Definition & Meaning

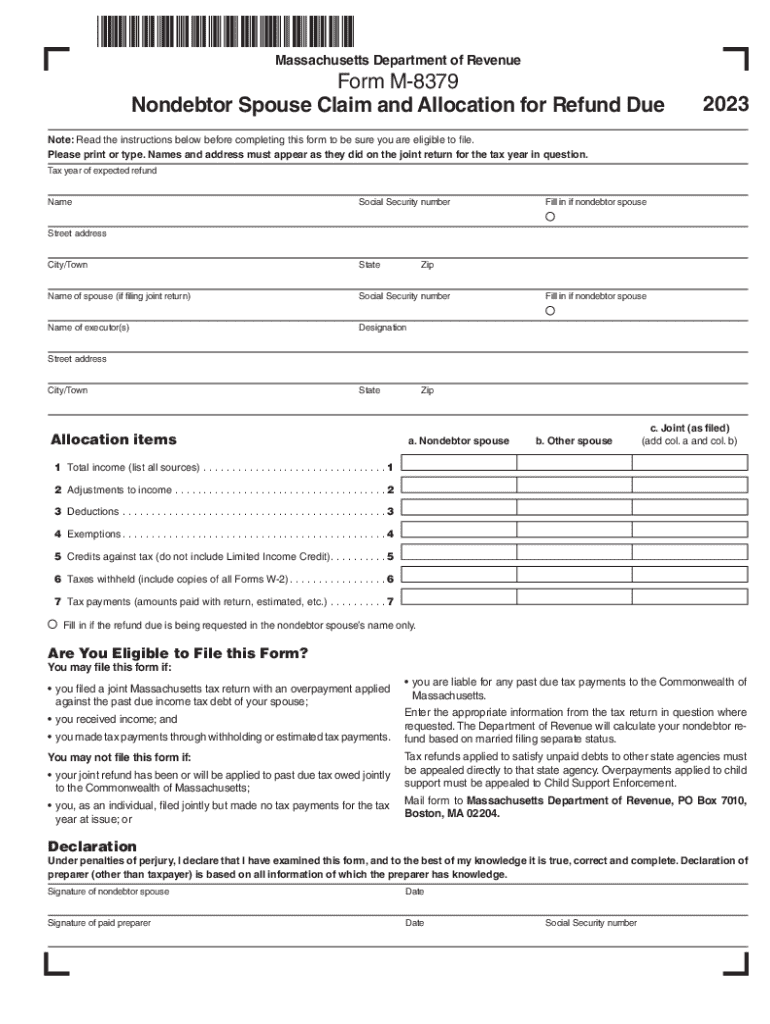

The M-8379 form, issued by the Massachusetts Department of Revenue, enables a nondebtor spouse to claim and allocate tax refunds from a joint tax return. This form is crucial when a tax refund is seized to cover a spouse's debts, allowing the nondebtor spouse to recoup their share. By filing the M-8379, the nondebtor spouse can legally request that their portion of the refund be returned, provided they meet specific criteria detailed within the form.

Key Points:

- The primary purpose of the M-8379 is to address tax overpayments on joint returns that have been applied against the spouse’s outstanding tax liabilities.

- This form ensures fair distribution of tax refunds between spouses when one spouse has debts that could affect joint refunds.

Steps to Complete the M-8379 Nondebtor Spouse Claim

Filling out the M-8379 form requires careful attention to detail. Below is a step-by-step guide to help navigate through this process efficiently.

-

Obtain the Form: Acquire the M-8379 form from the Massachusetts Department of Revenue's website or local office.

-

Personal Information Section:

- Fill in your full name, Social Security number, and address.

- Include your spouse’s equivalent details, ensuring accurate entry for identification purposes.

-

Income and Allocation Details:

- Provide a detailed breakdown of income received for the tax year in question.

- Clearly indicate the respective contributions of income by each spouse.

-

Explanation and Declaration:

- Provide a comprehensive explanation of why the refund should be reallocated.

- Sign the declaration affirming the truthfulness of the provided information.

-

Attach Supporting Documents: Gather all necessary documents, such as proof of income and previously filed tax returns, to substantiate your claim.

-

Submission: Once completed, submit the form and any attached documentation by mail or electronically, according to the instructions provided.

Eligibility Criteria

To successfully file the M-8379 form, certain criteria must be satisfied:

- Joint Tax Return: The couple must have filed a joint tax return during the tax year in question.

- Debt Condition: The overpayment must be applied to a debt owed by one spouse that the nondebtor spouse is not legally obligated to pay.

- Residency Status: Both spouses must be residents of Massachusetts, or qualify as such, during the tax year.

Additional Considerations:

- Ensure that no prior claim was filed for that specific tax year.

- Verify that the nondebtor spouse is indeed entitled to a portion of the refund.

Required Documents

When filing the M-8379 form, several documents are necessary to verify the claim:

- Proof of Income: W-2s, 1099s, and any other income statement relevant to the tax year.

- Tax Return Copies: Provide a copy of the original joint tax return filed.

- Debt Documentation: Any notices or statements related to the spouse's debt that influenced the refund allocation.

These documents support your claim and enhance the validity of your submission to the Massachusetts Department of Revenue.

Legal Use of the M-8379 Nondebtor Spouse Claim

The M-8379 form serves as a legal avenue for a nondebtor spouse to reclaim a fair share of a tax refund. This provision ensures that one spouse's financial obligations do not adversely impact the joint financial benefits rightfully belonging to both partners.

Legal Provisions:

- Aligns with Massachusetts state tax laws designed to protect nondebtor spouses.

- Requires signature and submission as a formal request to the Massachusetts Department of Revenue.

Important Terms Related to M-8379 Nondebtor Spouse Claim

Understanding certain terms is vital when dealing with the M-8379 form:

- Nondebtor Spouse: The spouse who is not responsible for the debt affecting the tax refund.

- Joint Tax Return: A tax return filed by a married couple that combines their incomes and allows for joint credit claims.

- Refund Allocation: The process of distributing a tax refund between spouses based on their respective income contributions.

Context and Application:

- These terms are integral to grasping the legal and financial aspects of the M-8379 form, facilitating proper filing and ensuring compliance.

Filing Deadlines / Important Dates

When dealing with the M-8379 form, it is essential to be aware of the key deadlines:

- Filing Period: The form should generally be filed within three years from the original due date of the joint tax return.

- Amendments and Extensions: If an amended return is necessary, ensure submission within two years from the payment of the tax or three years from the original deadline, whichever is later.

State-Specific Rules for the M-8379 Nondebtor Spouse Claim

Given this form is specific to Massachusetts, it's governed by state-specific rules that may differ from federal guidelines or other states’ procedures. Understanding these nuances is critical for accurate filing and ensuring proper compliance with state tax laws.