Type text, add images, blackout confidential details, add comments, highlights and more.

02. Sign it in a few clicks

Draw your signature, type it, upload its image, or use your mobile device as a signature pad.

03. Share your form with others

Send it via email, link, or fax. You can also download it, export it or print it out.

How to use or fill out form 92a200 2003 with our platform

Ease of Setup

DocHub User Ratings on G2

Ease of Use

DocHub User Ratings on G2

Click ‘Get Form’ to open it in the editor.

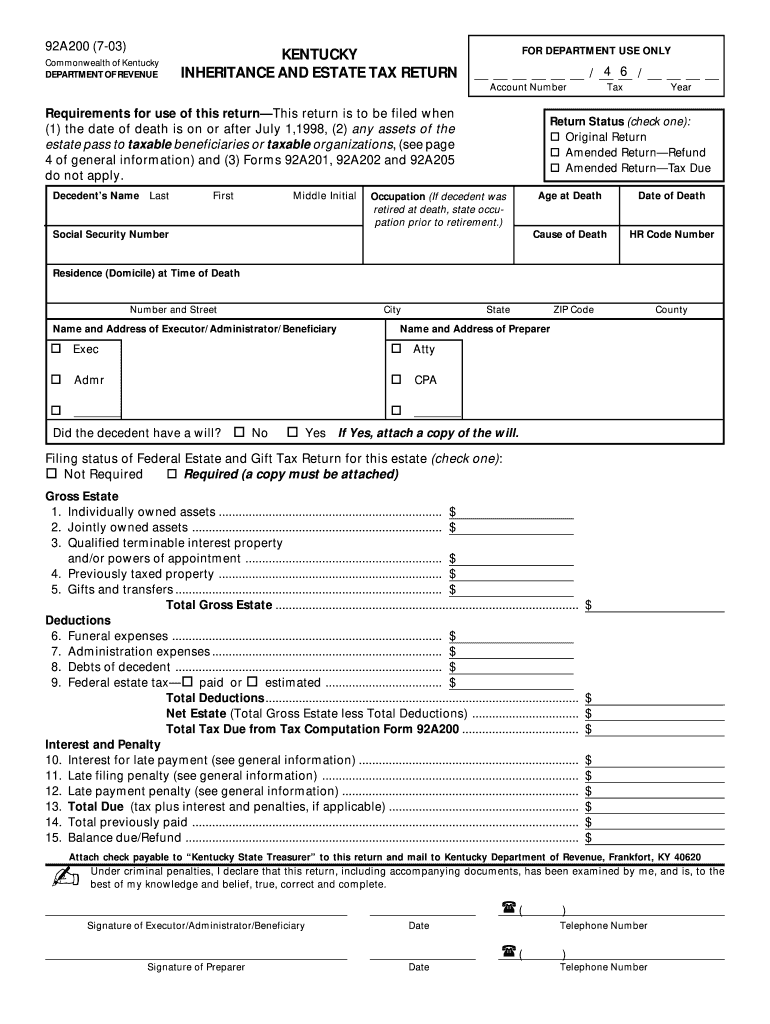

Begin by entering the decedent’s name, tax year, and account number at the top of the form. Ensure all details are accurate.

In the 'Return Status' section, select whether this is an original return or an amended return. Fill in the age at death and social security number.

Complete the sections for gross estate by listing individually owned assets, jointly owned assets, and any qualified terminable interest property. Be thorough in your descriptions and values.

Fill out deductions including funeral expenses, administration expenses, and debts of the decedent. Make sure to attach any necessary documentation as specified.

Finally, review all entries for accuracy before signing as executor or administrator. Submit your completed form through our platform for a seamless filing experience.

Start filling out your form 92a200 2003 today for free using our platform!

Form 92a200 2003 pdfForm 92a200 2003 onlineForm 92a200 2003 instructionsKentucky Inheritance tax return Short FormKentucky inheritance tax chart pdfKentucky inheritance laws with a will pdfAffidavit of EXEMPTION KentuckyExecutor of estate Form Kentucky

Security and compliance

At DocHub, your data security is our priority. We follow HIPAA, SOC2, GDPR, and other standards, so you can work on your documents with confidence.

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.