Definition & Meaning

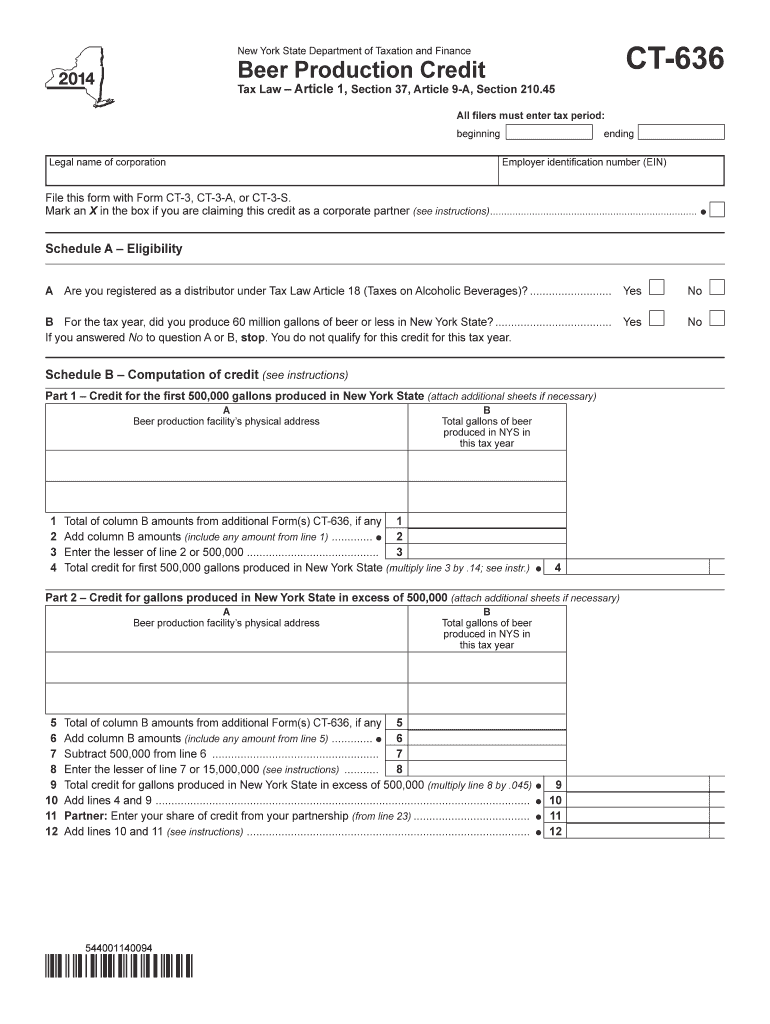

The CT-636 form, issued by the New York State Department of Taxation and Finance, is essential for corporations engaged in beer production within New York. This form is used to claim the Beer Production Credit, an incentive aimed at supporting the beer manufacturing industry by providing tax relief based on production volumes. The form outlines detailed eligibility criteria, which include ensuring the corporation is registered as a distributor and adheres to specific production limits. Understanding this form’s purpose is crucial for companies looking to maximize their tax credits effectively.

Steps to Complete the CT Form

- Gather Required Information: Collect details about your beer production, such as production volumes and distributor registration numbers.

- Fill Out Production Volumes: Input accurate figures relating to the total beer production to calculate the credit.

- Complete Associated Schedules: Integrate information from related corporate tax forms to ensure comprehensive reporting.

- Calculate Credits: Use the guidance provided in the form to compute the precise amount of credit applicable.

- Review for Accuracy: Double-check all entries to avoid errors that might delay the processing of your credit claim.

- Submit with Corporate Tax Forms: Ensure the form is filed in conjunction with your standard corporate tax filings.

How to Obtain the CT Form

Corporations can acquire the CT-636 form through the New York State Department of Taxation and Finance's official website. The form is available for download as a PDF, allowing integration with document management platforms such as DocHub for digital filling and submission. Additionally, the department may provide physical copies upon request for those preferring paper submissions.

Key Elements of the CT Form

- Eligibility Criteria: Detailed requirements for corporations to qualify for the Beer Production Credit.

- Credit Computation: Instructions for calculating the credit based on beer production volumes.

- Production Limits: Specific limits and thresholds that determine credit eligibility and amounts.

- Filing Instructions: Guidelines on how to integrate the form with corporate tax returns.

Eligibility Criteria

Eligibility for using the CT-636 form includes being a corporation registered as a distributor in New York with active beer production operations. The corporation must adhere to statutory production limits and be compliant with all other tax obligations. Understanding these criteria is essential for corporations to determine their qualification for the credit and to effectively manage their tax responsibilities.

Important Terms Related to CT Form

- Beer Production Credit: A tax credit provided to corporations producing beer in New York.

- Distributor: A registered entity responsible for the distribution of beer within state lines.

- Production Limit: The maximum volume of beer that can be produced while remaining eligible for the credit.

Form Submission Methods

Corporations can submit the CT-636 either online through the New York State Department of Taxation and Finance's digital filing services or via mail along with their corporate tax documents. Online submission is often preferred for its speed and efficiency, and platforms such as DocHub can facilitate digital form completion and secure submission.

Penalties for Non-Compliance

Failure to accurately complete and timely submit the CT-636 can result in penalties, including the loss of eligibility for the Beer Production Credit. Non-compliance with requirements such as accurate reporting of production volumes or failure to include the form with corporate tax filings may lead to financial repercussions and additional scrutiny by tax authorities.

Business Types that Benefit Most from the CT Form

Corporations actively involved in beer production within New York State, especially those facing significant tax burdens, benefit greatly from the CT-636 form. The credit helps mitigate financial pressures and supports investments in production capabilities, making it a valuable tool for breweries committed to expansion and competitiveness in the market.

By understanding and utilizing the CT-636 form, eligible corporations can ensure they are maximizing available tax credits while remaining compliant with state regulations.