Definition and Purpose of the 2008 Kansas Retailers' Sales Tax Form

The 2008 Kansas Retailers' Sales Tax Form, known officially as Form ST-36, is a vital document for retailers doing business in Kansas. It is used to report and remit sales tax collected from customers to the state revenue agency. This form ensures compliance with state tax regulations and is mandated for all businesses that engage in taxable retail sales within Kansas. By using this form, retailers contribute to state funding, which supports public services such as education, transportation, and public safety.

How to Obtain the 2008 Kansas Retailers' Sales Tax Form

Obtaining the 2008 Kansas Retailers' Sales Tax Form is straightforward. Businesses can access and download it directly from the Kansas Department of Revenue's official website. The form is available in both PDF format for download and printing, as well as an online version for electronic submission. For those who prefer a physical copy, it can also be requested by contacting the Kansas Department of Revenue through mail or by visiting their local offices.

Steps to Complete the 2008 Kansas Retailers' Sales Tax Form

-

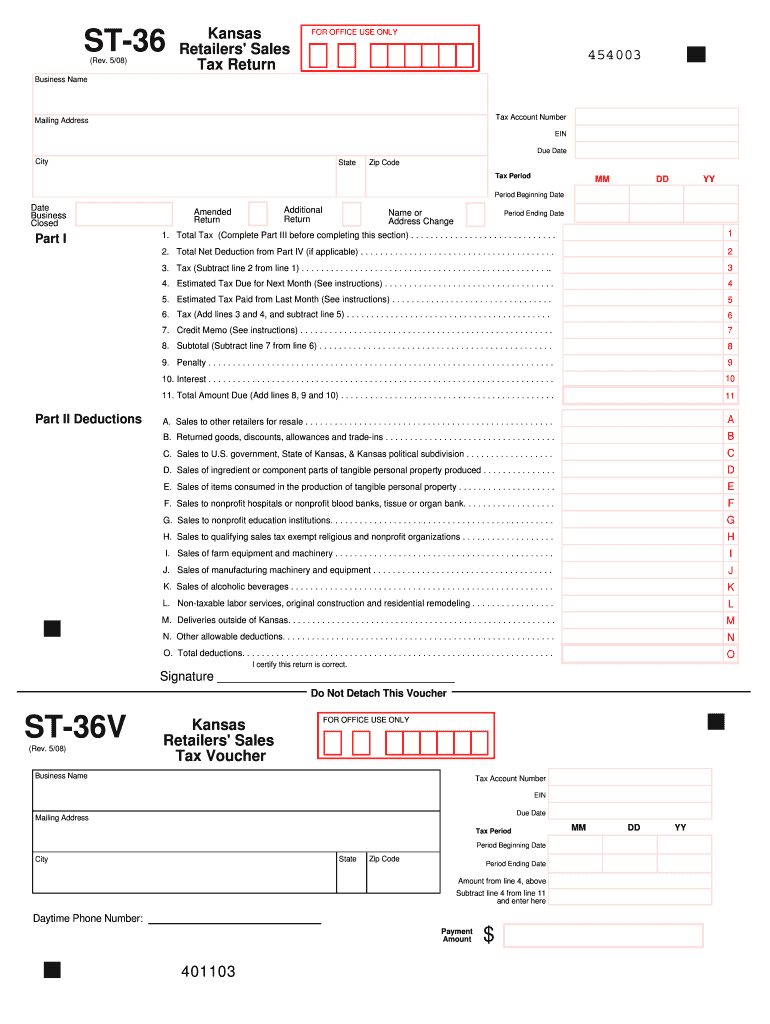

Personal and Business Information Entry: Start by entering your business name, address, and Kansas state tax ID number. Ensure all information is accurate to avoid processing delays.

-

Gross Sales Calculation: Report your total gross sales for the filing period, including all sales transactions before any deductions or exemptions.

-

Deductions and Exemptions: Deduct any sales that qualify for exemptions such as sales to tax-exempt organizations or out-of-state sales.

-

Net Taxable Sales Calculation: Subtract total deductions from the gross sales to determine the net taxable amount.

-

Tax Rate Application: Apply the appropriate sales tax rate based on your business location to calculate the total sales tax due.

-

Payment and Submission: Complete the payment section if submitting by mail, or attach your payment if filing electronically. Submit the completed form by the required deadline to ensure compliance.

Why Should You File the 2008 Kansas Retailers' Sales Tax Form

Filing the 2008 Kansas Retailers' Sales Tax Form is crucial for compliance with state tax laws. Failure to do so can result in penalties, fines, and potential audits. Timely and accurate filing also demonstrates the business's commitment to lawful operations and supports state funding. Additionally, maintaining a correct filing history aids in avoiding complications during business transactions and auditing processes.

Who Typically Uses the 2008 Kansas Retailers' Sales Tax Form

Typically, the form is used by a wide range of business entities, including sole proprietorships, partnerships, corporations, and limited liability companies (LLCs) operating in Kansas. Businesses involved in the sale of goods, whether physical or digital, within the state are required to utilize this form to report and remit sales tax collected from consumers. This includes both brick-and-mortar stores and online retailers whose customer base is located in Kansas.

Key Elements of the 2008 Kansas Retailers' Sales Tax Form

- Business Identification Information: Sections for inputting business name, address, and Kansas sales tax ID.

- Gross and Net Sales Lines: Fields for total gross sales and deductions leading to net taxable sales.

- Tax Rate Specification: Specific area to declare applicable sales tax rate based on business location.

- Signature and Date Section: Required for validation of form submission.

- Payment Information: Area to fill in details for tax payment if amounts are due.

State-Specific Rules for the 2008 Kansas Retailers' Sales Tax Form

Kansas has specific rules governing sales tax filing. It requires all retailers to file even if no taxable sales have occurred during the period. Retailers availing exemptions must maintain detailed records to substantiate claims in case of audits. Geographical location dictates the tax rate applied, which can vary within localities due to additional city or county taxes. Calculating and applying the correct tax rate is essential for compliance.

Filing Deadlines and Important Dates

All retailers must adhere to a strict filing schedule to avoid incurring penalties. The filing frequency—whether monthly, quarterly, or annually—depends on the volume of sales generated by the business:

- Annual Filers: Due by January 25 of the following year.

- Quarterly Filers: Due by the 25th of the month following the end of the quarter.

- Monthly Filers: Due by the 25th of the following month.

Adhering to these deadlines is critical for maintaining compliance and avoiding late fees.

Penalties for Non-Compliance

Failure to file the 2008 Kansas Retailers' Sales Tax Form on time can result in penalties and interest charges. The standard penalty is 1% of the unpaid tax amount for each month the return is late, with a maximum penalty of 24%. Additionally, interest is charged on unpaid tax at a rate determined by state statutes. Businesses with repeated infractions may also face audits or revocation of their sales tax permit, significantly impacting operations.

Examples of Using the 2008 Kansas Retailers' Sales Tax Form

Consider a retailer in Kansas City selling a mix of taxable and exempt goods. They need to report both the gross sales and deduct sales made to exempt entities, like schools, on the ST-36 Form. This process ensures only the correctly taxed amount is reported and paid. Similarly, an online retailer shipping goods to Kansas residents must account for local tax rates applicable to each delivery point when filling out the form, ensuring compliance with geographical tax exemptions and liabilities.