Definition & Meaning

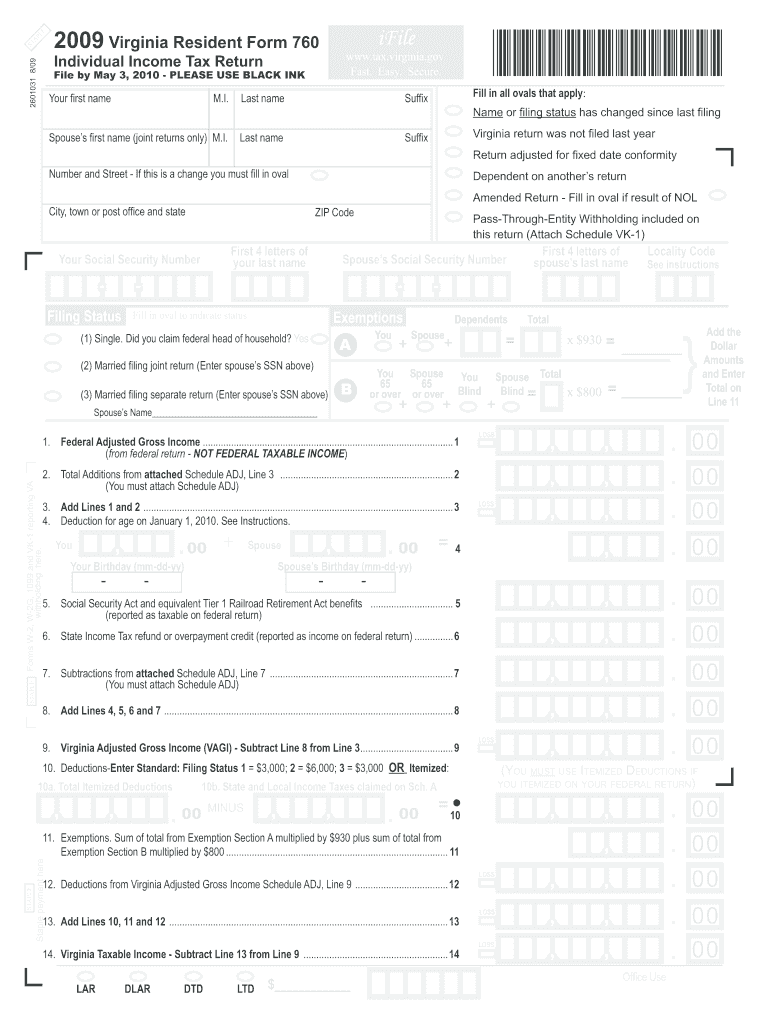

The 2009 Virginia Resident Form 760, commonly known as the 2009 760 form, is a state tax return document used by residents of Virginia to report their income and calculate taxes for the year 2009. Taxpayers must furnish details of their federal adjusted gross income and determine their Virginia taxable income. The form facilitates the declaration of exemptions, deductions, and tax credits applicable for the 2009 tax year.

Steps to Complete the 2009 760 Form

-

Gather Required Information: Collect personal and financial information, including Social Security numbers, W-2s, 1099s, and any documents reflecting income or deductions.

-

Calculate Federal Adjusted Gross Income: Use your federal tax return to fill in your adjusted gross income accurately.

-

Determine Virginia Taxable Income: Subtract any applicable deductions from your federal adjusted gross income to establish your state taxable income.

-

Apply Exemptions and Credits: Identify any exemptions and credits applicable to your situation to lower the taxable amount.

-

Complete the Filing Status and Personal Information Sections: Include your filing status and any dependent information.

-

Finalize and Review the Form: Ensure that all sections are filled correctly, double-check for any errors, and sign the document to validate it.

Who Typically Uses the 2009 760 Form

The form is primarily used by Virginia residents who earned income in 2009 and need to report their earnings to the state taxation authorities. It is vital for individuals or households who live within Virginia and have an obligation to file a state income tax return for that fiscal year.

Filing Deadlines / Important Dates

For the 2009 760 Form, taxpayers were required to submit their completed forms by May 3, 2010. This filing deadline ensured that taxpayers reported their income and fulfilled their tax obligations in a timely manner, avoiding any penalties or interest from late submissions. It's important to note that this deadline aligns with the federal tax return adjustments for that year.

Legal Use of the 2009 760 Form

The 2009 760 Form is legally mandated for taxpayers who need to declare their state income and calculate applicable taxes. Adhering to the regulations of the Virginia Department of Taxation is crucial to avoid any legal ramifications. The form ensures compliance with state tax laws and helps taxpayers take advantage of state-specific deductions and credits.

Key Elements of the 2009 760 Form

- Personal Information: Includes details such as name, address, and Social Security number.

- Filing Status: Helps determine tax calculations based on marital status and household structure.

- Exemptions and Deductions: Areas of the form where applicable reductions to taxable income are noted.

- Income Calculations: Sections dedicated to the breakdown and reporting of income sources.

- Tax Credits: Opportunities to reduce tax liability through various state credits.

State-Specific Rules for the 2009 760 Form

Virginia has specific laws and guidelines that impact how residents complete the 760 Form. Individual adjustments like the Land Preservation Credit, and other Virginia-specific deductions, can significantly affect the tax outcome. It is relevant for taxpayers to be aware of these unique state provisions to optimize their tax filings correctly.

Required Documents

When filing the 2009 760 Form, you need various documents:

- Federal Tax Return: For reference to adjusted gross income.

- Income Statements: W-2s, 1099s, and other documentation of income.

- Deductions: Receipts or records for claimed deductions.

- Tax Credits: Documents supporting eligibility for any credits claimed.

Form Submission Methods (Online / Mail / In-Person)

In 2009, the Virginia Department of Taxation provided multiple submission options. Taxpayers could mail their completed forms directly, opt for electronic filing via approved software, or sometimes submit them in person at designated tax offices. Each method had its own set of instructions to ensure a smooth and accurate filing process.

Penalties for Non-Compliance

Failing to submit the 2009 760 Form by the deadline or providing incorrect information could lead to penalties. These might include:

- Late Filing Penalties: Additional charges based on the tax owed if the form is not filed by the due date.

- Interest on Unpaid Taxes: Accumulated interest on any taxes not paid by the filing deadline.

- Audit Risks: Increased likelihood of state audits for discrepancies or omissions in reporting.