Definition & Meaning

The Connecticut Unrelated Business Income Tax Return, Form CT-990T for 2014, is specifically designed for organizations to report unrelated business income. It serves as a critical tool for ensuring compliance with state tax laws by capturing and calculating income derived from activities not directly related to the organization’s primary exempt purpose. This form is essential for maintaining transparency and accountability in financial reporting to the Department of Revenue Services in Connecticut.

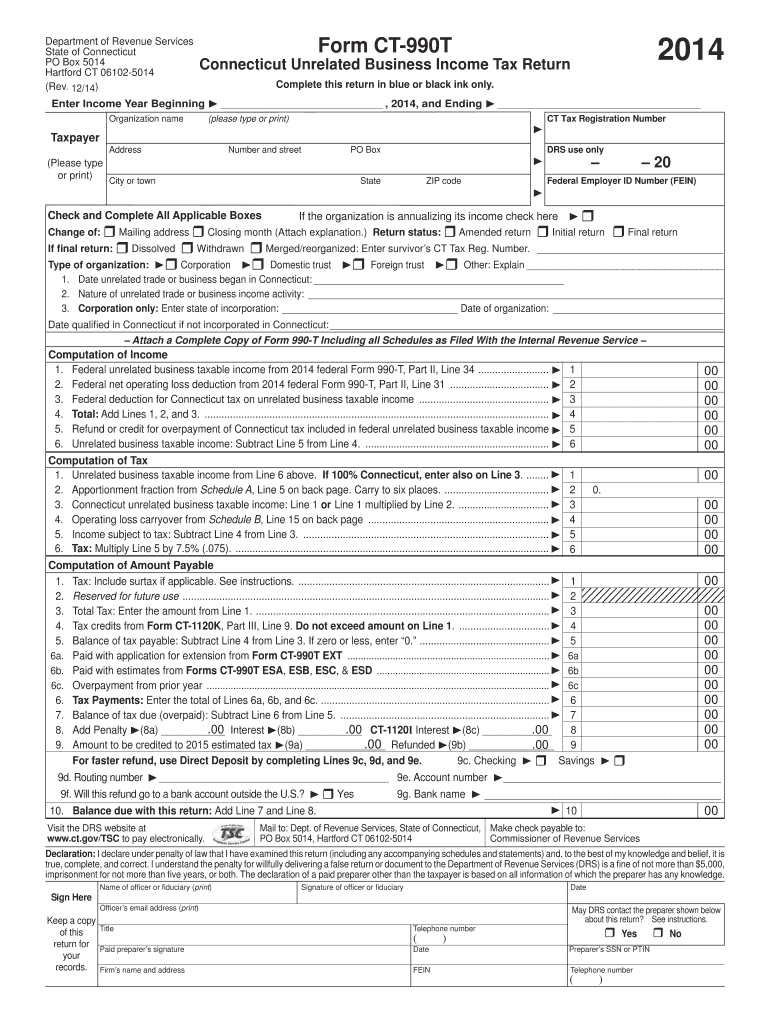

How to Use the Form CT-990T 2014

Organizations must use the form CT-990T 2014 to report unrelated business taxable income (UBTI) originating within Connecticut. The process starts by obtaining the form, filling in organizational details, and accurately reporting income, deductions, and tax computations. Users should ensure they follow all instructions carefully, including referencing federal Form 990-T for consistent data. The form also includes spaces for any modifications specific to Connecticut state tax rules, such as apportionment adjustments.

Steps to Complete the Form CT-990T 2014

- Gather Required Documentation: Before starting, collect financial records, including federal Form 990-T, profit and loss statements, and any relevant apportionment data.

- Fill in Organizational Details: Enter the organization's name, address, and federal employer identification number (FEIN).

- Calculate Unrelated Business Income: Report gross income from unrelated business activities minus applicable deductions.

- Apply Apportionment Calculations: If the organization operates in multiple states, use the form's apportionment schedule to adjust income to reflect business conducted in Connecticut.

- Determine Tax Liability: Utilize the provided instructions to calculate tax owed, considering carryovers and any applicable credits.

- Submit the Form: File with the Connecticut Department of Revenue Services by the deadline to avoid penalties.

Important Terms Related to Form CT-990T 2014

Understanding certain terms is crucial for accurately completing the form:

- Unrelated Business Taxable Income (UBTI): Income from a trade or business regularly carried on, not substantially related to the organization’s exempt purpose.

- Apportionment: A method of computing taxable income for multi-state businesses by assigning income based on business operations within Connecticut.

- Carryovers: Losses or credits from previous years that can reduce taxable income in future years.

Who Typically Uses the Form CT-990T 2014

The form is primarily used by tax-exempt organizations such as charities, universities, and non-profits. These entities engage in business activities not substantially related to their exempt purposes but generate income subject to unrelated business income tax. It enables these organizations to comply with state tax obligations while maintaining non-profit status.

Key Elements of the Form CT-990T 2014

The form comprises multiple sections:

- Identification Information: Details about the organization.

- Income Calculation: Section for detailing gross income from unrelated business activities.

- Deductions and Taxes: Itemization of allowable deductions and calculation of state taxes owed.

- Apportionment: Additional schedules for multi-state organizations to determine taxable income apportioned to Connecticut.

State-Specific Rules for the Form CT-990T 2014

Connecticut imposes unique rules on the calculation and filing of UBTI:

- Apportionment Methods: Specific guidelines on calculating income apportioned to Connecticut.

- Rate of Taxation: Connecticut may have different tax rates or requirements compared to federal calculations, necessitating careful adherence to instructions.

- Filing Requirements: Separate Connecticut filings are mandatory even if a federal filing isn’t needed due to low income or exceptions.

Filing Deadlines / Important Dates

The form must be filed annually, with the 2014 form due on or before the 15th day of the 5th month following the end of the organization's fiscal year. Adhering to deadlines is crucial to prevent incurring penalties or interest charges.

Penalties for Non-Compliance

Failing to file on time or errors in the submission can lead to penalties:

- Late Filing Penalty: Organizations may incur a percentage of tax liability for late submissions.

- Failure to Pay Penalty: Additional charges may apply for taxes not paid by the due date.

- Accuracy Penalties: Misreporting or oversight can trigger penalties unless rectified promptly under state guidelines.