Definition and Meaning of Form 8

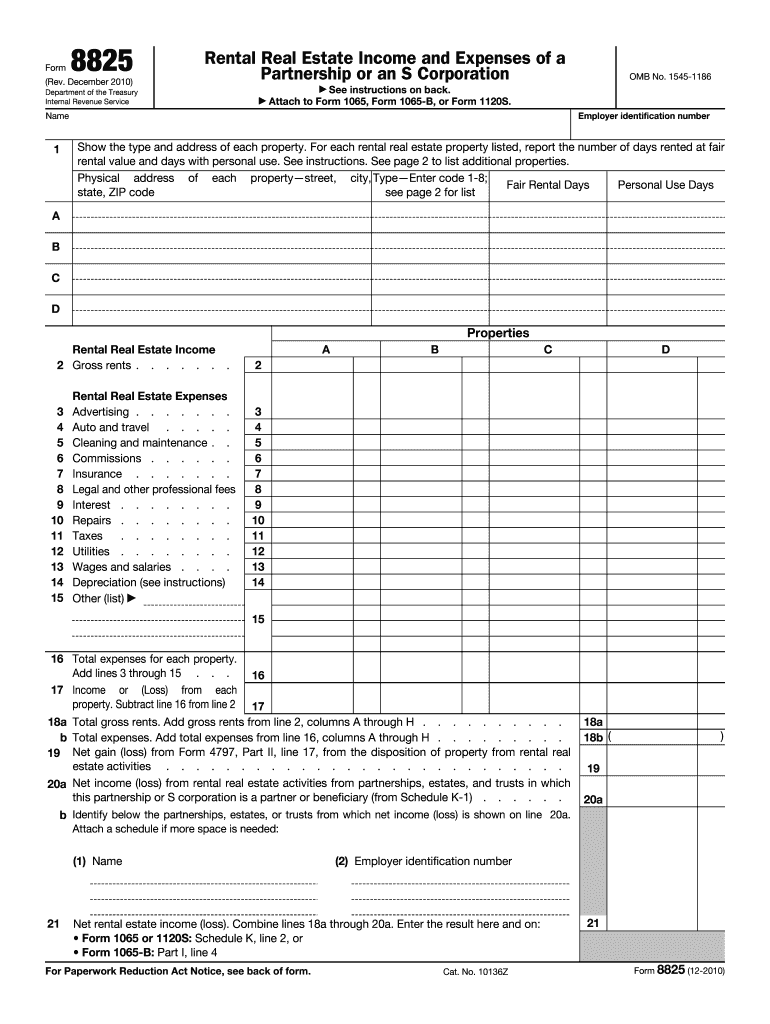

Form 8825 is a necessary tax document used by partnerships and S corporations to report income and expenses related to rental real estate activities. Emphasizing rental real estate, the form provides a structured approach to calculate net income or loss from these activities for tax reporting purposes. Each submitted form includes specifics about each rental property, such as its address, type, days rented at fair rental value, and days of personal use. Recognizing the significance of detailed reporting, the form breaks down rental income and expenses into various categories, aiding precision in final calculations.

How to Use Form 8

For those required to file Form 8825, its primary use is to accurately document and report all rental real estate income and expenses associated with partnerships or S corporations. Successful navigation of this form involves:

-

Collecting Information:

- Gather complete data regarding each property, including income generated and expenses incurred.

-

Organizing Details:

- Differentiate between expenses borne by the corporation and those covered by tenants, as they count towards your financial reporting.

-

Precise Entry:

- Ensure that the form is filled correctly by systematically aligning numbers from each property to their corresponding lines on the form. This involves precise detailing of rental days and fair value calculations.

Steps to Complete Form 8

Filling in Form 8825 effectively requires a step-by-step approach to avoid any errors or oversight:

-

Identifying Properties:

- Start by listing all properties related to the partnership or S corporation.

-

Recording Income:

- For each property, accurately document all rental income received.

-

Cataloguing Expenses:

- Note all expenses paid for the upkeep and management of these properties. Key expenses may include property taxes, repairs, utilities, and interest payments.

-

Calculation of Net Income or Loss:

- Compute the net income or loss by subtracting total expenses from total income, providing a clear financial picture to tax authorities.

-

Completion:

- Review the form meticulously for discrepancies, ensuring all information aligns with supporting documents.

Important Terms Related to Form 8

- Fair Rental Value: The rent an informed lessee would pay to an informed lessor, where both parties are acting in their best interest.

- Passive Activity: Any rental activity or business activity in which a taxpayer does not materially participate.

- Depreciation: A non-cash accommodation on the form, calculating the decrease in value of an asset over time.

IRS Guidelines for Form 8

The IRS provides comprehensive guidelines for completing Form 8825:

- Income Reporting: Rental income should include all amounts paid for the use or occupation of property.

- Expense Deduction: Only necessary and ordinary expenses directly related to the management and maintenance of the property are deductible.

- Documentation: Maintain adequate records to support all income and deductions reported.

Who Typically Uses Form 8

Form 8825 is prominently used by partnerships and S corporations involved in rental real estate pursuits:

- Partnerships: Groups of individuals or entities that operate real estate ventures cooperatively.

- S Corporations: Business entities that elect to pass corporate income, losses, deductions, and credits through to their shareholders for federal tax purposes.

Required Documents for Completing Form 8

To accurately complete Form 8825, ensure access to:

- Income Statements: Demonstrating all rental revenue.

- Expense Receipts and Invoices: Validating all claimed expenses.

- Property Records: Listing current ownership and property details.

- Prior Tax Documents: Useful for comparison and ensuring year-on-year accuracy.

Penalties for Non-Compliance

Adherence to compliance standards is crucial when filing Form 8825. Failing to file or provide adequate information may result in penalties such as:

- Monetary Penalties: Fines for each incorrect or missing form.

- Interest on Underreported Income: The IRS may charge interest on unreported taxable income.

- Audit Risks: Increased likelihood of a detailed IRS audit, which can be both time-consuming and financially detrimental.