Definition & Meaning

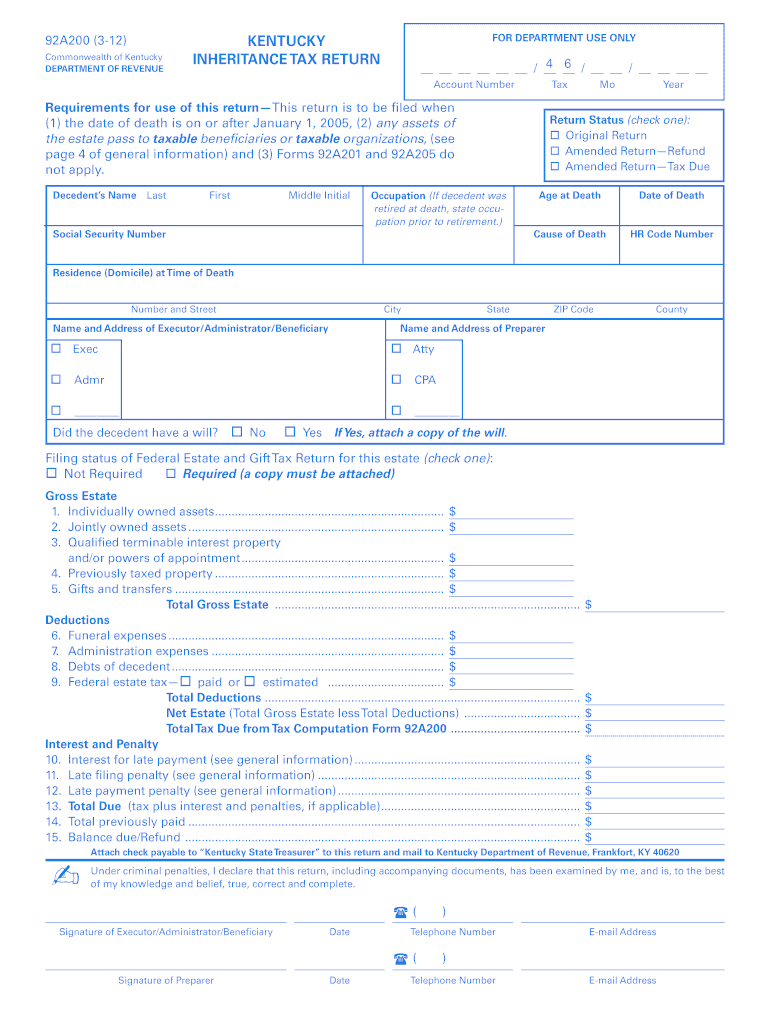

The 92A200 (3-12) - Kentucky: Department of Revenue form is primarily utilized in the process of filing a Kentucky Inheritance Tax Return. This tax form is mandatory for estates where a decedent's assets are transferred to beneficiaries who are subject to tax, effective from January 1, 2005. The form captures essential details about the deceased and their estate, ensuring that all individual and joint assets, terminable interest properties, and other relevant items are appropriately reported.

Inheritance Tax Context

- Inheritance Tax Definition: It is a tax assessed on the portion of the estate inherited by beneficiaries after an individual's death, differing across jurisdictions and subject to specific state rules.

- Kentucky Specifics: In Kentucky, this form is a mechanism to establish and report the tax liabilities of estates, complying with state revenue laws.

How to Use the 92A200 Form

Using the 92A200 correctly involves understanding the necessary details and sections required for comprehensive filing.

Detailed Procedure for Completion

-

Gather Information About the Decedent: Collect data such as date of death, social security number, and any documents that detail ownership of assets.

-

Asset Reporting: Identify all assets, categorizing them into individually owned, jointly owned, or gifts and transfers. These have specific sections on the form.

-

Expense and Debt Reporting: Document funeral expenses, administrative costs, and any debts the decedent owes, which can be deducted before tax calculation.

-

Provide Beneficiary Details: Enter information about each beneficiary, including relationship to the deceased and their portion of the estate.

Required Data Points

- Personal Identification: Social security, address, and date of death.

- Asset Valuations: Accurately assess real and personal property values.

Steps to Complete the 92A200 Form

Filing the 92A200 form involves a sequential approach to ensure compliance and accuracy.

Step-by-Step Instructions

- Identification Section: Fill out the decedent’s personal and estate identification details.

- Asset and Property Schedules: Complete schedules for each category of assets owned by the decedent.

- Debts and Expense Schedules: Detail any outstanding debts and allowable administration expenses.

- Beneficiary Details: For each beneficiary, indicate their share and relationship to the decedent.

- Tax Computation: Use the provided schedules to calculate the total and taxable estate, leading to the tax owed.

- Review and Sign: Thoroughly review for accuracy before signing.

Required Documents

Ensuring you have all necessary documentation beforehand simplifies filling out the 92A200.

Essential Document List

- Death Certificate: Official document confirming the passing of the decedent.

- Asset Valuation Records: Professional appraisals or market statements for real estate, stocks, and other investments.

- Debt and Expense Proofs: Receipts or statements of debts and funeral costs.

- Beneficiary Statements: Any legal documents supporting the allocation of estate shares to heirs.

Filing Deadlines / Important Dates

Adhering to specific deadlines is critical when filing the 92A200 form to avoid penalties.

Key Submission Deadlines

- Standard Filing Period: Typically within nine months of the decedent's date of death. Extensions may be requested under certain conditions.

- Penalty Avoidance: Filing before the deadline without errors helps avoid interest and penalty assessments.

Penalties for Non-Compliance

Failing to properly file the 92A200 form can result in significant penalties.

Consequences of Late or Inaccurate Filing

- Monetary Penalties: Interest charges and financial penalties for overdue taxes.

- Legal Repercussions: Possible legal action for significant discrepancies or fraudulent reporting.

Digital vs. Paper Version

The choice between digital and paper versions can impact filing efficiency and accuracy.

Comparison of Filing Methods

- Digital Filing: Allows for automatic calculations and error-checking features, reducing manual mistakes.

- Paper Filing: Suitable for those more comfortable with hard copy submissions but may require more manual checks.

State-Specific Rules

Different states have varying requirements, and understanding Kentucky-specific regulations is crucial.

Kentucky Inheritance Tax Rules

- Exemptions and Deductions: Specific exemptions apply, and some deductions may only be claimed based on Kentucky law.

- Filing Requirements: Kentucky mandates tax filing for taxable estates exceeding a certain asset threshold, requiring detailed reporting as per state provisions.

These comprehensive details ensure clarity and precise filing of the 92A200 form, accommodating the nuanced requirements of estates within Kentucky under the Department of Revenue guidelines.