Definition & Meaning

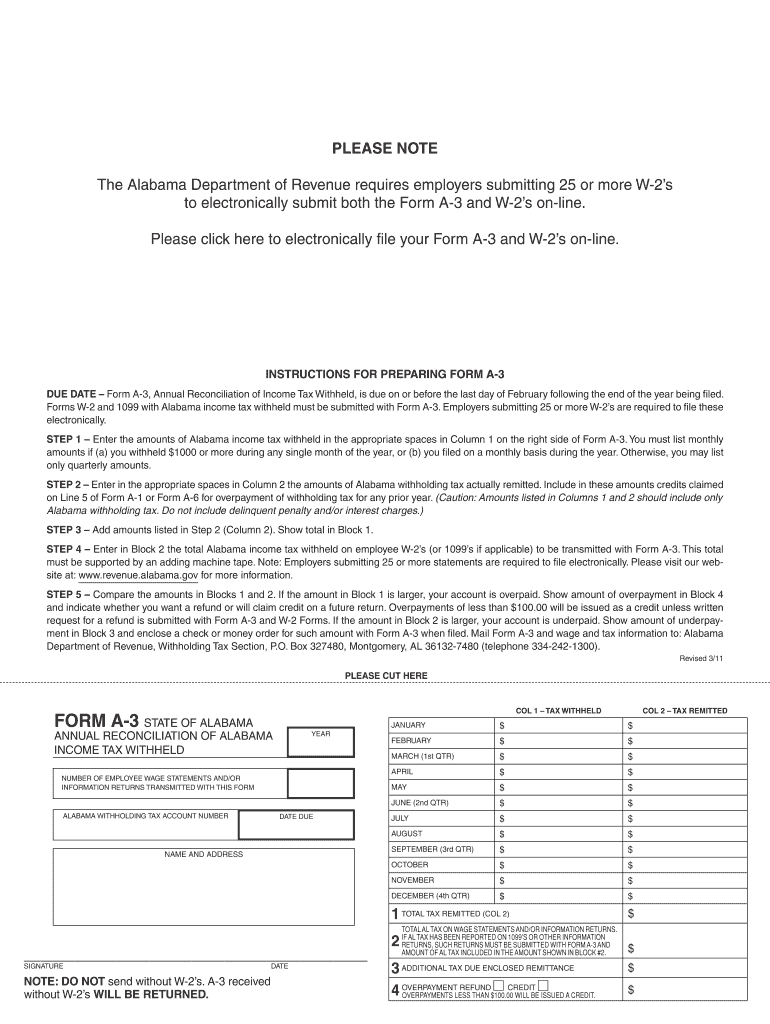

"AL Form 2011" refers to a specific tax form used in Alabama for the annual reconciliation of income taxes withheld from employees. This form is crucial for employers within the state, as it ensures compliance with state taxation laws. Employers who handle payroll must use AL Form 2011 to report the total income tax withheld and remitted during the calendar year. This documentation helps maintain transparency between the employer and the Alabama Department of Revenue, ensuring that the correct amount of tax has been reported and paid.

How to Use the AL Form 2011

Using AL Form 2011 requires employers to gather comprehensive payroll data for the year. This includes information about all employees for whom taxes were withheld. Employers will need to:

- Collect all relevant W-2 forms.

- Verify the accuracy of the information related to income and taxes.

- Enter this information into AL Form 2011 with precision, ensuring that each entry aligns with the records from the payroll system.

When filling out the form, it’s crucial to follow the instructions carefully. Any discrepancies or errors can lead to penalties. Once completed, the form can be submitted electronically or via mail, depending on the employer’s preference and available resources.

Steps to Complete the AL Form 2011

Completing AL Form 2011 involves several steps that ensure accuracy and compliance:

- Prepare Your Financial Records: Gather all necessary payroll records and verify their accuracy.

- Fill Out Employee Information: Use employee W-2 forms to enter data accurately onto AL Form 2011.

- Calculate Total Tax Withheld: Ensure that the total withholding matches the cumulative amounts on all employees’ W-2 forms.

- Reconcile Differences: Check for any overpayments or underpayments of withheld taxes and record these accurately.

- Submit the Form: Depending on your filing method, submit the form electronically or by mail to the Alabama Department of Revenue by the due date.

Key Elements of the AL Form 2011

AL Form 2011 contains several key elements that employers must understand:

- Employer Identification Number (EIN): It’s essential to include the correct EIN to avoid processing errors.

- Reporting Period: Specify the calendar year for which the reconciliation is being made.

- Employee Details: Accurately enter each employee's social security number and address.

- Tax Details: Include the total wages paid and taxes withheld for the year.

- Certification: The form must be signed and dated by an authorized representative of the employer to validate the information provided.

Important Terms Related to AL Form 2011

Understanding specific terms related to AL Form 2011 will aid in accurate completion and submission:

- Withholding Tax: The amount of employee pay withheld by the employer and sent directly to the government as partial payment of income tax.

- Reconciliation: The process of matching the reported income tax withheld with the actual amount paid and reported on employee W-2 forms.

- Overpayment/Underpayment: Situations where the tax withheld either exceeds or fails to meet the amount reported, requiring adjustment and documentation.

Who Typically Uses the AL Form 2011

AL Form 2011 is predominantly used by employers operating within Alabama who employ more than 25 employees. These employers are legally obliged to report and reconcile the income tax withheld from their employees' salaries. The form is applicable to various business types, including corporations, non-profit organizations, partnerships, and sole proprietorships, all of which handle employment and withhold income taxes for the state.

Filing Deadlines / Important Dates

The filing deadline for AL Form 2011 is a critical date that employers must not overlook:

- Due Date: The form is typically due by January 31 of the year following the tax year in question. This timeline aligns with federal W-2 form submissions, ensuring consistent and synchronous reporting.

Adhering to these deadlines is crucial to avoid penalties and ensure compliance with state tax requirements.

Penalties for Non-Compliance

Failure to comply with the requirements related to AL Form 2011 can result in penalties for employers. These penalties may include:

- Late Filing Penalties: If the form is not submitted by the due date, employers may incur financial penalties.

- Errors or Omissions: Inaccurate reporting can attract penalties, particularly if the discrepancies are not corrected promptly.

Employers should ensure thorough verification processes to mitigate the risk of incurring such penalties and maintain compliance with Alabama tax laws.