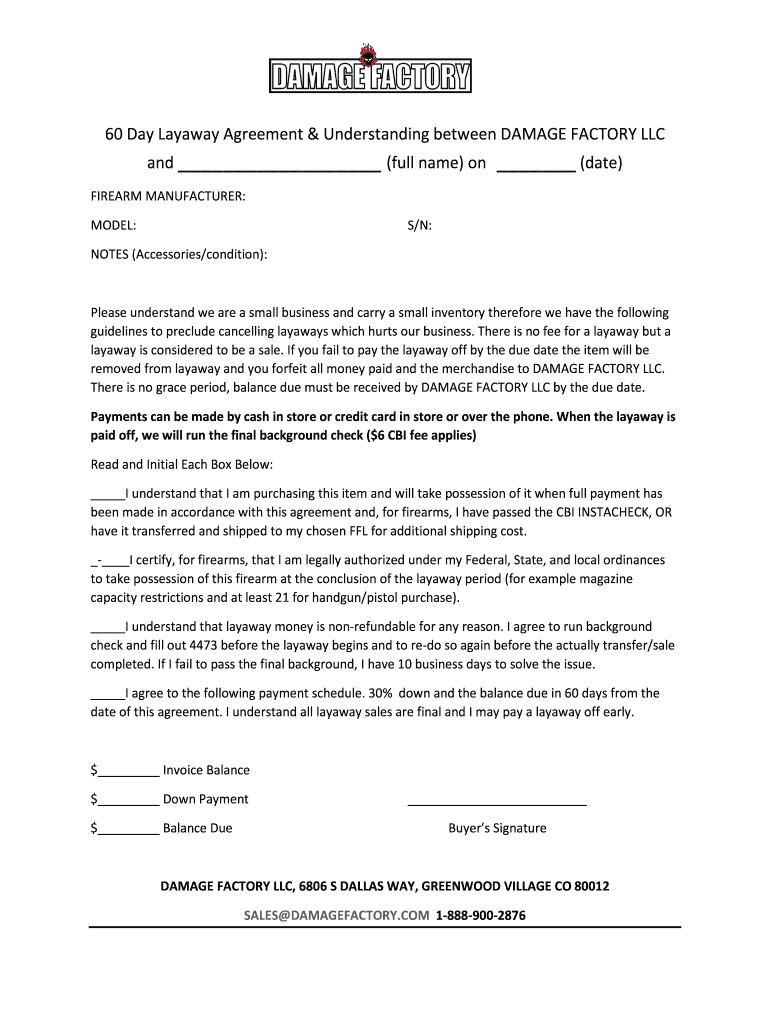

Definition and Meaning

A "60 Day Layaway Agreement - Damage Factory" is a contractual arrangement between DAMAGE FACTORY LLC and a buyer, designed to facilitate the purchase of a firearm. This agreement allows a buyer to reserve a firearm by making regular payments over 60 days. Unlike traditional purchase arrangements, this layaway deal treats each payment as part of the eventual sale, rather than as a simple deposit. If the buyer fails to complete all payments within the designated timeframe, the agreement stipulates that all payments made will be non-refundable.

Layaway agreements in general are beneficial for both the seller and buyer as they provide flexibility in payments while securing the desired item for the customer. In the context of a firearm purchase, it includes stipulations regarding required background checks and the buyer's legal eligibility to own firearms.

How to Use the 60 Day Layaway Agreement - Damage Factory

To effectively use this agreement, the buyer should start by selecting the desired firearm from DAMAGE FACTORY's available inventory. They must review the layaway terms and conditions carefully to understand payment schedules and other essential requirements:

- Payment Schedule: The agreement will outline the specific payment amounts and due dates across the 60-day period.

- Legal Compliance: Buyers must comply with any background checks and legal requirements associated with purchasing a firearm.

- Completion of Purchase: All payments must be completed by the end of the 60-day period to finalize the purchase.

Buyers are advised to keep track of their payment deadlines to ensure they can fulfill the agreement terms without financial strain.

Steps to Complete the 60 Day Layaway Agreement - Damage Factory

- Select the Firearm: Choose the desired firearm from DAMAGE FACTORY’s inventory.

- Review Agreement Terms: Go through the layaway agreement to understand payment terms and legal requirements.

- Initiate Layaway: Begin by making the initial payment as specified in the agreement.

- Complete Background Checks: If required, consent to and complete any necessary background checks.

- Make Scheduled Payments: Follow the payment schedule, ensuring that payments are made by the due dates.

- Fulfill Legal Requirements: Ensure that all legal obligations are met regarding firearm ownership.

- Finalize the Purchase: Once all payments are made and legal checks completed, the firearm ownership is transferred to the buyer.

Key Elements of the 60 Day Layaway Agreement - Damage Factory

This agreement includes several critical elements that buyers must be aware of:

- Non-Refundable Payments: Payments made are non-refundable if not completed within the timeframe.

- Background Check Requirements: Legal stipulations for purchasing firearms must be met.

- Payment Structuring: Details on payment intervals and amounts need strict adherence.

Recognizing these elements is essential for successfully navigating through the agreement.

Legal Use of the 60 Day Layaway Agreement - Damage Factory

The legal aspect of this agreement is vital, especially concerning firearm transfer laws. The agreement complies with all U.S. regulations surrounding the sale and ownership of firearms.

- Eligibility Verification: The buyer must be legally eligible to purchase a firearm, adhering to both federal and state laws.

- Contract Enforcement: This document upholds the contractual obligations, legally binding both parties to the stated terms.

Buyers should consult with legal experts if they have questions regarding their eligibility or the agreement's implications.

State-Specific Rules for the 60 Day Layaway Agreement - Damage Factory

Firearm purchase regulations can vary by state, making state-specific understanding imperative:

- Varied Background Check Requirements: Certain states might have additional checks or waiting periods.

- State Compliance: The agreement ensures compliance with not only federal but also state-specific firearms regulations.

Buyers should familiarize themselves with both federal laws and their specific state laws when entering into the agreement.

Who Typically Uses the 60 Day Layaway Agreement - Damage Factory

Such agreements are particularly advantageous for:

- Hobbyists or Collectors: Individuals looking to spread the financial burden over time while securing an item.

- Budget-Conscious Buyers: Customers who want to manage finances by distributing the total cost over several payments.

This target group finds layaway plans beneficial as it provides financial flexibility without accumulating interest, unlike conventional credit arrangements.

Important Terms Related to the 60 Day Layaway Agreement - Damage Factory

Understanding key terms related to the agreement is crucial for clear comprehension:

- Layaway: A payment arrangement that allows consumers to reserve an item by placing regular installments.

- Non-Refundable: Payments that cannot be returned if the buyer fails to complete the purchase.

- Firearm Eligibility: Legal criteria that a prospective buyer must satisfy to own a firearm.

Familiarizing oneself with these terms ensures a smoother process and clearer understanding of the agreement's requirements.