Type text, add images, blackout confidential details, add comments, highlights and more.

02. Sign it in a few clicks

Draw your signature, type it, upload its image, or use your mobile device as a signature pad.

03. Share your form with others

Send it via email, link, or fax. You can also download it, export it or print it out.

How to use or fill out form ct 588 2011 with our platform

Ease of Setup

DocHub User Ratings on G2

Ease of Use

DocHub User Ratings on G2

Click ‘Get Form’ to open it in the editor.

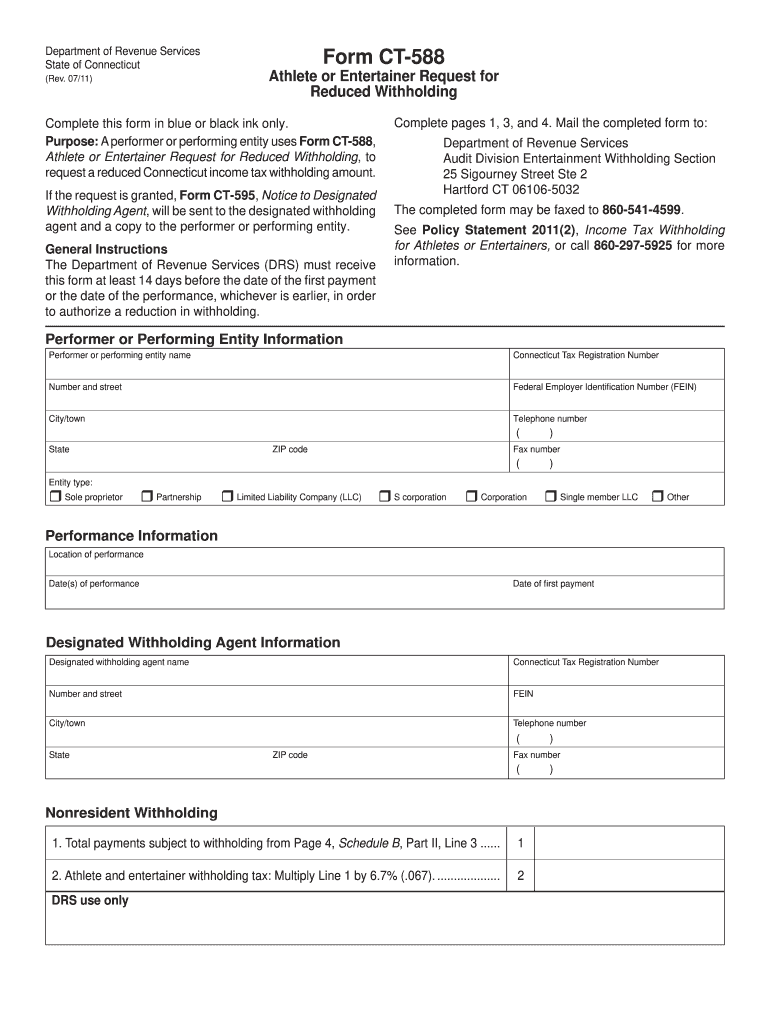

Begin by filling out the 'Performer or Performing Entity Information' section. Enter your name, Connecticut Tax Registration Number, address, and contact details accurately.

Next, provide the 'Performance Information.' Include the location and date(s) of your performance along with the date of the first payment.

In the 'Designated Withholding Agent Information' section, input the agent's name and tax registration number. Ensure all details are correct to avoid processing delays.

Proceed to complete Schedule A by listing all income received for Connecticut performances. Be thorough in detailing each item and its corresponding amount.

Fill out Schedule B with compensation details for each participant. Attach additional sheets if necessary and ensure totals align with previous sections.

Finally, review all entries for accuracy before submitting. You can easily save and share your completed form directly from our platform.

Start using our platform today to streamline your form completion process for free!

FTB Form 588, Nonresident Withholding Waiver Request Nonresident payee who qualifies can use Form 588 to get a waiver from withholding based generally on California tax filing history. Form 588 must be submitted at least 21 business days before payment is made.

What is Form 588?

Use Form 588, Nonresident Withholding Waiver Request, to request a waiver from withholding on payments of California source income to nonresident payees. Do not use Form 588 to request a waiver if you are a foreign (non-U.S.) partner or member.

What is the withholding tax in CT for athletes and entertainers?

3410.3 Exceptions to the Connecticut Athlete and Entertainer Withholding Tax. The State of Connecticut has provided several exceptions to the 6.99% withholding requirement outlined in Section 3410.2, above.

How to claim California nonwage withholding credit?

Claim your nonwage withholding credit on one of the following: Form 540, California Resident Income Tax Return. Form 540NR, California Nonresident or Part-Year Resident Income Tax Return. Form 541, California Fiduciary Income Tax Return.

What is the CT estate tax return form?

A Connecticut estate tax return must be filed after your death, regardless of the size of your estate. It will be your executors responsibility to file either Form CT-706 (for taxable estates) or CT-706 NT (for nontaxable estates). Both the return and any tax owed are due six months after the death.

Related Searches

Form ct 588 2011 instructionsHow to fill out form ct 588 2011

Security and compliance

At DocHub, your data security is our priority. We follow HIPAA, SOC2, GDPR, and other standards, so you can work on your documents with confidence.

Form 588 must be submitted at least 21 business days before payment is made. Withholding agent keeps a copy of the waiver certificate in records. No withholding required with a waiver certificate.

Who needs to fill out a California form 590 withholding?

If you have a permanent place of business in California or you are qualified to do business through the California Secretary of State, then complete: Franchise Tax Board Form 590 Withholding Exemption Certificate.

Related links

CT-588, Athlete or Entertainer Request for Reduced

Purpose: A performer or performing entity uses Form CT-588,. Athlete or Entertainer Request for Reduced Withholding, to request a reduced Connecticut income taxRead more

PS 2011(2), Income Tax Withholding for Athletes or

To request reduced Connecticut income tax withholding, mail Form CT-588 to Department of. Revenue Services, Audit Division, Entertainment. Withholding Section,Read more

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.