Definition & Meaning

The "1099-S" form is a critical document used in the United States to report the proceeds from real estate transactions to the Internal Revenue Service (IRS). The "2015" designation indicates that this form pertains to the tax year 2015. It is essential for sellers who have completed transactions such as sales or exchanges of real estate. The form ensures that the IRS is informed about the proceeds you received, which could affect your taxable income for that year.

Who Typically Uses the 1099-S Form

Generally, the 1099-S form is used by sellers, transferors, and parties involved in the primary role of a transaction transferring ownership of real estate. This often includes individual property owners, businesses, and sometimes legal representatives or real estate agents acting on behalf of others in facilitating these transactions. Being knowledgeable about who should be using these forms helps ensure compliance with tax laws.

How to Obtain the 1099-S 2015 Form

Acquiring the 1099-S 2015 form is a straightforward process. It can be downloaded directly from the IRS website or through authorized tax form distribution services. For businesses or individuals who frequently deal in real estate transactions, it might be beneficial to use tax software that includes built-in capabilities to generate such forms. Additionally, some cloud-based document management platforms can help manage and store these forms securely.

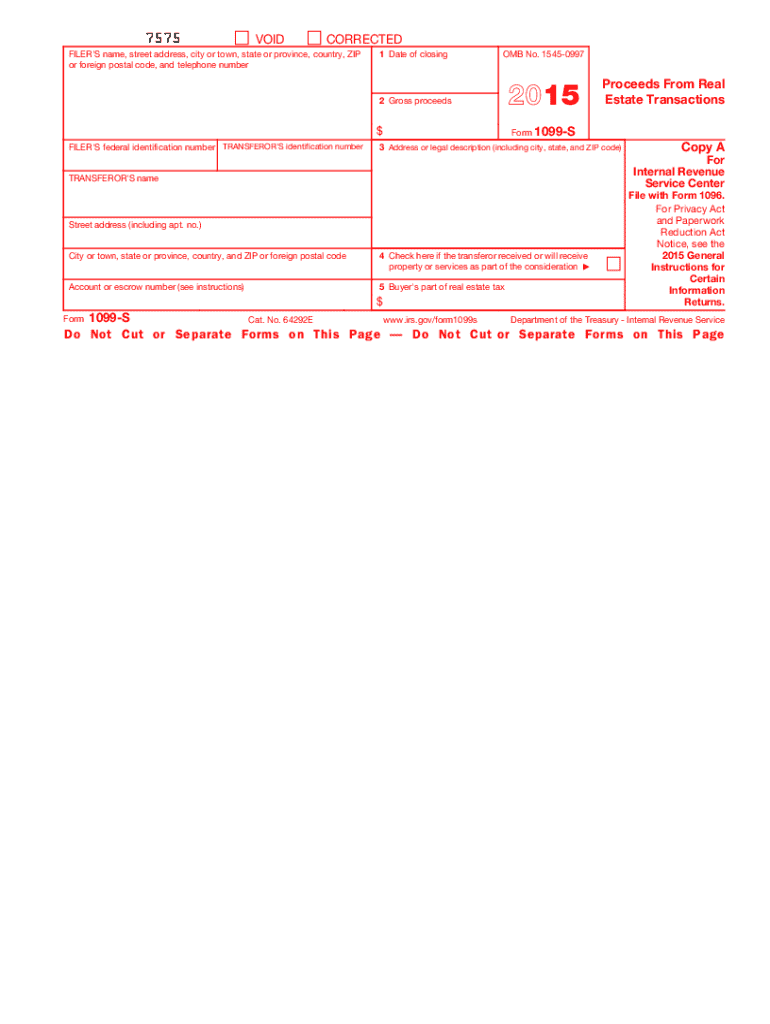

Key Elements of the 1099-S 2015 Form

The 1099-S 2015 form consists of several critical sections that must be completed accurately:

- Transferor’s Information: Includes the full legal name, address, and tax identification number.

- Description of the Property: Details about the property, such as location and specifics about the transaction.

- Gross Proceeds: This indicates the total proceeds from the transaction, exclusive of those transferred to third parties.

- Date of Closing: The official date when the property sale or exchange was completed.

Each element is crucial for ensuring the IRS has comprehensive data about the transaction.

Steps to Complete the 1099-S 2015 Form

- Gather Necessary Information: Identify all the required data points, including personal identification and property details.

- Fill Out Transferor Information: Complete with accurate names, addresses, and tax ID numbers.

- Provide Property Details: Ensure the property description is thorough and precise.

- Report Gross Proceeds: Calculate and fill in the total amount received from the sale or exchange.

- Verify the Closing Date: Make sure the date is correct to match official records.

Checking for inaccuracies or omissions is crucial to prevent processing delays or penalties.

IRS Guidelines

The IRS has specific guidelines for filing Form 1099-S, which are essential for ensuring compliance and avoiding penalties. According to these guidelines:

- Timely Filing: Ensure forms are submitted to both the IRS and the recipient by the respective deadlines to avoid late fees or penalties.

- Accurate Data: The form must be filled with precise numerical values and information to reflect the transaction accurately.

- Identifying Errors: Any discovered errors in submitted forms must be corrected promptly following IRS procedures.

Abiding by these guidelines protects against possible legal repercussions or financial penalties.

Filing Deadlines / Important Dates

Filing deadlines are paramount to maintaining compliance:

- January 31: Provide the completed form to the recipient involved in the real estate transaction by this date.

- February 28: Paper submissions to the IRS must also be completed by this date.

- March 31: For electronic submissions, ensure that the form is filed by this deadline.

Knowing these deadlines is vital for preparing documents and scheduling submissions to avoid unnecessary fines.

Penalties for Non-Compliance

Failing to file the 1099-S form, or filing it with incorrect information, can lead to substantial penalties. The IRS provides penalties depending on how long past the filing date the forms were submitted and whether the errors were corrected promptly:

- $50 per form if filed correctly within 30 days of the due date.

- $100 per form if filed more than 30 days late but before August 1.

- $260 per form for forms filed after August 1 or not at all.

Being aware of these potential penalties highlights the importance of timely and accurate submissions.

Software Compatibility

Software programs such as TurboTax and QuickBooks can assist in both completing and filing the 1099-S form. These tools simplify the input process and provide structured guidance to ensure compliance. For those involved in extensive real estate transactions, using software that offers e-filing capabilities can streamline workflow and reduce the risk of human error.

State-Specific Rules for the 1099-S Form

While the 1099-S form is a federal document, state-specific rules can influence how transactions are reported. Some states might have additional forms or require different filing procedures. It's advisable to consult a tax professional or legal advisor to ensure compliance with both federal and state requirements when filling out and submitting the 1099-S form.

Understanding these nuances allows individuals and businesses to navigate tax responsibilities with greater confidence and agility.