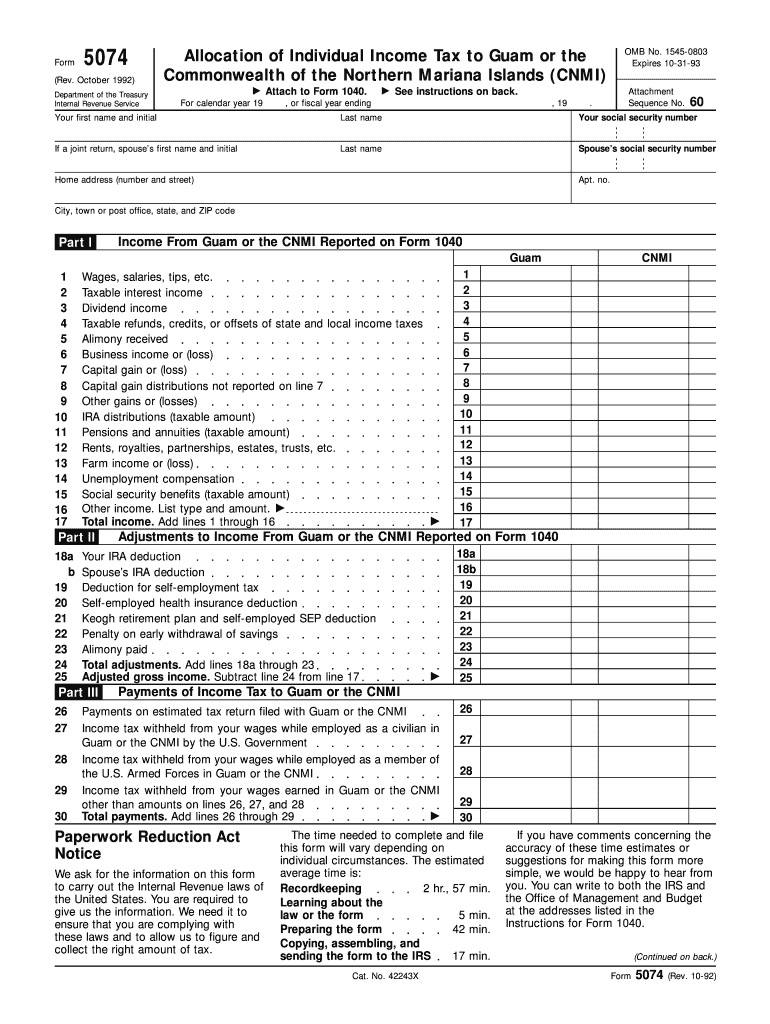

Definition and Purpose of Form 5074

Form 5074, titled "Allocation of Individual Income Tax to Guam or the Commonwealth of the Northern Mariana Islands (CNMI)," serves a specific function for U.S. taxpayers reporting income from these territories. The form assists individuals in dividing their U.S. income tax obligations between the mainland and either Guam or CNMI, according to income sourced from these regions. This allocation is essential to accurately reflect the taxpayer’s financial responsibilities and ensure compliance with both U.S. and territorial tax regulations.

Steps to Complete Form 5074

Successfully completing Form 5074 involves several critical steps that help in accurately reporting income:

-

Gather Necessary Information:

- Collect all income documents, including W-2s, 1099s, and any other records of income sourced from the mainland U.S., Guam, or CNMI.

- Ensure you have your previous year's tax returns and any documentation related to territorial income.

-

Determine Income Allocation:

- Identify income earned in Guam or CNMI separately from the rest of your U.S. income.

- Use your financial documentation to determine exact figures.

-

Complete the Form Details:

- Fill out the personal information, including your name, Social Security Number, and filing status.

- Enter income details specific to Guam or CNMI as instructed by the form.

-

Attach Required Documents:

- Ensure that you attach Form 5074 to your Form 1040 when filing the tax return.

- Include all relevant supporting documentation that verifies the income figures reported.

Important Terminologies Related to Form 5074

Familiarity with key terms can simplify the process of completing Form 5074:

- Allocation: The process of dividing income between the main U.S. and territorial obligations.

- Territorial Income: Earnings that specifically originate from Guam or CNMI.

- Filing Status: Your tax filing category, such as single, married filing jointly, etc., which affects how income is allocated.

Understanding these terms is fundamental to accurately completing the form and ensuring that income is properly reported according to U.S. and territorial tax laws.

Legal Applications of Form 5074

Form 5074 is legally significant as it ensures compliance with the Internal Revenue Code's stipulations regarding income earned in Guam or CNMI. Filing this document accurately prevents misreporting of income which can lead to penalties or interest charges. Taxpayers must meticulously follow IRS guidelines to allocate income correctly, avoiding potential legal challenges and ensuring the correct application of tax laws.

IRS Guidelines for Form 5074

The IRS provides detailed guidelines to assist taxpayers in accurately filing Form 5074:

- Publication Reference: Refer to IRS publications that detail territorial tax rules.

- Line-by-Line Instructions: Follow the instructions accompanying the form for clarity on entering information.

- Thresholds and Exemptions: Be aware of income thresholds that may necessitate the filing of this form.

Adhering to these guidelines is crucial for proper tax compliance and avoiding potential fines or audits.

Filing Deadlines for Form 5074

Form 5074 must be filed by the standard IRS tax return deadline, typically April 15. When this date falls on a weekend or holiday, the deadline extends to the next business day. Taxpayers who fail to meet this deadline should consider filing for an extension using Form 4868 to avoid late-filing penalties.

Required Documents for Filing

To complete Form 5074 accurately, you must gather the following essential documents:

- W-2s and 1099s: Documentation proving all sources of income.

- Previous Tax Returns: Copies of prior year returns to ensure consistency.

- Territorial Income Proof: Any records specific to income earned in Guam or CNMI.

Having these documents at hand allows for accurate completion and reporting on Form 5074, preventing errors and potential audits.

Digital vs. Paper Submission

Taxpayers can choose between digital or paper submissions when filing Form 5074:

- Digital Submission: Utilize tax preparation software or IRS e-file to submit electronically. This method is faster and typically confirms receipt more quickly.

- Paper Submission: Mail the form along with your completed Form 1040 to the designated IRS address.

Both methods have merits, and the choice often depends on taxpayer preference and comfort with technology. However, electronic submission is often faster and more secure.