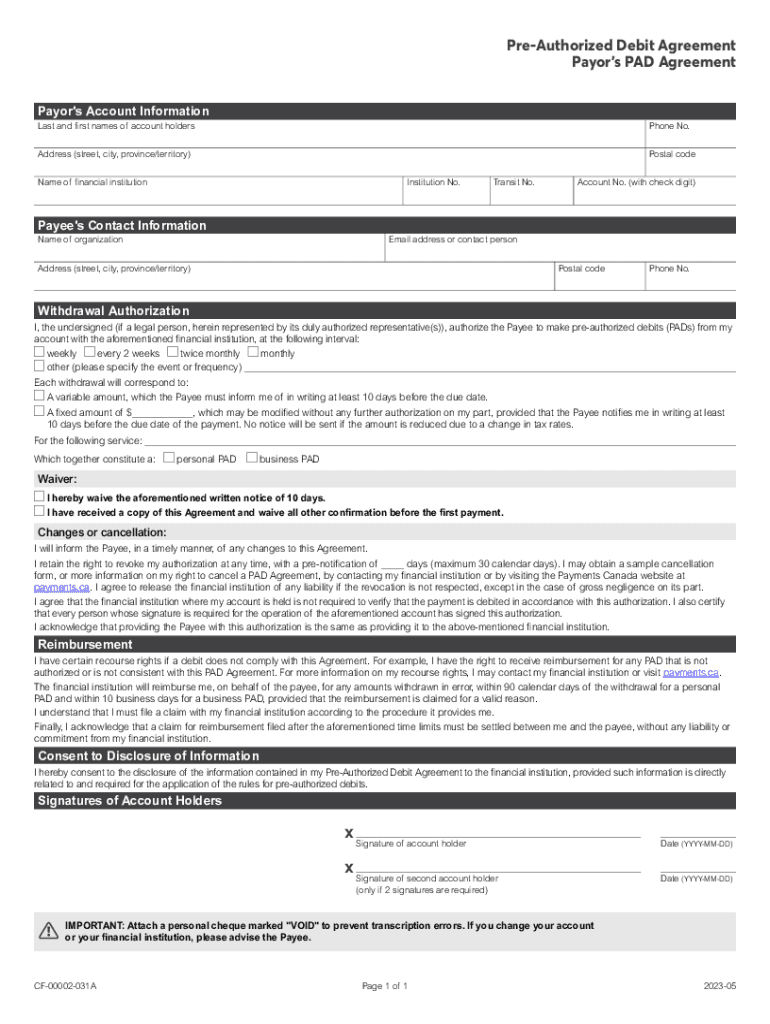

Definition and Purpose of the Pre-Authorized Debit (PAD) Payor Agreement

The Pre-Authorized Debit (PAD) Payor Agreement is a form that facilitates recurring payments from a payor's bank account to a payee. This agreement allows the payee to automatically withdraw specified amounts at agreed intervals, ensuring timely payments for services like utilities, loans, or subscriptions. It is commonly used by businesses to streamline billing processes and reduce the administrative burden associated with manual payment collections. The agreement aims to simplify financial transactions by automating payments, which ensures that obligations are met without requiring active monthly intervention from the payor.

How to Use the Pre-Authorized Debit (PAD) Payor Agreement

To effectively utilize the PAD Payor Agreement, the payor must first ensure that their bank supports pre-authorized debits. The payor then completes the form by providing the required personal or business information, such as bank account details, withdrawal amount, and frequency of payments. The payor must sign the agreement to authorize the payee to initiate withdrawals on the scheduled dates. Once completed, it’s recommended to provide a voided check to verify bank account details. After submission, maintaining a record of the agreement is advisable to resolve any potential disputes regarding the payments.

Steps to Complete the Pre-Authorized Debit (PAD) Payor Agreement

-

Gather Required Information:

- Bank account number and routing number.

- Payee details (name, contact information).

- Payment details (amount, start date, frequency).

-

Fill Out Personal or Business Information:

- Ensure accuracy in entering names, addresses, and other pertinent data.

-

Specify Withdrawal Information:

- Enter authorized withdrawal amount and frequency.

-

Read and Agree to Terms:

- Carefully review terms regarding cancellation, data sharing, and rights to reimbursement for unauthorized transactions.

-

Attach a Voided Check:

- Provide a voided check to confirm the bank account details.

-

Sign the Agreement:

- Ensure all authorized account holders have signed.

-

Submit the Agreement:

- Send to the payee as per their submission instructions, maintaining a copy for your records.

Key Elements of the Pre-Authorized Debit (PAD) Payor Agreement

- Payor and Payee Information: Clearly identified personal or business details of both parties involved.

- Banking Details: Precise bank account information including account and routing numbers.

- Withdrawal Terms: Specifies the amount, frequency, and start date of debits.

- Authorization and Consent: Sections where the payor signs to authorize the transactions.

- Cancellation Rights: Information on how and when the payor can cancel the agreement.

- Reimbursement Provisions: Details the procedure to claim refunds for unauthorized debits.

Legal Use and Compliance with the Pre-Authorized Debit (PAD) Payor Agreement

The PAD Payor Agreement must comply with applicable U.S. federal regulations, such as the Electronic Funds Transfer Act, which governs electronic transactions. Payors have legal rights to dispute unauthorized transactions and must be informed about these rights within the agreement. Legal compliance requires the clear presentation of terms regarding cancellation and reimbursement procedures. Both parties must retain a copy of the signed agreement to address compliance issues efficiently.

Important Terms Related to the Pre-Authorized Debit (PAD) Payor Agreement

- Authorized Payee: The entity or individual entitled to withdraw funds.

- Authorization Period: The period during which the agreement remains active.

- Notice of Change or Cancellation: Advanced notification requirement for altering or terminating the agreement.

- Void Check: A check rendered void by striking across it, used to verify bank details.

- Automatic Payment: Recurring payment without manual intervention from the payor.

Who Typically Uses the Pre-Authorized Debit (PAD) Payor Agreement

The PAD Payor Agreement is widely used by businesses, financial institutions, and individuals for efficient financial transactions. Businesses leverage it to secure timely payments from clients for services or products offered on a subscription or credit basis. It is particularly beneficial for companies providing ongoing services, such as utility providers, insurance companies, and lenders. Individuals use this form to simplify recurring payments for loans, subscriptions, and utility bills, among other expenses.

Benefits and Challenges of Using Pre-Authorized Debit (PAD) Payor Agreement

Benefits

- Convenience: Automates payments, reducing manual interventions.

- Timeliness: Ensures payments are made on schedule, avoiding late fees.

- Reduced Workload: Lowers administrative efforts in payment processing.

Challenges

- Authorization Risks: Requires trust in the payee’s integrity.

- Cancellation Complexity: May involve procedures to terminate the agreement.

- Dispute Resolution: Potential complications in reclaiming unauthorized payments.

Steps to Modify or Cancel the Pre-Authorized Debit (PAD) Payor Agreement

-

Review Agreement Terms:

- Check the terms on how to modify or cancel the agreement.

-

Provide Notification:

- Inform the payee in writing of your intent to change or cancel the agreement, adhering to notice periods prescribed.

-

Follow Payee's Process:

- Utilize the payee’s specified procedures for modifications or cancellations.

-

Confirm Changes:

- Obtain confirmation from the payee that the agreement has been amended or terminated as requested.

-

Notify Your Bank:

- Inform your bank of the changes to preempt any unauthorized withdrawals.

By adhering to these guidelines and understanding the nuances of the PAD Payor Agreement, users can efficiently manage their recurring payments while safeguarding their financial interests.