Definition and Meaning

Section 205 30 - Michigan Legislature - State of Michigan relates to a specific legislative provision within Michigan's legal framework. Although the precise text of the section is not provided here, such statutory sections typically cover a range of legal and regulatory obligations applicable to individuals or entities operating within the state. The interpretation of this section is critical for understanding responsibilities related to tax obligations, compliance measures, or other legal duties that are mandated by the state legislation.

- Typically includes guidelines on taxation, taxpayer responsibilities, or government regulatory measures.

- Interpretation of such a section often requires a review by legal professionals to ensure compliance.

- Understanding this section can help businesses and individuals avoid legal penalties and ensure adherence to Michigan laws.

How to Use the Section

Using Section 205 30 effectively involves understanding its implications and applying them to relevant scenarios, such as tax filings or legal compliance. Here are foundational steps in utilizing this section:

- Review the Legislative Text: Access the complete text of Section 205 30 to comprehend the scope of its regulations.

- Identify Applicable Entities: Determine whether this section applies to individuals, businesses, or specific industries.

- Integrate into Compliance Strategy: Align business processes and reporting practices with the mandates of this section.

Real-World Applications

- Businesses should integrate the demands of Section 205 30 within their operational compliance checklists.

- Legal advisors often employ this section to guide clients on Michigan-specific legal requirements.

Steps to Complete the Section

Complying with the requirements of Section 205 30 involves several critical steps:

- Documentation Collection: Gather all necessary financial records and legal documents required under this section.

- Form Completion: Fill out any associated forms or reports as dictated by the legislative guidelines.

- Submit Properly: Ensure that completed forms and documentation are submitted through directed channels, according to state protocols.

Examples

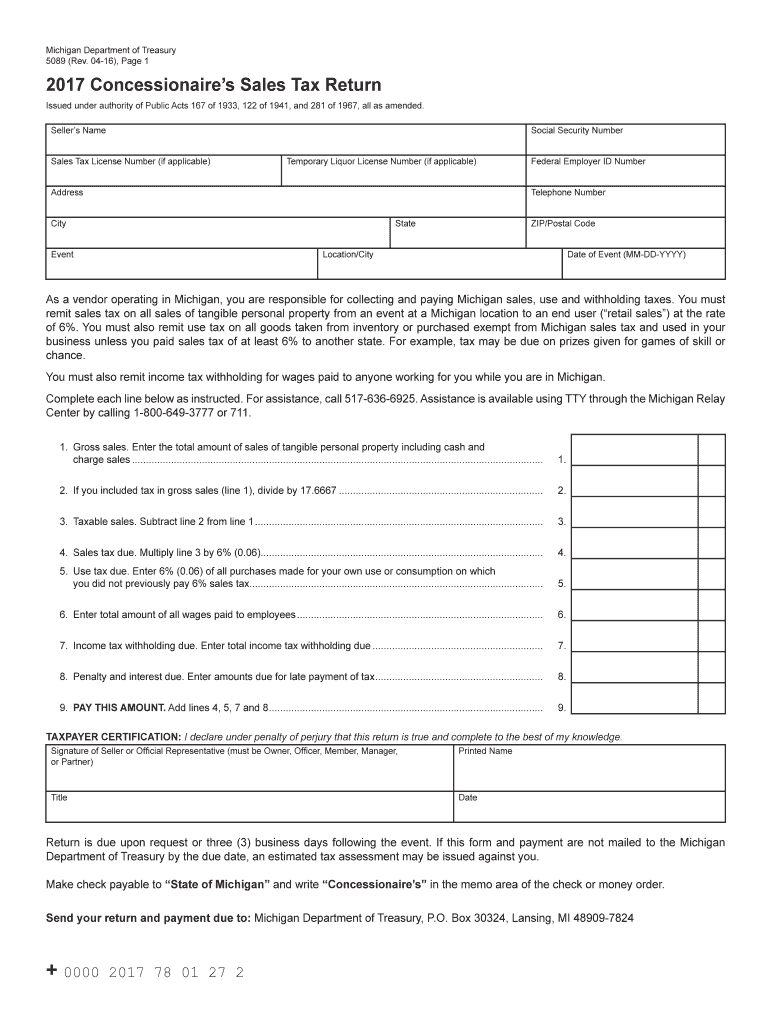

- A Michigan-based business filing its sales tax return would reference Section 205 30 to ensure all taxable sales are correctly reported.

- Individuals using this section may need to complete relevant forms as a part of their annual tax submission process.

Important Terms Related to Section 205 30

Understanding key terms within this section can clarify its application and ensure accurate compliance:

- Taxable Income: Refers to income amounts subject to tax under the guidelines of Section 205 30.

- Gross Receipts: The total revenue considered for taxation before deducting costs or expenses.

- Compliance: Adherence to the financial or legal obligations outlined in Section 205 30.

Further Explanation

- Businesses need to distinguish between taxable and non-taxable income streams, which is crucial when interpreting legal texts such as Section 205 30.

- Accurate understanding of terms avoids misinterpretations that could lead to penalties.

Legal Use of the Section

Legally, Section 205 30 may be used to establish clear rules around taxation, licenses, or operational regulations:

- It informs how taxes should be calculated and remitted to the State of Michigan.

- Legal advisors use it to defend clients' tax positions in disputes with tax authorities.

Practical Insight

- For example, businesses might use this section to cite specific tax deductions or credits available within state law.

- Legal counsel often interprets text within this section to ensure compliance advice aligns with the letter of the law.

State-Specific Rules

Section 205 30 may include regulations unique to Michigan, critical for taxpayers and businesses operating within the state:

- Specific sales tax rates or rules on deductions or credits might differ from federal standards.

- Understanding these nuances helps in establishing precise and compliant tax filing processes.

Example Case

- A company might need to adapt its tax strategies to accommodate Michigan's specific rules concerning sales tax and income reporting as outlined in this section.

Filing Deadlines and Important Dates

Meeting filing deadlines related to Section 205 30 ensures compliance and avoids penalties. Typical filing periods and deadlines include:

- Quarterly Filing: Many tax returns under this section might be due each quarter to reflect sales or income accurately.

- Annual Return Due Date: An annual filing date may also be specified, requiring completed documentation by a particular month each fiscal year.

Compliance Tip

- Keeping a calendar of these dates helps businesses avoid late fees or penalties associated with delayed filing.

Penalties for Non-Compliance

Failure to comply with Section 205 30 can result in penalties, including:

- Financial Fines: Monetary sanctions for late or incorrect submissions.

- Interest Charges: Accrued charges on unpaid tax amounts beyond the prescribed deadlines.

- Legal Penalties: More severe consequences for intentional non-compliance or fraud.

Avoidance Strategies

- Regular consultations with tax professionals can prevent unintentional non-compliance.

- Implementing a robust tax process can help identify and rectify errors before submission deadlines.

Key Takeaways

Familiarity with Section 205 30 is essential for individuals and businesses operating in Michigan to ensure proper tax compliance and avoid the ramifications of overlooking state-specific regulations. Understanding the application, deadlines, and key terms within this section equips users to manage their legal and tax responsibilities effectively, leveraging professional insights when necessary to navigate complexities and fulfill obligations smoothly.