Definition & Meaning

The Loan Agreement Promissory Note - State Bar of Texas is a legally binding document used to outline the terms and conditions of a loan agreement between a borrower and a lender within the state of Texas. This document sets the framework for financial transactions by detailing the amount borrowed, interest rate, repayment schedule, and additional legal provisions. It serves as a crucial tool for both parties to ensure clarity and legal enforceability of the loan arrangement.

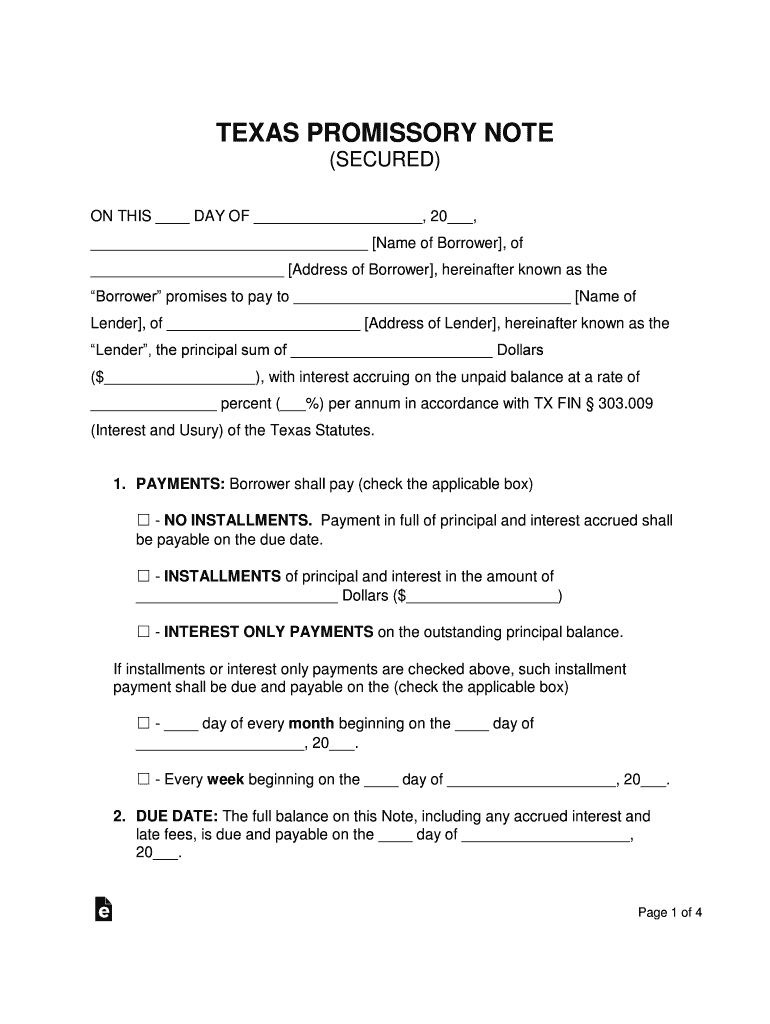

Key Elements of the Loan Agreement Promissory Note - State Bar of Texas

- Principal Amount: Defines the total sum borrowed by the borrower from the lender.

- Interest Rate: Specifies the percentage charged on the outstanding principal, reflecting the cost of borrowing.

- Payment Schedule: Outlines the timeline and frequency of installments that the borrower must adhere to for repaying the loan.

- Collateral: Assets pledged by the borrower to secure the loan, offering protection to the lender in case of borrower default.

- Acceleration Clause: A provision allowing the lender to demand immediate repayment if the borrower defaults.

These components ensure both parties have a clear understanding of their obligations and protect their interests under Texas law.

Steps to Complete the Loan Agreement Promissory Note - State Bar of Texas

- Identifying the parties: Clearly state the names and contact information of the borrower and the lender.

- Detail the loan amount: Include the principal sum borrowed, ensuring it matches both parties’ records.

- Establish the repayment terms: Set precise dates for payment installments and specify whether payments will be monthly, quarterly, or annually.

- Specify the interest rate: Document the agreed-upon interest rate and any applicable conditions.

- Outline collateral agreements: If secured, detail the assets used as collateral, including any valuation considerations or conditions for release.

- Include signatures and date: Ensure both parties sign and date the document for it to be considered legally binding.

- Legal review and notarization (if necessary): It may be prudent to have the document reviewed by a legal professional and notarized to ensure compliance with state laws.

Important Terms Related to Loan Agreement Promissory Note - State Bar of Texas

- Default: Failure by the borrower to meet the terms set out in the loan agreement.

- Prepayment: Payments made in advance of the due date, which may be subject to specific terms regarding reduction in interest or penalties.

- Usury Laws: State-specific laws governing the maximum permissible interest rates on loans to prevent exorbitant charges.

These terms are vital for understanding the rights and obligations within the note and for ensuring compliance with state regulations.

Legal Use of the Loan Agreement Promissory Note - State Bar of Texas

This form serves as a foundational document under Texas law to provide legal clarity and protection for all involved parties in a loan agreement. By adhering to its stipulations, both lenders and borrowers can ensure their transactions are recognized by the court system, thus offering a legal remedy in case of disputes or defaults.

State-Specific Rules for the Loan Agreement Promissory Note - State Bar of Texas

Texas imposes specific regulations governing the formation and execution of promissory notes. These include compliance with the Texas Finance Code and Usury Laws that control the maximum rate of interest that can be charged. It is crucial for parties to familiarize themselves with these rules to avoid inadvertently creating an unenforceable agreement.

Software Compatibility

In terms of digital compatibility, the Loan Agreement Promissory Note - State Bar of Texas can be handled using various document processing software. Platforms like DocHub provide comprehensive support for creating, editing, and signing legal documents such as promissory notes. This compatibility ensures ease of use and integration within digital workflows.

Examples of Using the Loan Agreement Promissory Note - State Bar of Texas

Common scenarios include personal loans between family members, business financing, or lending between friends. Each scenario will have its nuances, but the promissory note provides a tool for clearly delineating the terms and ensuring the enforceability of the agreement in Texas.

Penalties for Non-Compliance

Non-compliance with the terms specified in the loan agreement can lead to severe penalties, including acceleration of the payment schedule or seizure of collateral. Legal action may also be pursued by the aggrieved party, potentially resulting in a court order for repayment and additional damages or fines in accordance with Texas law.