Definition and Meaning of Form M-6

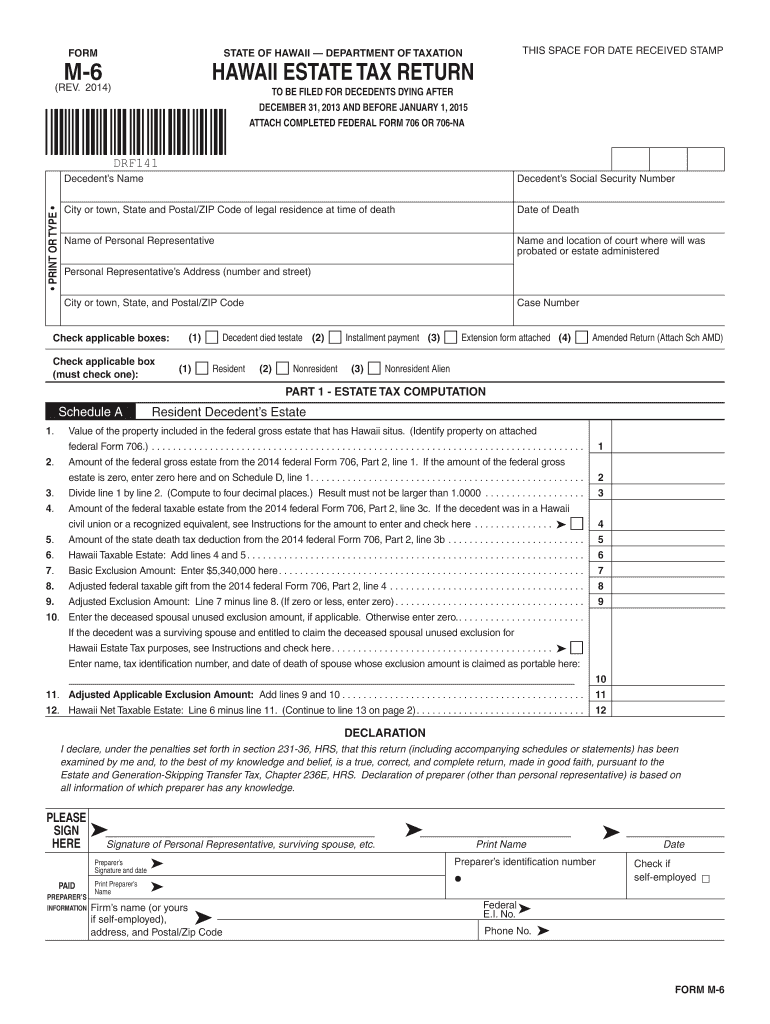

Form M-6, known as the Hawaii Estate Tax Return, is a crucial document used to determine the estate tax liability of decedents in Hawaii. This form is specifically applicable to individuals who passed away between December 31, 2013, and January 1, 2015. The form encompasses various sections where detailed information about the decedent and their estate is recorded to calculate the necessary tax obligations according to Hawaii's estate tax laws.

Steps to Complete Form M-6

-

Gather Required Information: Start by collecting all necessary information about the decedent, including their personal details, date of death, and financial records. This data is pivotal for completing the sections related to the taxable estate.

-

Complete Schedules: The form includes several schedules to calculate the taxable estate value and applicable exclusions. Make sure to work through each schedule carefully, providing all the required details accurately.

-

Calculate Tax Amount: Using the provided instructions, compute the total estate tax liability based on the data entered. This requires a thorough understanding of exemptions and deductions applicable under Hawaii law.

-

Review and Verify: Double-check all the information to ensure accuracy. Mistakes in the form can lead to delays or incorrect tax calculations.

-

Submission: Once completed, the form must be submitted to the Hawaii Department of Taxation. Ensure you are aware of the submission deadline to avoid penalties.

Required Documents for Form M-6

- Death Certificate: A certified copy of the decedent's death certificate is necessary.

- Financial Statements: Complete financial statements reflecting all assets and liabilities of the estate.

- Property Records: Documentation of any real estate or significant properties owned by the decedent.

- Valuations and Appraisals: Professional appraisals or valuations for non-cash assets, such as real estate or collectibles.

- Existing Estate Plans or Wills: Copies of any wills or legal documents related to the decedent’s estate distribution.

Important Terms Related to Form M-6

- Decedent: The individual who has died and whose estate is being taxed.

- Personal Representative: The person responsible for managing the deceased's estate, often named in the will.

- Taxable Estate: The total value of a decedent's assets subject to estate tax after deductions and exemptions.

- Exclusion Amount: A set amount of the estate that is not subject to taxation, which can vary based on state law.

Who Typically Uses Form M-6

Form M-6 is primarily used by personal representatives or executors of estates that include decedents in Hawaii. These individuals are responsible for managing the estate's affairs, ensuring all tax obligations are fulfilled, and distributing assets according to the decedent's wishes or the state's intestacy laws.

State-Specific Rules for Form M-6

Hawaii has specific regulations governing estate taxes, which differ from federal rules. It is essential to familiarize oneself with these state-specific requirements, such as the exemption amounts and particular deductions unique to Hawaii. The Hawaii Department of Taxation provides guidelines to ensure compliance with these local rules.

Filing Deadlines for Form M-6

The Hawaii Estate Tax Return must be filed typically within nine months of the decedent's date of death. It is crucial to adhere to this deadline to avoid penalties or interest on unpaid taxes. Extensions may be available under certain circumstances but require a formal request.

Penalties for Non-Compliance

Failing to file Form M-6 on time or providing false information can result in significant penalties. These could include fines, additional late fees, or interest on unpaid amounts. In severe cases, incorrect filing can also lead to legal action or a requirement to pay higher taxes than initially determined. It is important to understand the implications of non-compliance and to take necessary steps to ensure accurate and timely submission.