Definition & Meaning

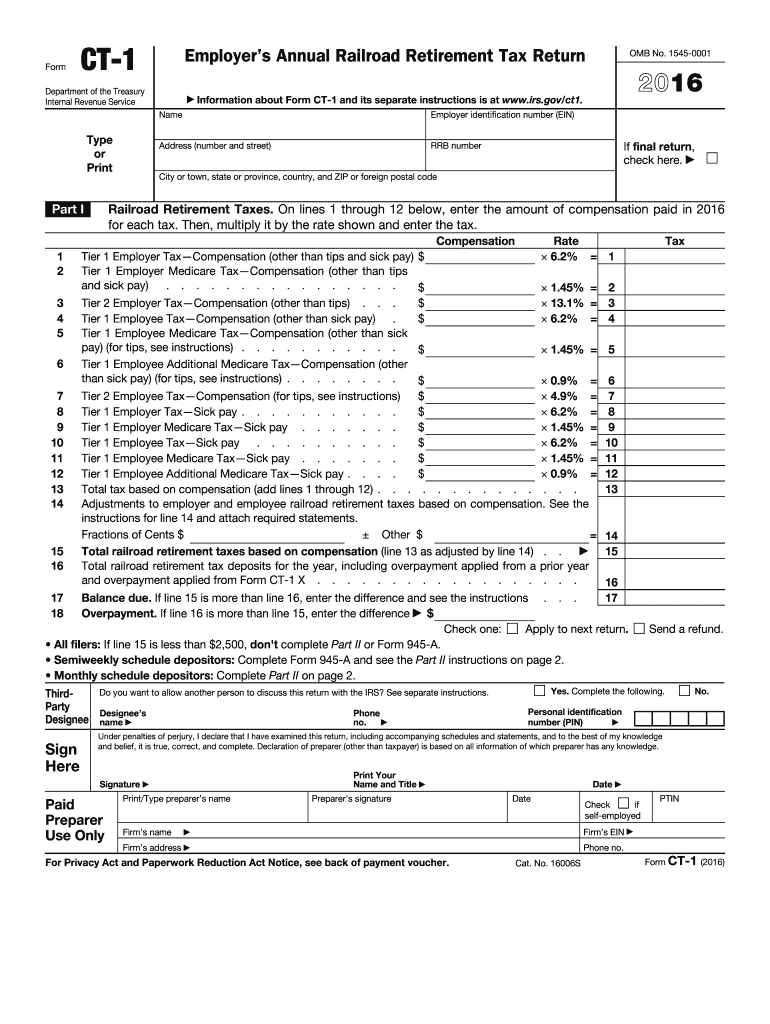

The 2016 Form CT-1, known as the Employer's Annual Railroad Retirement Tax Return, is a specific tax document used by employers within the railroad industry to report taxes related to railroad retirement benefits. This form allows employers to calculate Tier 1 and Tier 2 tax liabilities, ensuring accurate payments toward their employees' retirement benefits under the Railroad Retirement Tax Act (RRTA). The form is crucial for maintaining compliance with federal tax obligations surrounding the unique retirement benefits system of the railroad industry.

How to Use the 2016 Form CT-1 Employer's Annual Railroad Retirement Tax Return

Employers use Form CT-1 to:

- Calculate taxes owed under the RRTA for Tier 1 (Social Security equivalent) and Tier 2 (railroad-specific pension benefits).

- Report compensation paid to railroad employees.

- Determine any balance due or overpayment at the end of the tax year.

Careful attention to detail is necessary to ensure that all compensation is reported accurately and that the correct tax rates are applied. Employers need to follow IRS instructions to complete each section of the form correctly, ensuring compliance with federal regulations.

Practical Example

Consider an employer within the railroad industry who paid $1,000,000 in compensation to employees. They must calculate both Tier 1 and Tier 2 taxes based on this amount, using the rates specified by the IRS for 2016. Accurate reporting on Form CT-1 is essential to avoid any penalties due to underpayment.

Steps to Complete the 2016 Form CT-1 Employer's Annual Railroad Retirement Tax Return

Completing the Form CT-1 involves several critical steps:

-

Gathering Information:

- Collect all necessary payroll records and any previous tax filings related to railroad employment for the 2016 tax year.

-

Calculating Compensation:

- Report total compensation subject to RRTA taxes, ensuring that exemptions and caps are applied correctly.

-

Calculating Tier 1 and Tier 2 Taxes:

- Use the specified tax rates for the year 2016 to determine the amounts owed for both Tier 1 and Tier 2 sections.

-

Reporting Payments:

- Include details of any pre-payments made throughout the year to determine the balance due or refund expected.

-

Review and Submitting:

- Double-check all entries for accuracy and completeness, then send the completed form to the IRS by the specified deadline.

Filing Deadlines / Important Dates

For the tax year 2016, employers must file Form CT-1 by February 28, 2017. This is the deadline to ensure timely filing and avoid penalties for late submissions. If the employer opts to file electronically, Form CT-1 can be submitted by March 31, 2017. These deadlines are crucial to adhere to, as failing to do so can result in significant penalties.

Deadline Variations

While the standard deadline is Feb 28, extensions for filing might be available under certain circumstances, though they must be applied for in advance and justified adequately to the IRS.

Who Typically Uses the 2016 Form CT-1 Employer's Annual Railroad Retirement Tax Return

This form is primarily used by:

- Railroad companies and their subsidiaries.

- Employers who have compensated employees for railroad work within the tax year.

- Businesses responsible for withholding railroad retirement taxes from employee wages.

These entities are obligated to file Form CT-1 to report their tax liabilities derived from employee compensation, in alignment with RRTA requirements.

IRS Guidelines

The IRS provides specific guidelines for completing Form CT-1, which offer detailed instructions on calculating compensation and correctly determining tax liabilities. Key areas covered include:

-

Completing Each Section:

- Detailed instructions are provided for each part of the form, guiding employers through the complex reporting process.

-

Common Pitfalls:

- Identifies frequent errors made during the form's preparation and provides tips on how to avoid them.

Penalties for Non-Compliance

Failure to comply with Form CT-1 filing requirements can lead to significant penalties, including:

-

Late Filing Penalty:

- A percentage of the unpaid tax imposed monthly after the deadline until the form is filed.

-

Accuracy-Related Penalty:

- Applied if the IRS discovers significant errors in the tax reported.

Recognizing the importance of timely and accurate filing, employers must ensure all calculations and entries on Form CT-1 are verified before submission to avoid potential penalties.

Required Documents

To accurately complete Form CT-1, the following documents are typically required:

-

Payroll Records:

- Comprehensive records of all compensated amounts to employees for the tax year 2016.

-

Previous Year Filings:

- Any relevant documents from past filings that might affect current calculations.

-

IRS Forms and Notices:

- Any prior notices or forms received from the IRS that relate to RRTA obligations or previous discrepancies.

Utilizing these documents, employers can ensure the correct completion of Form CT-1, fulfilling their legal obligations while contributing to their employees’ retirement benefits accurately.