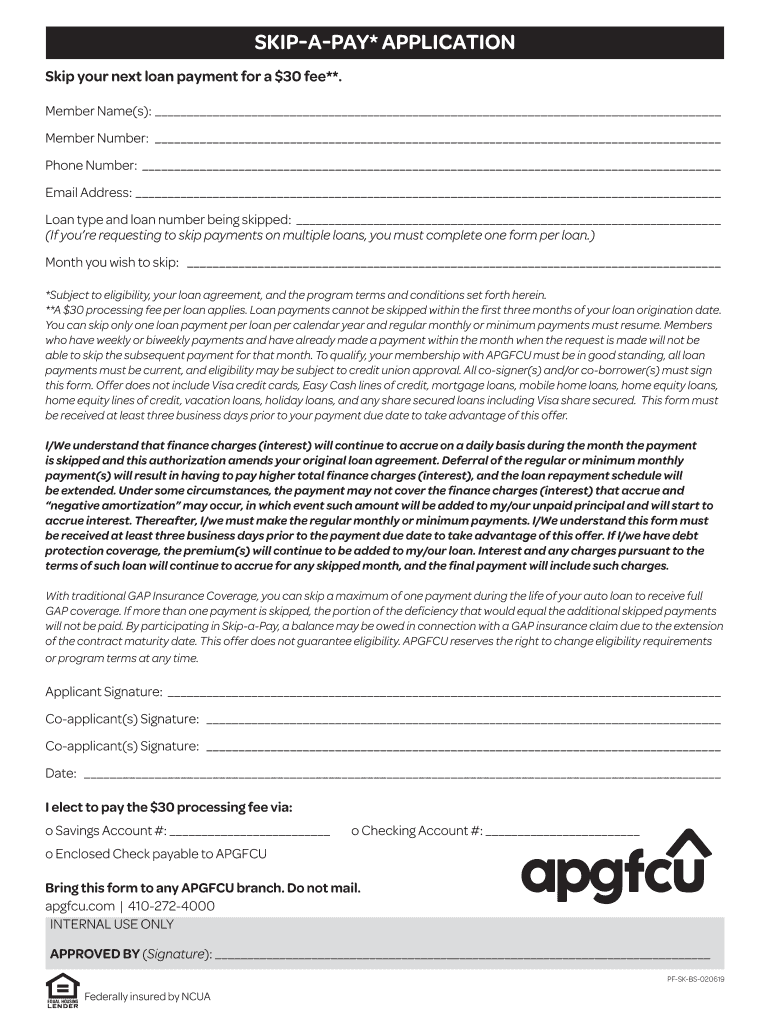

Definition & Meaning

The "Skip your next loan payment for a $30 fee" refers to a financial option offered by certain credit institutions allowing borrowers to defer a scheduled loan payment by paying a nominal processing fee of $30. This option, commonly called "Skip-A-Pay," provides flexibility and temporary financial relief to borrowers who might be facing short-term financial challenges. The program is specifically designed to help manage personal cash flow without defaulting on a loan agreement. However, it's important to note that skipping a payment may lead to continued interest accrual and could result in negative amortization, affecting the total cost of the loan over its lifetime.

How to Use the Skip-A-Pay Program

Using the Skip-A-Pay program involves several steps to ensure compliance with the institution's terms:

-

Review Eligibility: Check with your credit institution to understand the eligibility criteria, such as account standing, loan limits, and the number of payments you can skip annually.

-

Submit Form: Complete the Skip-A-Pay application form, ensuring all required fields are accurately filled. This form must typically be submitted at least three business days before the upcoming payment due date.

-

Acceptance and Fee Payment: Upon review and acceptance of your application, pay the $30 processing fee. This fee is usually non-refundable and may have to be paid directly from your linked account.

-

Confirmation: Await a confirmation from the institution that your payment skip has been processed successfully. Retain this confirmation for your records.

Steps to Complete the Skip-A-Pay Application

Following a meticulous approach when completing the Skip-A-Pay application form is crucial for successful processing:

-

Provide Personal Details: Fill out all personal identification sections, including full name, contact information, and account number.

-

Specify Loan Information: Indicate the loan type, account number, and the specific payment period you intend to skip.

-

Attach Required Documents: Include any documentation that may support your application, such as income statements or any form of financial hardship documentation, if required by the lender.

-

Agree to Terms: Read and acknowledge the program's terms and conditions, confirm understanding of interest accrual impact, and validate your agreement with a signature where required.

Why Consider Skipping Your Loan Payment

There are various reasons why one might opt to skip a loan payment under this program:

-

Cash Flow Management: Temporarily redirect funds toward urgent financial obligations, such as unexpected medical expenses or emergency home repairs.

-

Seasonal Expenses: Align payment schedules with income flow, especially in scenarios where an individual might experience seasonal employment or income fluctuations.

-

Debt Consolidation Strategy: Allow for more strategic debt management as part of a broader financial planning strategy.

Choosing to skip a payment must be part of a well-considered financial plan, as it may extend the loan period and increase interest accrued.

Eligibility Criteria

Eligibility for the Skip-A-Pay program typically involves fulfilling specific criteria set by the lender:

-

Loan Account Currentness: The account must be in good standing, with no outstanding arrears or significant overdue amounts.

-

Limitations on Skips: Generally, only one payment per loan per calendar year is permitted under the program.

-

Loan Types Eligible: Confirm the specific types of loans eligible for this option, which may vary by institution, often excluding mortgages or certain secured loans.

These criteria are designed to ensure that only eligible borrowers who are maintaining adequate financial health are permitted to utilize this option.

Key Elements of the Skip-A-Pay Form

Important aspects of the form include:

-

Personal Information Details: Identity verification and contact information.

-

Loan Account Information: Specifics about the loan, including type and account number.

-

Signature and Acknowledgements: Areas where you agree to the terms and acknowledge understanding of interest implications.

Each element must be accurately provided to prevent delays in processing.

Legal Use and Implications

Using the Skip-A-Pay program involves legal considerations:

-

Contractual Compliance: Skipping a payment must adhere to the terms agreed upon within the loan contract.

-

Interest Accrual: Continued accrual of interest may occur, which the borrower needs to account for in their financial planning.

-

Potential for Negative Amortization: As payments are deferred, this could lead to negative amortization, thereby increasing the loan's overall cost over time.

Understanding these aspects helps ensure informed usage of the service.

Examples of Using the Skip-A-Pay Program

Consider real-world applications of the program:

-

Unexpected Medical Bills: Use the option to redirect funds to cover unexpected out-of-pocket medical expenses momentarily.

-

Temporary Job Loss: Offer breathing room financially during a temporary job loss period, allowing the individual time to seek new employment.

These scenarios depict everyday situations where the program's utilization offers significant short-term financial relief.