Definition & Meaning

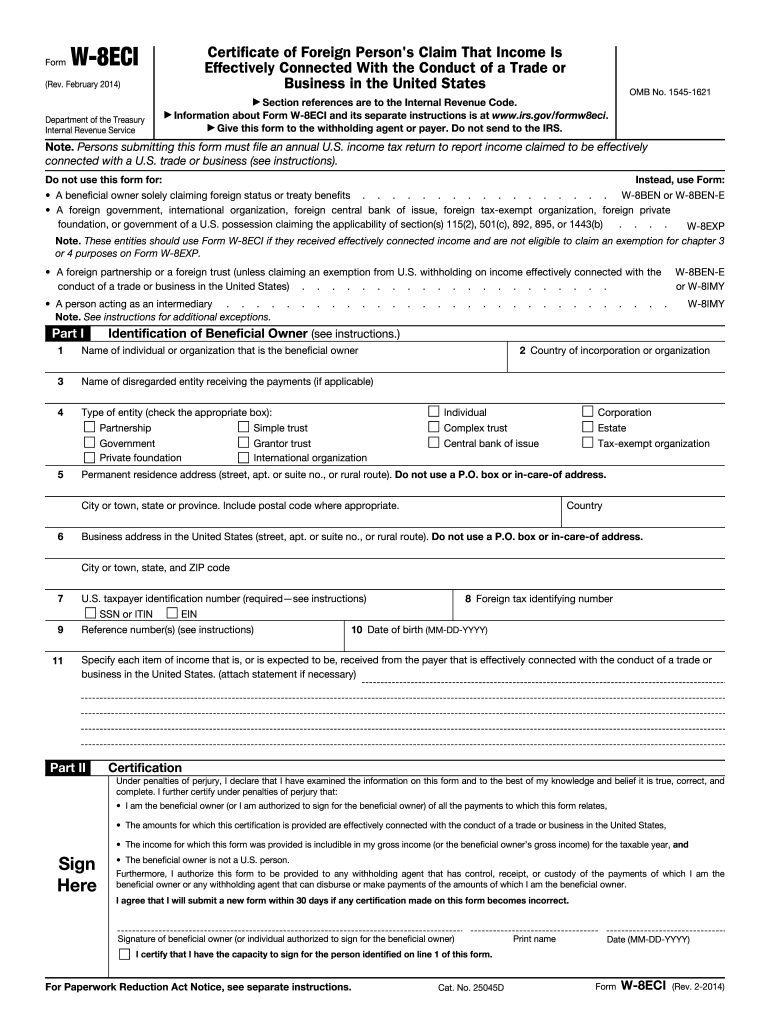

The document titled "Foreign Governments and Certain Other Foreign ... - IRS.gov" is a key tax form used by foreign entities interacting economically with the United States. It specifically applies to foreign governments, international organizations, foreign central banks of issue, and certain other foreign entities seeking to claim relief from U.S. taxation or assert their exemption status under U.S. tax laws. This form is instrumental for these entities in ensuring compliance with IRS regulations, allowing them to accurately report tax-exempt income or income connected to a U.S. trade or business.

How to Use the Form

To accurately use this form, foreign entities must first determine their eligibility for tax exemptions or special conditions under U.S. tax laws. The form facilitates claims regarding income effectively connected with a trade or business in the United States. Users should complete the necessary fields to specify their entity type, the nature of the income, and how it aligns with U.S. tax regulations. The form helps in detailing the specific provisions or articles under U.S. tax treaties that apply, allowing entities to clearly outline why certain tax benefits are applicable to their income.

Steps to Complete the Foreign Governments and Certain Other Foreign Form

- Identify Eligibility: Determine if your entity qualifies under the relevant categories, such as a foreign government or international organization, to use this form.

- Gather Necessary Documents: Collect all required documentation that supports your claims for tax exemption or classification, like official government certificates or organizational charters.

- Complete Identification Sections: Accurately fill out the entity's identification information, which includes the name, address, and identification numbers.

- Detail Income Characteristics: Explicitly state the types of income that your entity receives and how it is connected to a U.S. business operation.

- Cite Relevant Tax Provisions: Clearly cite applicable tax treaty articles or IRS provisions that support the claimed exemptions or statuses.

- Review and Validate Information: Ensure all entered information is correct and complete; errors can delay processing or lead to potential penalties.

Eligibility Criteria

The eligibility to file the "Foreign Governments and Certain Other Foreign ..." form is reserved for foreign governments, international organizations, and other defined foreign entities. Each entity must consistently operate under the guidelines that determine such statuses, often related to diplomatic activities, provision of public services without profit, or operating as a central bank. Detailed eligibility requirements should comply directly with IRS regulations or the relevant tax treaty provisions. Entities must not partake in commercial activities that could disqualify them from tax exemptions based on U.S. tax codes.

Important Terms Related to the Form

Understanding certain terminology is key in effectively completing the form. Terms like "Effectively Connected Income" (ECI) refer to income earned from trade or business connections within the U.S., impacting how you report and claim taxes. "Tax Treaty Benefits" signifies international agreements that allow foreign entities to benefit from reduced tax rates or exemptions, and "Exemption Status" relates to an entity's qualification to avoid certain U.S. taxes altogether. These terms are vital for ensuring proper classification and potential IRS compliance.

Legal Use of the Form

Properly utilizing this form entails adherence to legal intents and procedural accuracy. This means foreign entities must validly demonstrate eligibility for tax report exclusions or claims, based on diplomatic immunity, nonprofit service nature, or similar legal standings. By legally justifying tax exemption claims, entities can prevent disputes with the IRS or other U.S. tax authorities. Misuse or incorrect assertions can result in legal penalties or audits, enforcing the importance of understanding the legal implications tied to this form.

IRS Guidelines

The IRS outlines specific guidelines for the use and submission of this form. They incorporate instructions on how to fill out each section, acceptable documentation, and detailed criteria for exemptions. Compliance with these guidelines involves maintaining accurate records and documentation conducive to IRS audits or verifications. IRS guidelines are designed to assist in avoiding common errors and ensuring that submissions meet reporting standards.

Form Submission Methods

This form can be submitted through multiple channels, reflecting accessibility and convenience. Traditional methods include mail submissions to designated IRS offices, especially for entities that prefer paper trails. However, digital submissions are becoming increasingly acceptable, where online filing systems allow faster and more efficient processing. In-person submissions can also be applicable through consultations with IRS officials or registered tax experts, particularly for entities requiring intricate guidance.

Penalties for Non-Compliance

Failure to comply with the form's submission requirements or inaccurate representation of facts can lead to penalties. These may include financial fines, revocation of tax-exempt status, or legal action from the IRS. Ensuring compliance by meeting deadlines, maintaining accurate records, and truthful representation of entity status is essential for avoiding punitive actions. Regular consultation with tax professionals or legal advisors who specialize in foreign entity taxation can mitigate risks associated with non-compliance.

Key Elements of the Form

The form comprises several key elements that are essential for correct completion. These include identification sections for detailing the entity's name and address, descriptive parts for tax exemption claims, and income characterization fields which succinctly convey the nature and source of income. Each part is crucial as it builds the framework for the IRS to assess taxation eligibility and the legitimacy of claims presented by the foreign entity. Meticulous attention to these elements is required for effective submission.