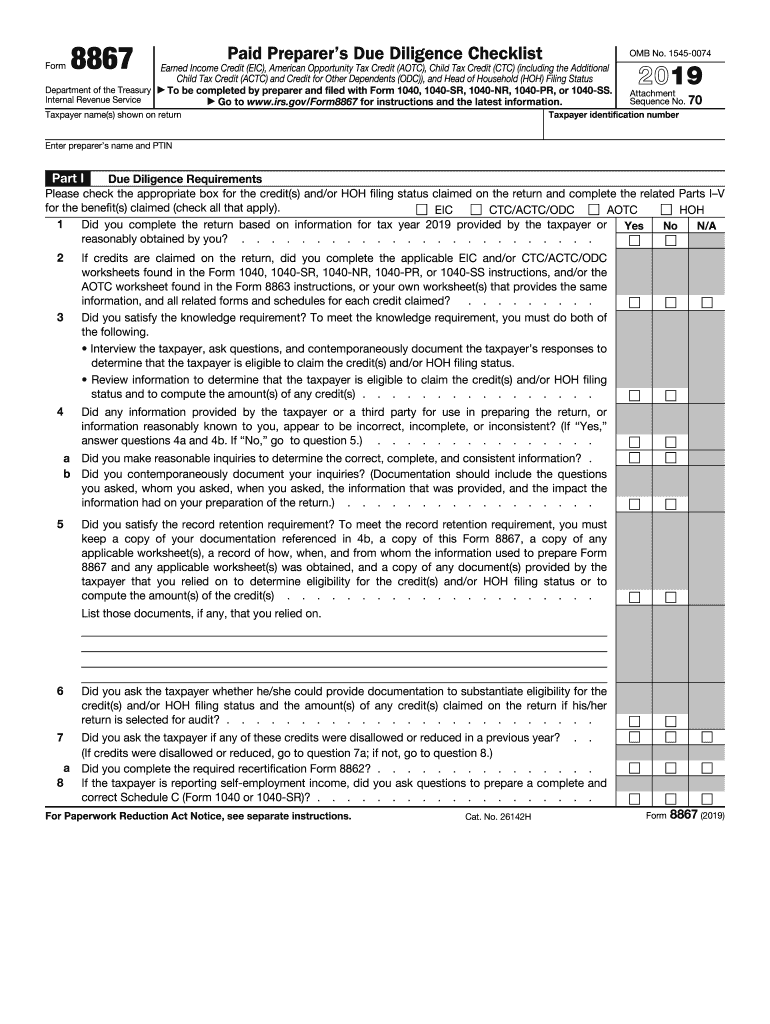

Definition & Purpose of Form 8867

Form 8867, also known as the Paid Preparer's Due Diligence Checklist, is mandated by the IRS for tax preparers to complete when filing returns that claim specific credits, such as the Earned Income Credit (EIC), American Opportunity Tax Credit (AOTC), Child Tax Credit (CTC), and Head of Household (HOH) filing status. This form ensures tax preparers verify taxpayer eligibility, maintain the necessary documentation, and adhere to due diligence requirements for these claims.

Key Elements of Form 8867

- Eligibility Verification: Preparers must assess and confirm the claimant's eligibility for the tax credits they are applying for.

- Documentation of Inquiries: It is essential to document all inquiries made to the taxpayer to support the eligibility for claimed tax credits.

- Record Retention: Preparers are required to retain records and documents that substantiate the information provided on the form and the taxpayer's eligibility for the credits claimed.

How to Use Form 8867

Completing Form 8867 involves checking compliance with due diligence requirements for each credit. Preparers should:

- Review Taxpayer Information: Ensure all information provided by the taxpayer is accurate and complete.

- Verify Eligibility: Use the form to make inquiries and verify eligibility criteria for each credit.

- Document Interactions: Keep detailed records of all taxpayer interactions and inquiries.

- Attach to Returns: Attach Form 8867 to the applicable tax return to indicate compliance with IRS due diligence standards.

How to Obtain Form 8867

Form 8867 can be obtained directly from the IRS website, where it is available for download as a PDF. Alternatively, most tax preparation software includes the form automatically when applicable credits are claimed. Using IRS-approved software ensures that the latest version of the form is used, containing all updates and modifications from previous years.

Digital vs. Paper Version

- Digital: Forms completed and filed using tax software, ensuring automated compliance checks and easier record retention.

- Paper: Can be printed and filled out manually, but requires diligent personal tracking of compliance and retention requirements.

Steps to Complete Form 8867

- Gather Required Documents: Collect all necessary information and documentation from the taxpayer.

- Review Each Section: Assess each section of the form pertaining to specific credits.

- Ensure Accuracy: Double-check the information to ensure complete and accurate documentation.

- Submit with Tax Return: Attach the completed Form 8867 when submitting the taxpayer's IRS return.

Important Terms Related to Form 8867

- Due Diligence: Required effort by tax preparers to verify taxpayer information and eligibility.

- Credits Involved: Specifically refers to EIC, AOTC, CTC, and HOH claims.

- IRS Compliance: Adherence to IRS guidelines for tax preparers regarding due diligence obligations.

IRS Guidelines

The IRS provides detailed guidelines for completing Form 8867. These guidelines outline preparers' responsibilities, including:

- Standard of Conduct: Adhering to professional conduct and ethical standards.

- Penalty Avoidance: Understanding penalties associated with non-compliance or inaccurate claims.

- Performance Evaluation: Familiarity with IRS reviews that ensure adherence to due diligence standards.

Penalties for Non-Compliance

Failure to comply with Form 8867 requirements can result in significant penalties for preparers. These penalties are incurred if the IRS finds that due diligence was not adequately conducted, or records were not properly retained.

Taxpayer Scenarios & Form 8867

Form 8867 applicability varies based on several scenarios:

- Self-Employed Individuals: Must substantiate income claims and eligibility for relevant credits.

- Retirees: Need to confirm EIC eligibility based on retirement income and household status.

- Students: May require specific documentation for the AOTC, evidencing educational expenses and status.