Definition & Purpose of the FR-900M Form

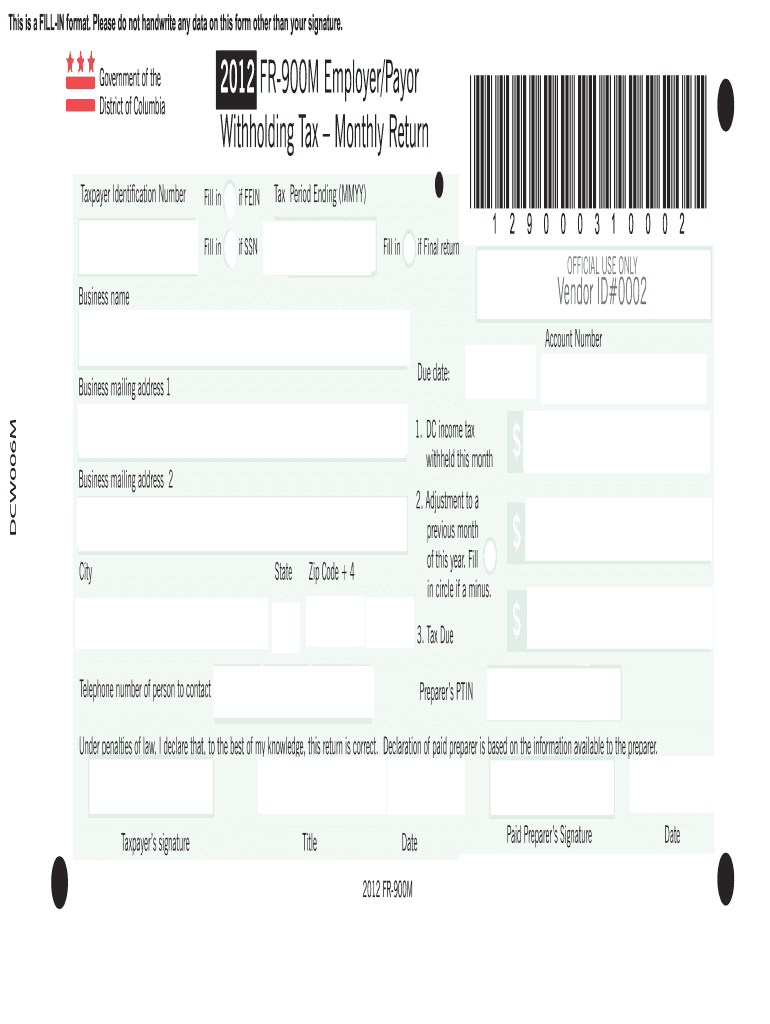

The FR-900M, formally known as the "Employer/Payor Withholding Tax Monthly Return," is a crucial tax document for employers operating within the District of Columbia. The primary purpose of this form is to report and remit the withheld income taxes from employees' salaries monthly. By doing so, businesses fulfill their tax obligations to the D.C. government, ensuring compliance with local tax laws. It's essential for maintaining accurate financial records and avoiding potential legal issues arising from withholding tax mismanagement.

Key Components of the FR-900M Form

- Identification Number: Employers must provide their unique identification number, which links the entity to the tax return.

- Business Details: Must include the legal name, address, and contact information of the business filing the form.

- Tax Period: Clearly state the specific month for which the taxes are being reported.

- Income Tax Withheld: Disclose the total amount of income tax withheld from all employees' salaries during the reporting period.

- Adjustments and Tax Due: Include any necessary adjustments and calculate the total tax due after adjustments.

Steps to Complete the FR-900M Form

Completing the FR-900M form accurately is vital for ensuring compliance and avoiding penalties. Here is a step-by-step guide to assist you:

- Gather Necessary Information: Before starting, collect all relevant data, such as employee payroll records, total wages paid, and tax amounts withheld.

- Fill in Business Identification Details: Accurately enter your business identification number and official business name as registered.

- Report the Tax Period: Clearly specify the month and year for which you're reporting taxes.

- Enter Withholding Details: Record the total amount of income tax withheld from employee salaries for the specified month.

- Calculate Adjustments: Make any necessary adjustments, such as corrections from previous filings, and record the adjusted tax amount.

- Determine Total Tax Due: Subtract any previous payments or credits applied from the total tax withheld to determine the tax due.

- Review and Sign: Carefully review the entire form for accuracy and completeness. Once verified, an authorized person should sign the document.

Filing Deadlines and Important Dates

Timely submission of the FR-900M form is critical to maintaining compliance. The form must be submitted by the 20th day of the month following the reporting period. For instance, the return for July is due by August 20. Failing to meet this deadline can result in penalties and interest charges.

Penalties for Late Submission

- Penalty Charges: Late filings incur a penalty of 5% per month, up to a maximum of 25% of the unpaid tax.

- Interest Rates: Interest is charged on any unpaid tax amount at the rate specified by D.C. tax regulations, compounded daily.

Digital vs. Paper Version

The FR-900M can be submitted either digitally or via a paper version. Both methods serve the purpose of reporting taxes, though each has unique advantages:

- Digital Submission: Offers a faster, more efficient way of filing, ensuring timely delivery and reduced risk of lost paperwork. This method is often integrated with payroll software for seamless data transfer.

- Paper Submission: Offers a traditional approach, usually preferred by businesses with minimal digital involvement. It involves mailing the completed form to the specified D.C. tax office address.

Software Compatibility

Many employers leverage software solutions such as QuickBooks or TurboTax to streamline the FR-900M filing process. These platforms support form generation, calculation of withholdings, and submission, making them invaluable for businesses handling extensive payroll operations.

Who Typically Uses the FR-900M Form

The FR-900M is predominantly used by employers who withhold income tax from employee wages in D.C. This includes various business types such as:

- Corporations: Large and small businesses that manage significant employees and payroll operations.

- LLCs and Partnerships: Smaller businesses and collaborations that have opted for monthly tax reporting cycles.

- Non-Profit Organizations: Entities employing staff within the district and responsible for withholding obligations.

Eligible Business Entity Types

- Sole Proprietorships: While often less complex, sole proprietors employing staff must also file the FR-900M.

- Franchises: These often larger-scale operations within D.C. need to adhere to monthly filing for accurate tax withholding.

Important Terms Related to the FR-900M

Understanding key terms is essential for accurately completing the FR-900M form:

- Withholding Tax: The income tax withheld from employee wages to be paid to the government.

- Identification Number: A unique number assigned to a business for tax purposes, similar to an EIN.

- Payroll Adjustments: Corrections made to previously reported wages or tax withheld.

Legal Use of the FR-900M Form

The FR-900M must be used in accordance with D.C. tax laws, which require employers to accurately report and pay withholding taxes monthly. Misuse, misreporting, or failure to file can lead to significant legal repercussions, including fines and potential audits.

State-Specific Rules for the FR-900M Form

The FR-900M is specific to the District of Columbia and is subject to state-specific tax laws:

- Tax Rates: Compliance with the withholding tax rates as determined by D.C. regulations.

- Mandatory Electronic Filing: Certain businesses may be required to file electronically based on the volume of withholding taxes.

- Record Keeping Requirements: Businesses must maintain detailed records of payroll and withholding data for future audits or verification by the state's tax authority.

State-by-State Differences

Businesses operating both in D.C. and other states must be aware of the differences in filing requirements, as regulations can vary significantly. Multi-state operations should maintain separate records and ensure compliance with each state’s tax laws.