Definition & Meaning

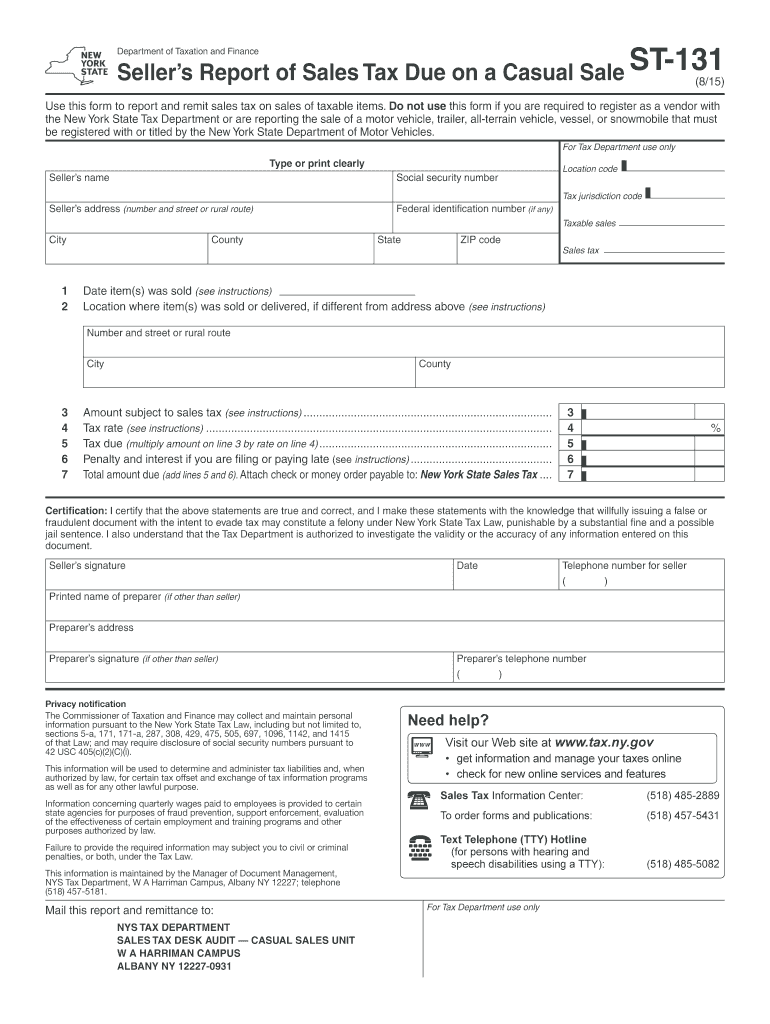

The Form ST-131815, known as the Seller's Report of Sales Tax Due on a Casual Sale, is a crucial document used in New York State for reporting and remitting sales tax on occasional taxable sales by individuals or entities not registered as vendors. This form is specifically designed to ensure compliance with state taxation laws by collecting the necessary sales tax on casual sales, which are typically non-recurring transactions such as the sale of personal items or assets. By filing this form, sellers can avoid potential legal issues while ensuring the state collects all due taxes.

How to Use the Form ST-131815

Using the Form ST-131815 involves several key steps to ensure accurate tax reporting. Sellers must first identify if the sale qualifies as a casual sale under New York State's tax laws. Once confirmed, the seller should calculate the sales tax due based on the transaction’s value and applicable tax rates. Accurate completion of all sections, such as seller information, sale details, and tax calculation, is essential. After filling out the form, it should be submitted to the New York State Tax Department within the stipulated timeframe, which is typically 20 days from the sale date.

Obtaining the Form ST-131815

The Form ST-131815 can be obtained through multiple channels. It is available for download on the New York State Department of Taxation and Finance website, ensuring easy access for all potential users. Additionally, paper versions might be available upon request from local tax offices. For those who prefer digital options, various tax software platforms may also include this form in their offerings, allowing for easier integration into electronic tax filing systems.

Completing the Form ST-131815

To complete the Form ST-131815 accurately, sellers should follow a structured approach:

- Gather Necessary Information: Collect all relevant details concerning the sale, including the date, description, and selling price of the items involved.

- Calculate Sales Tax: Determine the appropriate sales tax rate and calculate the total tax due based on the sale amount.

- Fill Out Sections: Complete all sections of the form, including seller information, transaction details, and tax calculation.

- Verify Information: Double-check the form for accuracy and completeness to avoid errors that could lead to penalties.

- Submit: Send the completed form along with payment for the tax due to the appropriate state tax office within 20 days of the transaction.

Important Terms Related to Form ST-131815

Understanding the terminology associated with the Form ST-131815 is vital for accurate filing:

- Casual Sale: A non-recurring, occasional sale not typically made in the course of regular business activities.

- Sales Tax: A tax imposed by the state on the sale of goods and services.

- Seller’s Report: A document indicating the amount of sales tax due from a particular sale.

- Vendor: An individual or business entity registered with the state to collect and remit sales tax regularly.

Legal Use of the Form ST-131815

The legal use of Form ST-131815 ensures compliance with New York State's taxation regulations. It serves as a self-reporting tool for casual sellers to fulfill their tax obligations without needing vendor registration. Filing this form accurately prevents legal complications that could arise from unreported sales taxes, thereby safeguarding the seller from fines or penalties associated with non-compliance.

Key Elements of the Form ST-131815

Understanding the critical elements of the Form ST-131815 is essential for precise completion:

- Seller Identification: Includes personal or business information of the seller.

- Transaction Details: Covers specifics about the sale, such as date, item sold, and sale amount.

- Tax Computation: Involves the calculation of sales tax based on prescribed state rates.

- Submission Details: Instructions on filing the form and payment submission to the tax authorities.

Penalties for Non-Compliance

Non-compliance with the requirements of the Form ST-131815 can lead to significant penalties. Failure to file the form within the 20-day period after the sale may result in financial fines, and persistent non-compliance could lead to more severe legal actions. It’s crucial for sellers engaging in casual sales to understand and fulfill their tax obligations to avoid these penalties.

Filing Deadlines and Important Dates

The Form ST-131815 must be filed promptly within the designated timeframe set by the New York State Tax Department. The deadline requires submission within 20 days of the sale. Sellers should mark important dates related to casual sales and tax reporting on their calendar to prevent late submissions and the accompanying penalties.