Definition & Meaning

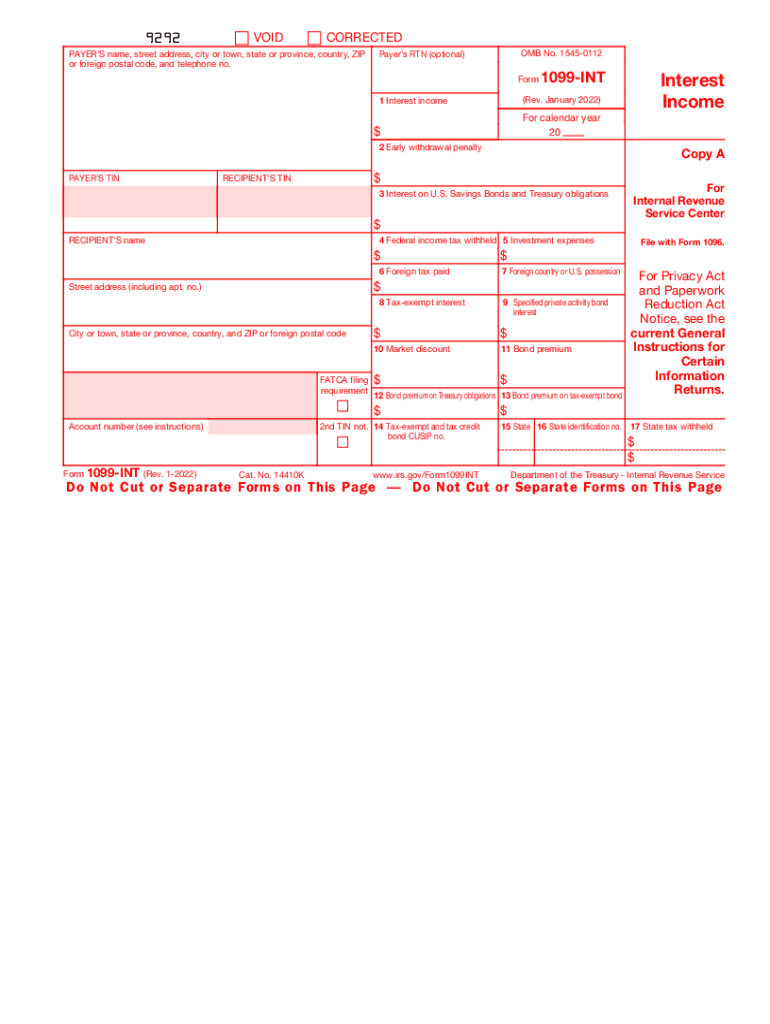

Form 1099-INT is a tax document used in the United States to report interest income paid to individuals. This form is crucial for taxpayers and the IRS alike, as it ensures that all interest income is accurately reported and taxed accordingly. The issuer of the interest—typically financial institutions like banks or credit unions—must send out the form to recipients and the IRS if the interest exceeds $10.

Key Elements Explained

- Interest Income: This refers to the income earned from interest on accounts like savings or certificates of deposit.

- Payee: The individual or entity receiving the interest income.

- Payer: The institution or entity that pays the interest to the individual or entity.

How to Obtain the 1099-INT

Financial institutions are responsible for providing Form 1099-INT to both the interest recipient and the IRS. Typically, these forms are sent out by January 31 each year, covering the previous year's interest income.

Ways to Obtain the Form

- Through Mail: Most institutions mail the form directly to your registered address.

- Online Access: Many banks and credit unions offer electronic access to tax documents through their online banking portals.

- Customer Service: If you do not receive your form or misplace it, contact your financial institution's customer service for assistance.

Steps to Complete Form 1099-INT

Accurate completion of Form 1099-INT involves a series of careful steps, primarily handled by the interest payer.

- Identify Interest Payees: Determine all individuals or entities to whom $10 or more in interest was paid.

- Calculate Total Interest Paid: Compile all interest payments made during the year.

- Fill Out Required Information: Complete the sections detailing both the payee and payer information.

- Submit Copies: Send Copy A to the IRS and Copy B to the interest payee.

Who Typically Uses the 1099-INT

Form 1099-INT is used by:

- Financial Institutions: Banks, credit unions, or brokerages issuing $10 or more of interest.

- Account Holders: Individuals who receive interest income must use the form to report this income on their tax returns.

- The IRS: Ensures compliance with tax regulations by verifying reported interest income.

IRS Guidelines for 1099-INT

The IRS has set specific guidelines for completing and submitting Form 1099-INT, which help ensure compliance and avoid potential penalties.

Essential Instructions

- Electronic Filing: Required if more than 250 forms are filed by a single institution.

- Accuracy: Ensure that taxpayer identification numbers and interest payments are correct.

- Submission Deadlines: Furnish the forms by January 31 to taxpayers; file with the IRS by the end of February or March if filed electronically.

Important Terms Related to 1099-INT

Understanding the terminology used in Form 1099-INT is crucial for accurate reporting.

Key Terms

- Box 1 - Interest Income: Total interest paid to the account holder.

- Box 3 - Interest on U.S. Savings Bonds: Non-taxable amounts included for informational purposes.

- Box 8 - Tax-exempt Interest: Interest that is exempt from federal income tax but may require reporting.

Penalties for Non-Compliance

Failure to comply with IRS regulations regarding Form 1099-INT can result in penalties for both the payer and the recipient.

Common Penalties

- Late Filing: There are incremental penalties depending on the lateness of filing.

- Inaccuracies: Incorrect information or incomplete forms may incur additional penalties.

- Failure to Furnish: Not providing the recipient with the form can result in fines.

Filing Deadlines / Important Dates

Correct and timely filing of Form 1099-INT is crucial to avoid penalties.

Key Deadlines

- January 31: Deadline for furnishing Copy B to the recipient.

- February 28: Deadline for paper filing with the IRS.

- March 31: Deadline for electronic filing with the IRS.

State-specific Rules for 1099-INT

Some states have unique reporting requirements that differ from federal guidelines.

Common State Variations

- State Reporting: Some states require copies of the 1099-INT if state taxes are involved.

- Additional Forms: A few states might require additional documentation or forms along with the 1099-INT.

Understanding Form 1099-INT is vital for correct interest income reporting, facilitating proper adherence to both federal and state tax regulations.