Definition and Meaning

Understanding the Gifts from Foreign Person document as required by the IRS involves grasping its central purpose. This form, often tied to U.S. tax regulations, is a pivotal tool designed to track gifts received from non-U.S. persons and entities. It assists the Internal Revenue Service in monitoring substantial international financial transfers to ensure compliance with tax obligations. By requiring disclosure of these gifts, the IRS seeks to prevent tax evasion and maintain transparency in cross-border financial activities.

IRS Guidelines

The IRS provides specific guidelines for completing the Gifts from Foreign Person form. These guidelines dictate the conditions under which a gift must be reported, such as the monetary thresholds that trigger the reporting requirement. For cash gifts, the threshold may be as low as $100,000 when received from a foreign individual or estate. This threshold reflects the IRS's intent to capture significant financial gifts that might otherwise go unreported. The IRS also outlines penalties for failing to comply with these reporting requirements, emphasizing the importance of timely and accurate submissions.

Steps to Complete the Gifts from Foreign Person Form

- Gather Information: Collect all relevant details about the gift, including the donor's full name, address, and the gift's total value.

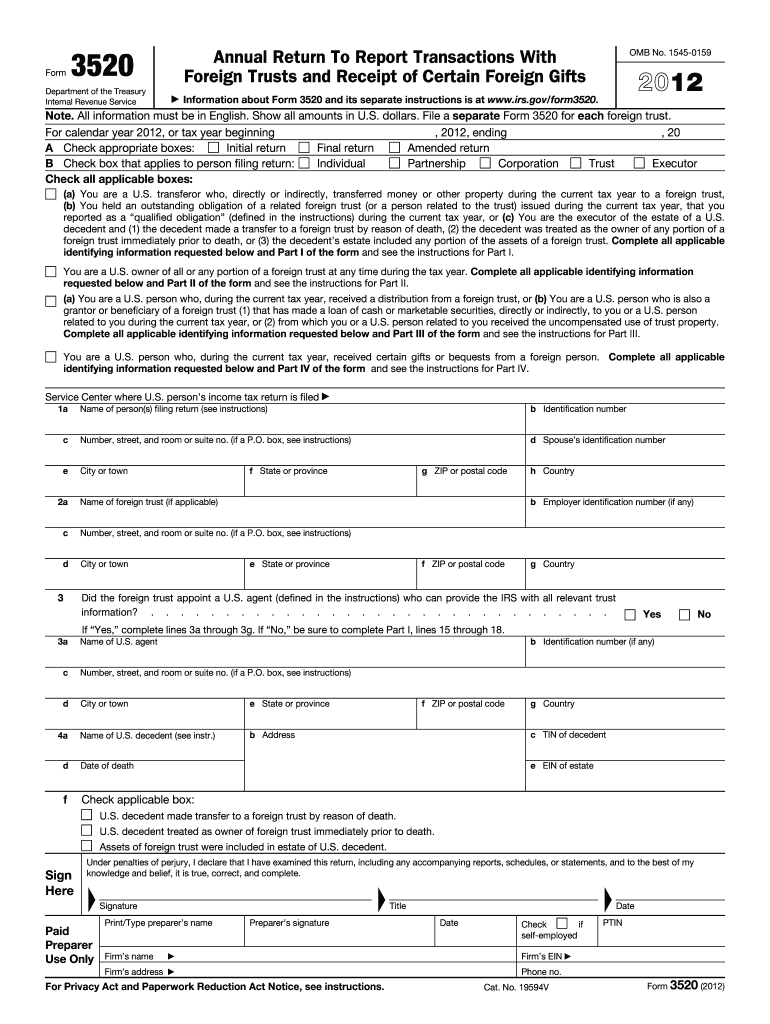

- Consult IRS Instructions: Refer to the IRS's official instructions for Form 3520 to ensure understanding of each section.

- Complete Required Sections: Fill out the necessary sections, including those detailing the nature and value of the gift.

- Review and Verify: Double-check all entered information for accuracy to avoid penalties.

- Submit the Form: File the form by the specified deadline, which is typically the same as your annual tax return deadline.

Important Terms Related to the Form

- Foreign Person: Refers to individuals or entities that are not U.S. residents or citizens, including non-resident aliens and foreign corporations.

- Gift: Any money or asset received from a foreign source without an expectation of repayment.

- IRS Form 3520: The official document used for reporting gifts or bequests from foreign individuals to U.S. taxpayers.

Penalties for Non-Compliance

Failing to report gifts from foreign individuals can result in significant penalties imposed by the IRS. These penalties can be a percentage of the unreported gift's value, potentially reaching 25% in severe cases. The enforcement measures underscore the necessity of adhering to IRS reporting schedules and requirements. Misreporting or late submissions can also trigger additional fees, further emphasizing the importance of comprehensive compliance.

Key Elements of the Form

The form encompasses several critical sections:

- Donor Details: Information about the gift provider.

- Gift Description: A detailed description of the gift, including its value and type.

- Recipient Information: Details of the U.S. person receiving the gift. These elements serve to ensure that the IRS receives a complete picture of the financial exchange and can accurately assess any tax implications.

Filing Deadlines and Important Dates

The deadline for filing the Gifts from Foreign Person form aligns with the taxpayer's annual tax return deadline, typically April 15 of the following year. Extensions can be requested, but late submissions without prior approval can incur penalties. Marking these dates on a calendar and setting reminders can help prevent inadvertent period lapses.

Use in Different Taxpayer Scenarios

Different taxpayers, including those who are self-employed, expatriates, or retirees, might encounter distinct considerations when dealing with foreign gifts. For self-employed individuals receiving gifts, it may affect business finances or asset declarations. Retirees might receive foreign gifts as part of estate planning transactions. Understanding how receipt of a foreign gift impacts one's unique tax situation is vital for accurate financial planning and compliance.

Digital vs. Paper Version

Taxpayers may choose between filing the form electronically or via traditional mail. In many cases, electronic submission offers a faster and arguably more secure method of delivering sensitive information. However, some prefer the tangible comfort of a mailed paper trail. Each method requires specific preparation steps, such as ensuring electronic forms are complete and saved correctly, or that paper versions are mailed well ahead of the filing deadline.