Definition & Meaning

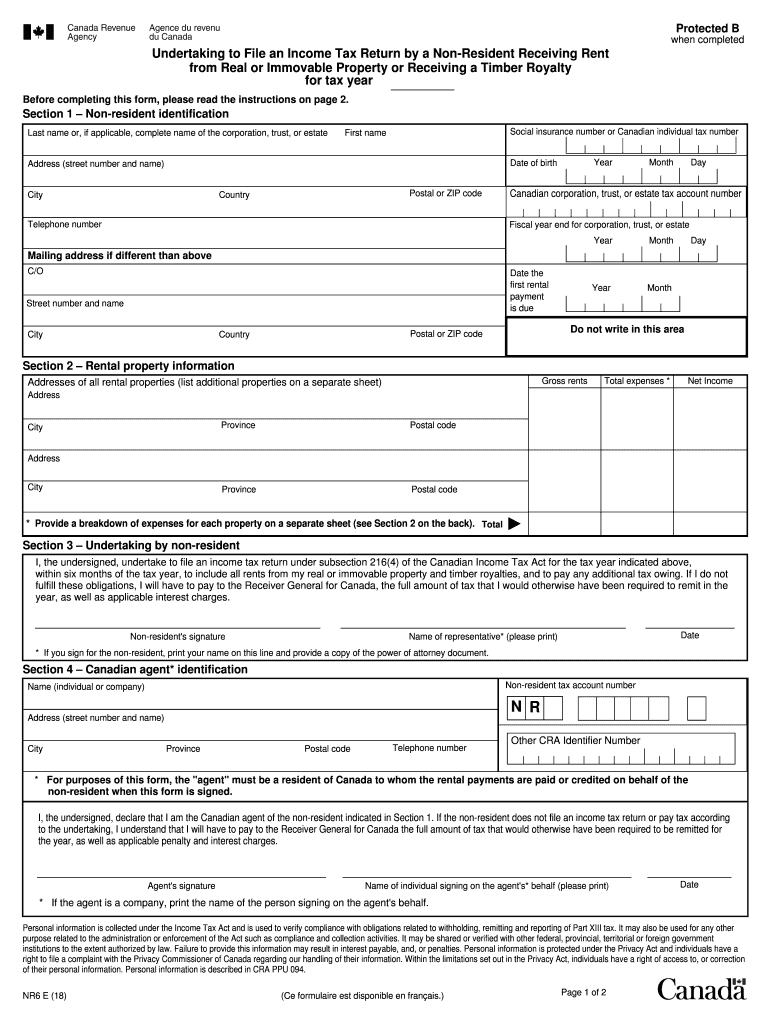

The NR6 form is a tax document used by non-residents in Canada who receive rental income from Canadian real estate or timber royalties. It allows these individuals to file an income tax return under subsection 216(4) of the Canadian Income Tax Act, enabling them to pay tax on net rental income rather than gross rental income. This form plays a critical role in assessing tax obligations for non-resident individuals or entities earning income within Canada. The NR6 form must be completed accurately to ensure compliance with tax laws and to avoid potential penalties.

How to Use the NR6 Form

The NR6 form is utilized to declare that a non-resident plans to pay tax on net rental income. It must be submitted before the tax year or before the first payment of rental income is due. Completing this form involves detailing anticipated rental income and associated expenses to determine the net income. Once completed, it is sent to the Canada Revenue Agency (CRA) for approval. Approval allows the payer to withhold tax on a net basis. Without filing the NR6 form, non-residents must remit 25% of the gross rental income.

Step-by-Step Instructions

- Obtain the NR6 form from the CRA website.

- Fill in personal information, including non-resident identification and rental property details.

- Estimate rental income and associated expenses for the tax year.

- Complete sections related to Canadian agents if applicable.

- Submit the form to the CRA for approval before the first rental payment of the year is due.

How to Obtain the NR6 Form

The NR6 form can be acquired directly from the Canada Revenue Agency’s website. This ensures you are using the most current version of the form. You can either complete it online and print it out or download it in PDF format to fill out manually. Alternatively, you can contact the CRA to receive a paper copy by mail. Many tax software packages also include the NR6 form, which can be filled out and submitted electronically.

Steps to Complete the NR6 Form

The NR6 form involves several steps to ensure proper completion.

- Identify Non-Resident Status: Confirm your non-resident status for Canadian tax purposes.

- Provide Personal Details: Include your name, address, and Canadian tax identification number.

- Detail Rental Property: Describe the Canadian location from which rental or royalty income is derived.

- Estimate Income and Expenses: Include anticipated rental income and allowable expenses.

- Assign Canadian Agent Responsibilities: If applicable, detail the Canadian agent managing tax remittance.

- Declaration: Sign and date the form to declare accuracy.

- Submit the Form: Send the completed form to the CRA for approval.

Important Terms Related to NR6 Form

- Non-Resident: An individual or entity not tax-resident in Canada but earning Canadian income.

- Gross Income: The total income received from rental properties or royalties before deductions.

- Net Income: The income remaining after allowable expenses are deducted from gross income.

- Canadian Agent: A representative managing tax payments on behalf of the non-resident.

- Subsection 216(4): A specific Canadian tax code provision allowing net rental income taxation for non-residents.

Key Elements of the NR6 Form

The NR6 form comprises several critical components that ensure compliance with tax legislation.

- Non-Resident Identification: Includes details such as legal name and tax residency status.

- Rental Property Information: The address and specifics of the property in Canada generating income.

- Income Estimate: Anticipated rental or royalty income and detailed expense projections.

- Agent Designation: Information about any Canadian agent responsible for tax matters.

- Declaration and Signature: A formal declaration of truthfulness and signature of the non-resident.

Filing Deadlines / Important Dates

The NR6 form should be submitted to the CRA before January 1 of the tax year or before the first rental payment of that year is due. It's crucial to adhere to this timeline to ensure approval for tax withholding on a net basis. Missing the deadline can result in the obligation to remit 25% of gross rental income, rather than net. It is advisable to allow sufficient time for processing the form with the CRA.

Penalties for Non-Compliance

Failing to properly file the NR6 form or submitting it after the deadline can lead to significant financial consequences. The primary penalty entails remitting 25% of gross rental income instead of being taxed on a potentially lower net income. Moreover, interest and additional fines might be imposed for late submission. To mitigate such risks, non-residents should ensure complete, accurate, and timely submission of the NR6 form to the CRA.