Definition and Meaning of the CLGS 32-5 2012 Form

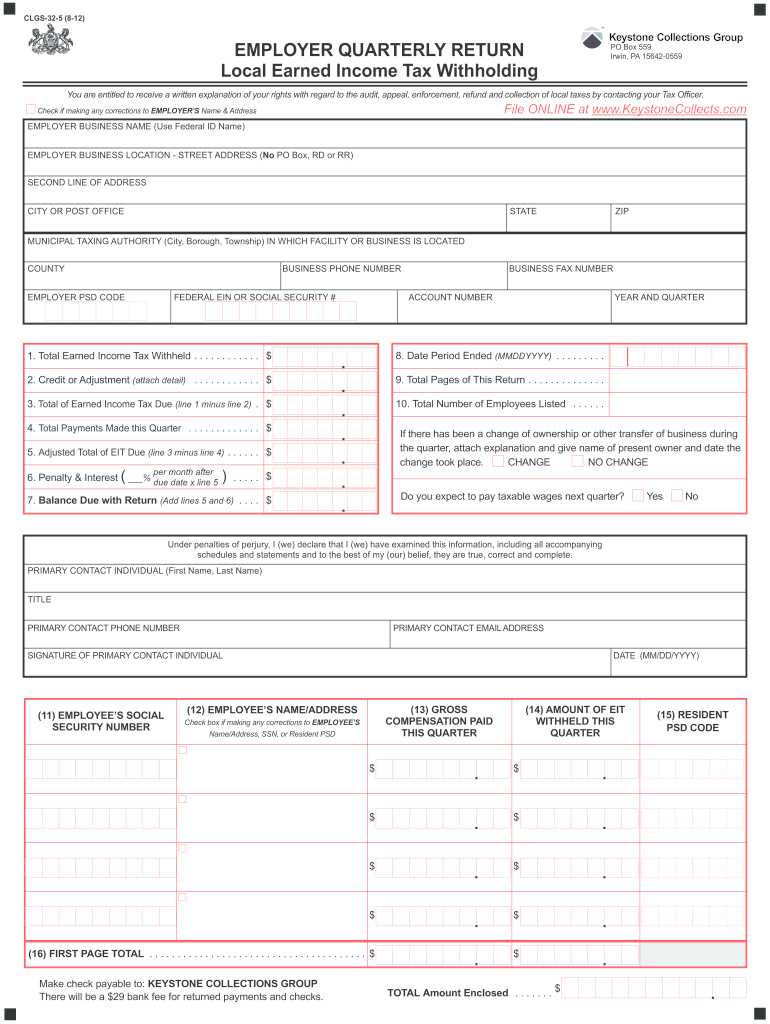

The CLGS 32-5 2012 form is an Employer Quarterly Return document used for reporting and reconciling local earned income tax withheld by employers in certain jurisdictions, particularly in Pennsylvania. Issued by the Keystone Collections Group, this form requires employers to provide details about the total earned income tax withheld from employees, any adjustments or credits, and the total payments made during a specific quarter. Accurate reporting on this form ensures compliance with local tax obligations and facilitates efficient processing by tax authorities.

Key Elements of the CLGS 32-5 2012 Form

- Employer Information: This section captures the employer's demographic and identification details, including the business name and address.

- Employee Earnings: Employers report the total compensation paid to employees for the quarter, providing a basis for tax withholding calculations.

- Withholding Details: This area involves specifying the total local earned income tax withheld from employee wages during the quarter.

- Adjustments or Credits: Employers need to declare any prior period adjustments or credits that may affect the tax amount due.

- Payments Made: Employers document all payments made towards the withheld taxes to date, aiding reconciliation.

How to Use the CLGS 32-5 2012 Form

When utilizing the CLGS 32-5 2012 form, employers must compile and verify their records of employee earnings and tax withholdings for the quarter. They should then accurately input this data into the relevant sections. Employers should double-check for errors or discrepancies that may require amendments before submission.

- Maintain Comprehensive Payroll Records: Ensure all payroll systems record complete and precise data on employee earnings and tax withholdings.

- Verify Tax Withholding Rates: Confirm the local tax rate applicable to your jurisdiction to ensure correct calculation of the withheld amounts.

- Reconcile with Payments: Compare reported withholding with tax payments already made to identify any discrepancies.

