taxpayer Information: This section requires personal details such as name, address, and taxpayer identification number.

- Representative Information: Details of the designated representative, including their name, title, and address, must be filled out in this section.

- Authorization Details: Clearly outlines which tax years and types of taxes the authorization pertains to.

- Revocation Options: Specifies how and when the taxpayer can revoke the authorization, ensuring flexibility and control over the disclosure.

Each section ensures comprehensive documentation and safeguards both the taxpayer's and the representative's interests.

Steps to Complete Form 500

Completing Form 500 involves a series of careful steps to ensure accuracy and compliance:

- Gather Required Information: Assemble details about the taxpayer and the designated representative.

- Fill in Taxpayer Information: Enter personal information, ensuring consistency with official tax records.

- Identify the Representative: Provide accurate details about the representative or firm involved.

- Detail Authorization Scope: Clearly define the scope of authorization, including specific tax periods and types.

- Review Revocation Process: Understand how to revoke authorization if circumstances change.

- Sign and Date the Form: Ensure both the taxpayer and representative (where applicable) sign the form to authenticate the authorization.

- Submit the Form: Choose an appropriate submission method, which could include mailing or in-person delivery, depending on the state’s guidelines.

Legal Use of Form 500

Using Form 500 comes with specific legal stipulations that must be adhered to. The authorization provided is legally binding and subject to the confidentiality regulations set forth by the North Dakota Office of State Tax Commissioner. The form ensures that representatives only have access to the specified information, and taxpayers are provided with the legal assurance that their data is handled according to the law. This legal framework protects both parties, ensuring accountability and transparency in handling sensitive tax information.

Who Typically Uses Form 500

The primary users of Form 500 are individual taxpayers and business entities in North Dakota. These users often seek to delegate their tax-related tasks to tax professionals or legal representatives. Small businesses, in particular, gain significant benefits, as they can appoint accountants or tax advisors to manage complex tax obligations. Additionally, individuals with intricate tax situations, such as self-employment income or multiple sources of revenue, often use Form 500 to ensure that their tax liabilities are expertly handled.

State-Specific Rules for Form 500

Form 500 must be understood within the context of North Dakota’s unique tax regulations. The state has specific rules governing the types of taxes that can be disclosed and how the designation of representatives is managed. The form is tailored to North Dakota's tax laws, meaning that users need to be aware of any unique requirements or limitations imposed by the state. These might include specific procedures for revocation or amendments, ensuring that representatives adhere strictly to state legislation.

Why Use Form 500

Utilizing Form 500 offers several benefits, primarily streamlining the process of managing tax-related issues through delegation. Taxpayers who may not be well-versed in tax law can leverage the expertise of seasoned professionals, ensuring compliance and accuracy in filings. Additionally, by allowing representatives to handle their tax affairs, individuals and businesses can focus on core activities. The form also provides legal protection by clearly defining the scope of the representative’s powers, reducing the risk of unauthorized access to sensitive information.

Important Terms Related to Form 500

Understanding the terminology associated with Form 500 is crucial for proper utilization:

- Taxpayer Identification Number (TIN): An essential number required to complete the form, identifying the taxpayer with tax authorities.

- Representative: The individual or firm authorized to act on behalf of the taxpayer.

- Revocation: The process through which the taxpayer can nullify the authorization granted to a representative.

- Confidential Tax Information: Taxpayer information that is protected under state and federal privacy laws, only disclosed through authorized channels.

By familiarizing themselves with these terms, users can ensure they correctly fill out and interpret the form to safeguard their tax interests.

Form Submission Methods (Online / Mail / In-Person)

There are several ways taxpayers can submit Form 500. Depending on individual preferences and requirements, choices typically include:

- Online Submission: For tech-savvy individuals, many tax authorities, including North Dakota, might offer digital submissions through secure portals, providing convenience and instant confirmation.

- Mail Submission: Traditional mail submission remains a viable option for those who prefer physical documentation.

- In-Person Submission: For immediate queries or assistance, taxpayers can submit forms directly at designated offices, ensuring clarity and accuracy in submission.

Choosing the appropriate submission method can impact processing times, so taxpayers should select a method that best meets their needs and urgency.