Definition & Meaning

The Paid-Up Life Insurance or Surrender Request form is pivotal for participants in a Group Variable Universal Life Insurance program. This form facilitates the termination of one’s involvement in the life insurance plan and provides a structured process for two major actions: cash value withdrawal or purchasing paid-up life insurance. Paid-up life insurance allows you to use the accumulated cash value to buy a smaller policy that requires no further premium payments, while a surrender request typically terminates the policy altogether, releasing any cash value.

How to Use the Paid-Up Life Insurance or Surrender Request

Utilizing this form requires a good understanding of its two primary functions: opting for paid-up life insurance or outright surrender. Participants begin by reading the instructions carefully, as these guide the completion of the form. Specifying whether one wishes to maintain a paid-up policy or withdraw cash is essential, and each choice has different implications. If opting for cash value withdrawal, the individual must decide whether to receive the funds directly or apply them toward another financial product.

Steps to Complete the Paid-Up Life Insurance or Surrender Request

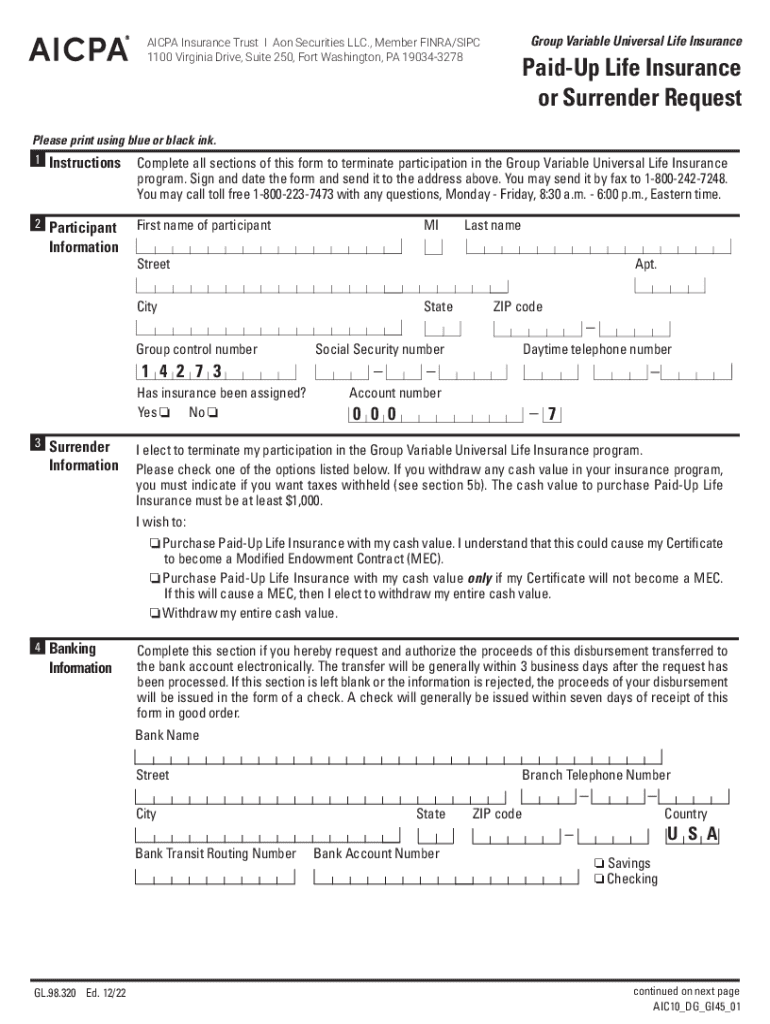

- Personal Information: Begin by providing accurate personal details including full name, current address, and contact information. Ensure that all information is up-to-date to avoid delays.

- Decision Selection: Clearly indicate your preference between cash value withdrawal or converting to a paid-up life insurance policy.

- Banking Details: For those choosing cash withdrawal, provide banking information for electronic transfer to ensure timely receipt of funds.

- Tax Certification: Complete the taxpayer identification certification to comply with IRS requirements, which confirm your status and potential withholding needs.

- Signature and Date: Sign and date the form as a legal acknowledgment of your decision and the accuracy of provided information.

Why Should You Submit a Paid-Up Life Insurance or Surrender Request

Submitting this form is crucial when you decide it’s time to reassess your life insurance needs. For some, maintaining paid-up life insurance offers ongoing coverage without future payments. For others, withdrawing the policy’s cash value could meet immediate financial needs or support alternative investment opportunities. This form is also essential for those wishing to terminate their insurance participation due to changes in financial circumstances or shifting life goals.

Key Elements of the Paid-Up Life Insurance or Surrender Request

Several components define this form’s structure, ensuring a seamless transition whether you're selecting cash withdrawal or paid-up life insurance:

- Participant Identification: Ensures you are accurately identified as the policyholder.

- Withdrawal Instructions: Details your choice of action regarding the policy.

- Banking and Tax Information: Ensures compliance with financial regulations.

- Signature Line: Legalizes your request and confirms all entries are correct.

Required Documents

When preparing to submit this form, gather the necessary documents to minimize processing delays:

- Identity Proof: Government-issued ID as verification.

- Current Policy Statement: For reference to your insurance details.

- Bank Account Details: To facilitate any cash withdrawals.

- Tax Identification Documents: As proof of compliance with IRS guidelines.

Form Submission Methods

The form can be submitted through several channels, depending on your convenience and urgency. Options typically include:

- Online Submission: Through secure insurance provider portals, ensuring instant confirmation of receipt.

- Mail: Traditional postal mail, though slower, confirms submission through tangible records.

- In-Person: Visiting a branch office can provide immediate attention, advice, or correction of potential errors.

Legal Use of the Paid-Up Life Insurance or Surrender Request

This form serves a legal purpose beyond administrative convenience. It allows policyholders to exercise their rights within the terms stipulated by their insurance contract. This process is governed by both state and federal laws, which dictates full transparency and informed decision-making. Legal use also involves fulfilling all statutory reporting requirements and cooperating with the insurance provider to ensure fair and efficient processing.

Who Issues the Form

Typically, the form is issued by the life insurance company who manages your Group Variable Universal Life Insurance policy. This ensures form authenticity and alignment with the provider’s administrative systems. Each insurer might have slightly different versions of the form, reflecting their processing procedures and compliance needs.