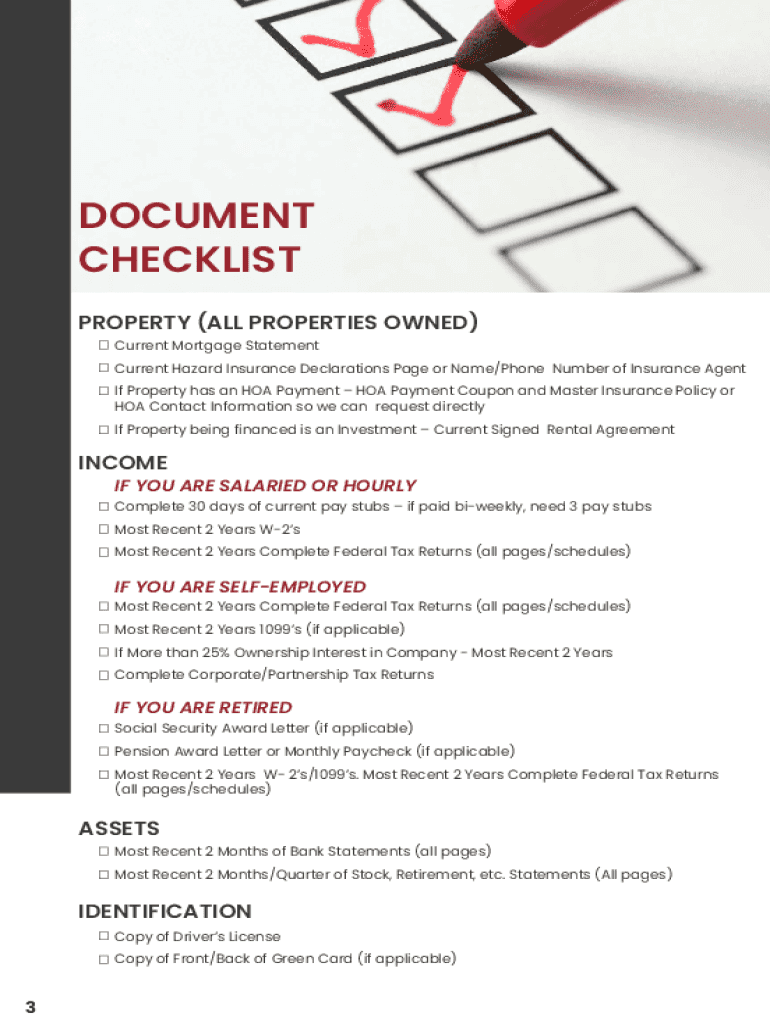

Definition and Purpose of the Home Buying Checklist for First-Time Home Buyers

The "Home Buying Checklist for First-Time Home Buyers" is a detailed resource designed to assist individuals entering the property market. This checklist provides a structured guide to navigating the complexities of purchasing a home, ensuring that all essential steps are completed for a successful transaction. It encompasses financial readiness, property search criteria, and final closing arrangements, serving as an essential tool for both organization and compliance with standard home-buying procedures. With precise attention to detail, this checklist also includes elements specific to first-time homebuyers, offering tailored advice and support.

Using the Home Buying Checklist for Maximum Efficiency

First-time homebuyers can optimize their use of the checklist by following a sequential approach, breaking down the home-buying process into manageable steps. This involves:

- Financial Preparation: Review financial health, including credit scores and budgeting for a down payment and other costs.

- Property Search: Identify key features and areas of interest, utilize online tools for property comparisons, and schedule viewings.

- Offer and Negotiation: Understand the current real estate market to make competitive offers and engage in price negotiations.

- Closing Procedures: Ensure all legal and financial documents are finalized and complete mandatory inspections.

Each aspect of the checklist aims to prevent common pitfalls by fostering a comprehensive understanding of requirements and timelines.

Steps to Complete the Home Buying Checklist for First-Time Home Buyers

Completing the checklist effectively requires a methodical approach:

- Gather Initial Documentation: Collect necessary personal information like identification documents, proof of income, and credit history.

- Conduct Market Research: Utilize local real estate listings and market analyses to familiarize yourself with property values.

- Secure Financing: Shop for lenders, compare mortgage options, and get pre-approved to understand your borrowing capacity.

- Engage Real Estate Professionals: Hire a reputable real estate agent and possibly a real estate attorney for specialized guidance.

- Perform Due Diligence: Have properties of interest appraised and inspected to assess condition and value.

- Finalize Purchase: Coordinate the signing of the purchase agreement, secure homeowner's insurance, and prepare for closing day.

These steps ensure a thorough and informed approach to buying a home for the first time.

Key Elements of the Checklist

Critical elements incorporated in the checklist include:

- Financial Readiness: Budgeting, credit checks, and understanding mortgage pre-approval.

- Property Criteria and Viewings: Checklists for evaluating property features, neighborhood amenities, and potential renovations.

- Legal Documentation: Necessary legal documents like purchase agreements, disclosures, and inspection reports.

These components are essential for navigating the home-buying process with confidence and accuracy.

Important Terms in Home Buying

Understanding specific real estate terminology is crucial:

- Earnest Money: A deposit made to demonstrate serious intent to purchase a property.

- Closing Costs: Fees required to complete a real estate transaction, including taxes, insurance, and lender fees.

- Escrow: A third-party service that holds funds and documents until conditions are met for a transaction.

Acquaintance with these terms will aid in comprehending agreements and negotiations.

Legal Aspects and Compliance

Homebuyers must comply with pertinent legal requirements, ensuring adherence to federal and state housing laws. Essential actions include:

- Reviewing Legal Documents: Thoroughly examine contracts and disclosures.

- Understanding Title Insurance: Protect against losses from defects in the property’s title.

- Adhering to Fair Housing Laws: Acknowledge anti-discrimination policies during property negotiations.

These legalities ensure a fair and lawful home-buying experience.

Examples of Using the Checklist Effectively

Real-world application of the checklist involves scenarios like:

- Budget Management: Tailor a savings plan based on guidance from the checklist to facilitate a larger down payment.

- Negotiation Techniques: Utilize checklist strategies to confidently negotiate with sellers based on market research.

- Problem-Solving: Resolve potential issues flagged during inspections by referring to checklist recommendations for repairs or credits.

These practical applications highlight the checklist’s utility in overcoming challenges faced by first-time buyers.

State-Specific Considerations

The checklist accounts for variations in real estate practices across different states. Highlighted areas include:

- Property Taxes: Understanding local property tax rates and applicable deductions.

- Zoning Regulations: Familiarity with state-specific zoning laws affecting property use.

- Disclosure Requirements: Knowledge of state-mandated disclosure forms sellers must provide.

Buyers should research state-specific information to align their buying process with regional laws and standards.