Examples

- Example Scenario: A small business in Pennsylvania calculates total wages paid during Q1 as $500,000. At a local tax withholding rate of 1%, the business withholds $5,000. They report this on the CLGS 32-5 2012 form alongside any payments already made.

Steps to Complete the CLGS 32-5 2012 Form

Completing the CLGS 32-5 2012 involves a systematic approach to ensure accuracy and compliance.

- Gather Necessary Documents: Compile payroll records, tax rate schedules, and previous returns for reference.

- Fill in Employer Details: Complete the sections detailing employer name, address, and contact information.

- Report Earnings and Withholdings: Precisely enter the total wages paid and applicable withholdings for the quarter.

- Include Adjustments: Document any adjustments like prior period corrections and credits.

- Review and Reconcile: Cross-verify the reported figures against your financial records and rectify any inaccuracies.

- Submit the Form: Follow submission guidelines specific to your jurisdiction, which may include online, mail, or in-person delivery.

Subsection: Filing Options

- Online Submission: Many jurisdictions offer electronic filing through specialized portals, streamlining submission and speeding up processing times.

- Mail Submission: Traditional filing via mail remains an option, requiring proper postage and timely delivery.

Who Typically Uses the CLGS 32-5 2012 Form

Frequently used by employers in Pennsylvania, the CLGS 32-5 2012 form is essential for businesses that employ individuals liable for local earned income tax. This includes:

- Small-to-Medium Enterprises (SMEs): Typically those with multiple employees under payroll liable for local tax deductions.

- Corporations and Partnerships: Engaging in business activities within specified local jurisdictions.

- Sole Proprietors with Employees: Especially those based where local tax withholding is mandatory.

Legal Use of the CLGS 32-5 2012 Form

The CLGS 32-5 2012 must be used in compliance with state and local tax laws. Employers are responsible for ensuring the accuracy and timeliness of their filings to avoid legal penalties or issues. Any discrepancies or inaccuracies may need to be addressed through amendments or penalty payments.

Penalties for Non-Compliance

- Fines: Financial penalties can be imposed for late submissions or inaccurate reports.

- Legal Repercussions: Continued non-compliance may lead to legal action or additional audits from tax authorities.

Important Terms Related to the CLGS 32-5 2012 Form

Understanding key terms helps in successfully completing and submitting the form.

- Withholding: The portion of income deducted by employers to remit to tax authorities as prepayment of tax liabilities.

- Quarterly Return: A periodic tax report reflecting employer tax activities over a three-month period.

- Reconciliation: Ensuring that all tax deductions match the reports submitted to tax authorities, preventing discrepancies.

IRS Guidelines and Recommendations

While the CLGS 32-5 2012 is a local form, it coordinates with federal tax principles. Employers must comply with relevant IRS guidelines to ensure accuracy and consistency across different forms and reports. For instance:

- Maintain Detailed Records: Both the IRS and state tax authorities require comprehensive documentation to support reported figures.

- Review IRS Circulars: While directly local-focused, keeping abreast of broader IRS guidelines ensures systemic compliance.

Filing Deadlines and Important Dates

Adhering to filing deadlines for the CLGS 32-5 2012 form is necessary to avoid penalties.

- Quarterly Deadlines: Submissions typically due shortly after the end of each calendar quarter.

- Extension Options: Some jurisdictions may allow for extensions upon request under certain circumstances.

State-Specific Rules for the CLGS 32-5 2012 Form

Primarily used in Pennsylvania, the form is subject to state-specific regulations governing local tax collection and employer responsibilities. Understanding these nuances ensures complete and accurate reporting.

Examples

- Pennsylvania: Different municipalities may have varying tax rates and submission requirements, necessitating tailored compliance strategies.

Methods for Obtaining the CLGS 32-5 2012 Form

Employers can usually acquire the form through various channels to ensure compliance.

- Direct Download: Available from tax authority websites or specific municipal portals.

- Tax Software: Some accounting software may include templates for the CLGS 32-5 2012 as part of their tax management offerings.

Form Submission Methods (Online / Mail / In-Person)

Submitting the CLGS 32-5 2012 involves several options which vary by jurisdiction.

- Online: Expedites the process and offers a digital trail for convenience and record-keeping.

- Mail: Requires physical delivery; ensure adequate postage and timely dispatch.

- In-Person: Direct filing at local tax offices may be required or preferred in some cases.

In utilizing the CLGS 32-5 2012 form effectively, maintaining adherence to all procedural requirements is essential for accurate and timely reporting of local earned income taxes.