Definition & Meaning

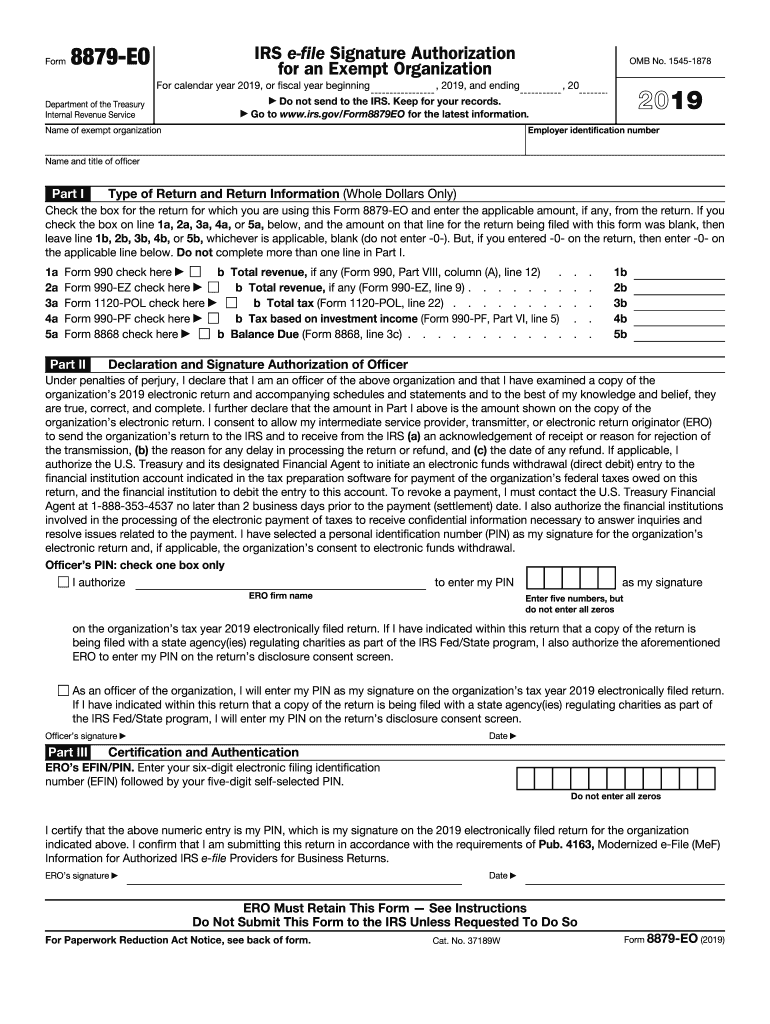

Form 8879-EO, or the IRS e-file Signature Authorization for Exempt Organizations, facilitates the electronic signing of tax returns for exempt organizations. It authorizes the organization officer to sign the organization's return and permits electronic fund withdrawal if necessary. This form is not submitted to the IRS but must be retained for records, serving as proof of consent for electronic filing.

Key Responsibilities

- Organization Officer: Ensures accurate and truthful information before signing.

- Electronic Return Originator (ERO): Responsible for filing the return electronically and maintaining form compliance.

Steps to Complete the 8879-EO

- Verify Information: Confirm that all data on the organization's return is accurate.

- Review the Return: Check the electronic return for completeness.

- Sign the Form: The organization's officer should sign the form to authorize e-filing.

- Retain for Records: Store the signed form and accompanying documents securely.

Common Pitfalls

- Missing signatures or dates can invalidate the form.

- Ensure accurate information to prevent submission rejection.

How to Obtain the 8879-EO

Form 8879-EO can be accessed directly through the IRS website, ensuring you have the latest version. Organizations can also rely on tax preparation software that supports exemption filings to access and complete the form electronically.

Access Points

- IRS Website: Download the PDF version.

- Tax Software: Use platforms like TurboTax for seamless integration.

Important Terms Related to 8879-EO

- Authorization: Consent given by the officer to file the return electronically.

- ERO: Electronic Return Originator, crucial for handling the e-filing process.

- Exempt Organization: Non-profit entities required to file tax returns but exempt from paying federal income taxes.

Legal Use of the 8879-EO

The 8879-EO supports compliance with the ESIGN Act, making electronically generated signatures legally binding. It outlines the steps required for secure electronic submissions and the retention of evidence of authorization.

Key Legal Notes

- ESIGN Compliance: Electronic signatures must meet legal standards.

- Record Retention: Businesses need not send the form to the IRS, but keeping it for record is vital.

Filing Deadlines / Important Dates

Organizations must ensure the 8879-EO is completed before filing the electronic return. The exact date varies according to the fiscal year but should be aligned with the IRS-specified filing deadline for exempt organization returns.

Critical Timelines

- Regular Fiscal Year: Aligns with IRS tax return deadlines.

- Extension Filers: Adjust based on individual approved extensions.

Required Documents

To correctly complete Form 8879-EO, organizations must gather:

- Completed e-File Tax Return: The exact figures for authorization.

- Authentication Details: For the organization officer, ensuring they are the correct signatory.

- Supporting Documentation: Basis for any claims made in the return.

State-Specific Rules for the 8879-EO

While the IRS administers Form 8879-EO at the federal level, some states have variations in their form requirements or equivalent processes that must be observed.

Navigating State Variations

- Comprehensive Review: Check state-specific additional requirements.

- Unique Filings: Some states require separate electronic filing authorizations.

Examples of Using the 8879-EO

Consider a non-profit organization, ABC Charities, using Form 8879-EO to file its annual tax return electronically. The officer reviews the return for accuracy and authorizes the e-filing, ensuring organizational compliance without mailing physical documentation to the IRS.

Real-World Scenarios

- Multi-Signature Environment: Environments where multiple officer signatures are necessary.

- Remote Operations: Non-profits operating remotely benefit from electronic processes.

Penalties for Non-Compliance

Failure to accurately complete or retain Form 8879-EO can result in significant consequences, such as:

- Audit Risks: Increase in audit likelihood without proper authorization records.

- Non-Compliance Penalties: Potential fines for faulty or incomplete filings, emphasizing the need for diligent completion and record maintenance.