Definition & Meaning

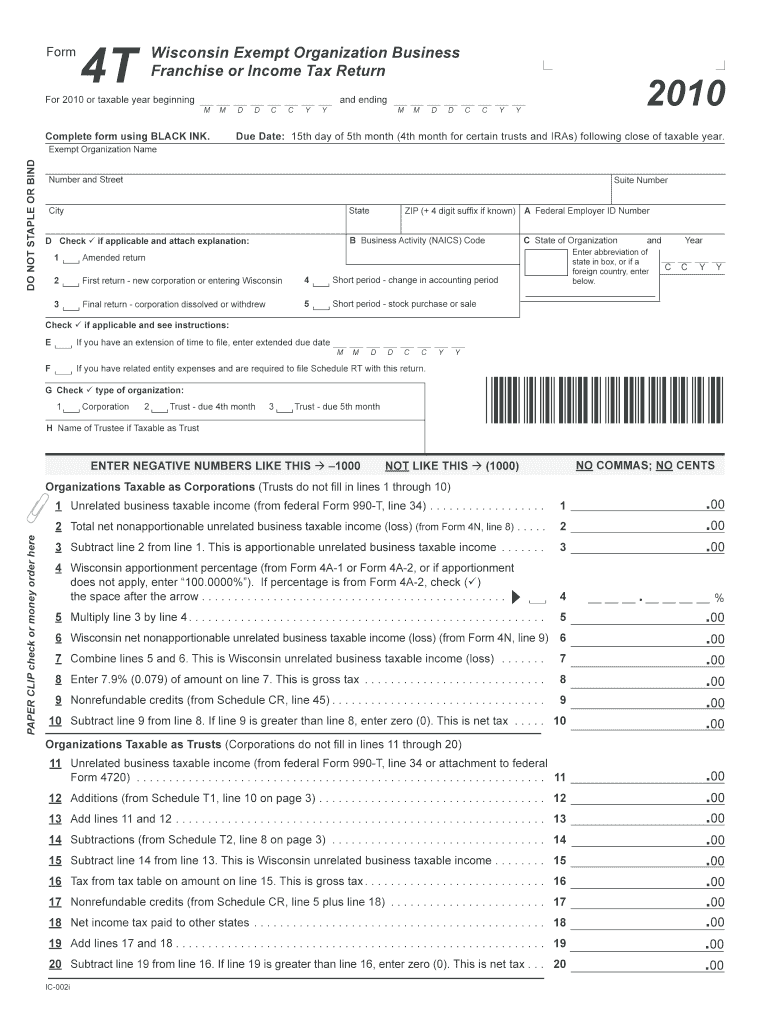

The Wisconsin Form 4T, also known as the Exempt Organization Business Franchise or Income Tax Return, is a specialized tax document used by exempt organizations within Wisconsin. This form is designed to report the organization's unrelated business taxable income. Exempt organizations, such as certain non-profits or religious entities, typically do not pay taxes on their primary functions; however, when they engage in unrelated business ventures, such income becomes subject to taxation through the Form 4T.

How to Use the Wisconsin Form 4T

To effectively use the Wisconsin Form 4T, organizations need to identify any unrelated business activities they participate in. This form requires careful documentation and calculation of any taxable income outside the entity’s primary exempt function. Organizations should gather necessary financial records documenting such activities, as these will be used to accurately compute the tax obligations. Filling out every section of the form correctly ensures compliance with state tax laws and avoids potential penalties.

Steps to Complete the Wisconsin Form 4T

-

Gather Documentation:

- Collect all financial records related to unrelated business activities, including revenues, expenses, and any prior year carryovers.

-

Fill Out Identifying Information:

- Enter the organization’s name, tax year, and federal employer identification number (FEIN).

-

Calculate Income:

- Use provided schedules to determine gross unrelated business income. This includes sections for specific types of income like rents, dividends, and interest.

-

Compute Deductions:

- Deduct applicable expenses related to the business activities to arrive at the unrelated business taxable income (UBTI).

-

Submit and Pay:

- File the completed form with the Wisconsin Department of Revenue. Payment for any taxes due should accompany the return unless electronic methods are used.

Who Typically Uses the Wisconsin Form 4T

The primary users of the Wisconsin Form 4T are tax-exempt organizations such as charities, religious institutions, and certain educational entities. These groups engage in unrelated business activities that require them to report income separate from their primary exempt purposes. Compliance involves having dedicated personnel or a financial advisor knowledgeable in non-profit tax regulations to ensure proper completion and submission of the form.

Important Terms Related to Wisconsin Form 4T

- Unrelated Business Income (UBI): Income earned from activities unrelated to the organization’s primary exempt purpose.

- Exempt Organization: Entities recognized under certain sections of the IRS code that are granted tax exemption privileges.

- Deductions: Allowable expenses that reduce the total amount of UBIT calculated for the tax year.

State-Specific Rules for the Wisconsin Form 4T

Wisconsin state laws detail specific guidelines that differ from federal regulations in handling unrelated business income. Organizations should be aware of state-specific deductions and exemptions that might apply and are encouraged to consult Wisconsin tax publications or a state-qualified tax advisor for clarity. Considerations include specific thresholds for different income types and the impact of state-level tax credits.

Filing Deadlines / Important Dates

The Wisconsin Form 4T must be filed by the 15th day of the 5th month following the end of the taxable year. For organizations using a calendar year, this typically means a due date of May 15. Extensions can be requested, but they do not postpone the payment of any taxes due. Organizations should maintain a calendar to track these deadlines and avoid late submission penalties.

Required Documents

Organizations must prepare specific documents to effectively file the Wisconsin Form 4T:

- Financial statements and ledgers detailing unrelated business revenues and expenses.

- Prior year tax filings and forms if carrying over any losses or credits.

- Copies of any federal tax returns or informational returns related to business activities.

Legal Use of the Wisconsin Form 4T

It's crucial for organizations to understand the legal requirements when using the Wisconsin Form 4T. The document should be used solely to report unrelated business taxable income. Underreporting or failing to file can lead to penalties or loss of tax-exempt status. Transparency and accuracy in reflecting financial engagements are mandatory to adhere to both state and federal tax specifications and maintain the integrity of their exempt status.