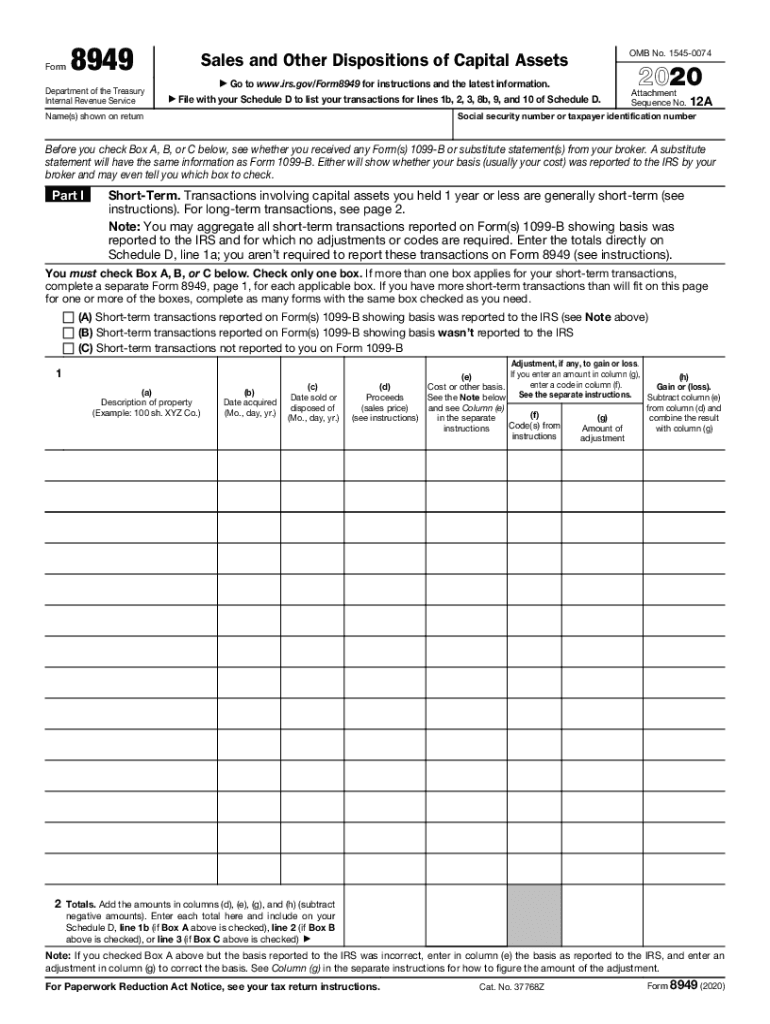

Definition and Meaning of Form 8949

Form 8949, titled "Sales and Other Dispositions of Capital Assets," is an integral tax document used by the IRS. It's designed for reporting capital gains and losses from sales or exchanges of capital assets such as stocks, bonds, and real estate. On this form, taxpayers must detail short-term and long-term transactions, illustrating the nature of their investment activities.

Key Components

- Short-Term vs. Long-Term: Transactions are categorized based on how long an asset was held before disposition.

- Transaction Details: Information such as date acquired, date sold, proceeds, cost basis, and adjustments to gain or loss.

- Box-Ticking Necessity: Taxpayers must indicate whether the basis of the asset was reported to the IRS on a 1099-B form.

How to Obtain the Form 8949

Online Resources

- IRS Website: Form 8949 can be directly downloaded from the IRS's official website. This ensures you have the most updated version.

- Tax Software: Platforms like TurboTax and QuickBooks often provide downloadable forms tailored to individual tax situations.

Physical Copies

- Local IRS Offices: Physical copies can be obtained at IRS offices for those who prefer tangible documents.

- Libraries and Post Offices: Some community locations offer commonly used tax forms during tax season.

Steps to Complete Form 8949

-

Gather Necessary Documents:

- Collect all 1099-B forms and any other documentation related to sales of capital assets.

-

Input Transaction Information:

- For each transaction, fill in details such as description, dates, proceeds, and cost basis.

-

Adjust Gain or Loss:

- Use provided codes and instructions to adjust gains or losses according to specific scenarios.

-

Group and Total Transactions:

- Segregate files by short-term and long-term, summing them separately.

-

Transfer Totals to Schedule D:

- Incorporate the final information from Form 8949 into Schedule D of your tax return.

Who Typically Uses Form 8949

Individual Taxpayers

- Investors: Those who buy and sell stocks, bonds, or ETFs.

- Home Sellers: Individuals disposing of property addresses and private residences.

Businesses and Organizations

- Corporations and LLCs: Entities engaging in capital asset transactions, tracking gains and losses for accurate reporting.

- Partnerships and Trusts: Entities with distributed gains or interests in collectively held assets.

Important Terms Related to Form 8949

- Capital Asset: Any asset held for investment, such as stocks or real estate, not typically a part of normal business inventory.

- Basis: The original purchase price or investment in an asset.

- Adjusted Gain/Loss: The net difference accounting for special items or conditions that affect the raw gain or loss of a transaction.

IRS Guidelines on Form 8949

Reporting Rules

- Transactions must be accurately matched to correct basis status as indicated by the 1099-B.

- Disclosure of the underlying assets, rather than just financial records, is essential for compliance.

Filing Nuances

- Attachments Needed: Attach additional pages if more transactions are present than the form can accommodate.

- Audit Trail: Maintain comprehensive and clear records to substantiate entries on Form 8949.

Examples of Using Form 8949

Case Study: Stock Investment

- An investor sells multiple stocks throughout the year. Each sale needs to have its transaction details, including its nature as short-term or long-term, as well as any specific identifier codes recorded on Form 8949.

Real Estate Sale

- When an individual sells a secondary home, the required information on Form 8949 would include the original purchase price, selling price, and associated fees and improvements affecting the cost basis.

Filing Deadlines for Form 8949

- Standard Deadline: Generally, Form 8949 needs to be filed by April 15 of the tax year, coinciding with the federal tax return deadline.

- Extensions: Taxpayers filing for an extension must still submit Form 8949 with their extended return by October 15.

Required Documents for Filing Form 8949

- 1099-B Forms: Provided by brokers or financial institutions for reporting transactions.

- Receipts and Statements: Documentation supporting the cost basis, sale proceeds, and other transactional elements.

- Prior Year Records: Past Form 8949 filings may be useful for establishing continuity and historical basis records.