Definition and Meaning of Form 211 (Rev 3-2024)

Form 211, officially titled "Application for Award for Original Information," is utilized by individuals aiming to report significant tax violations to the Internal Revenue Service (IRS). The form facilitates the whistleblower process, enabling informants to disclose actionable data that might lead to the recovery of taxes owed to the government. When valid, these disclosures may result in a financial award for the whistleblower, provided that certain IRS criteria are met.

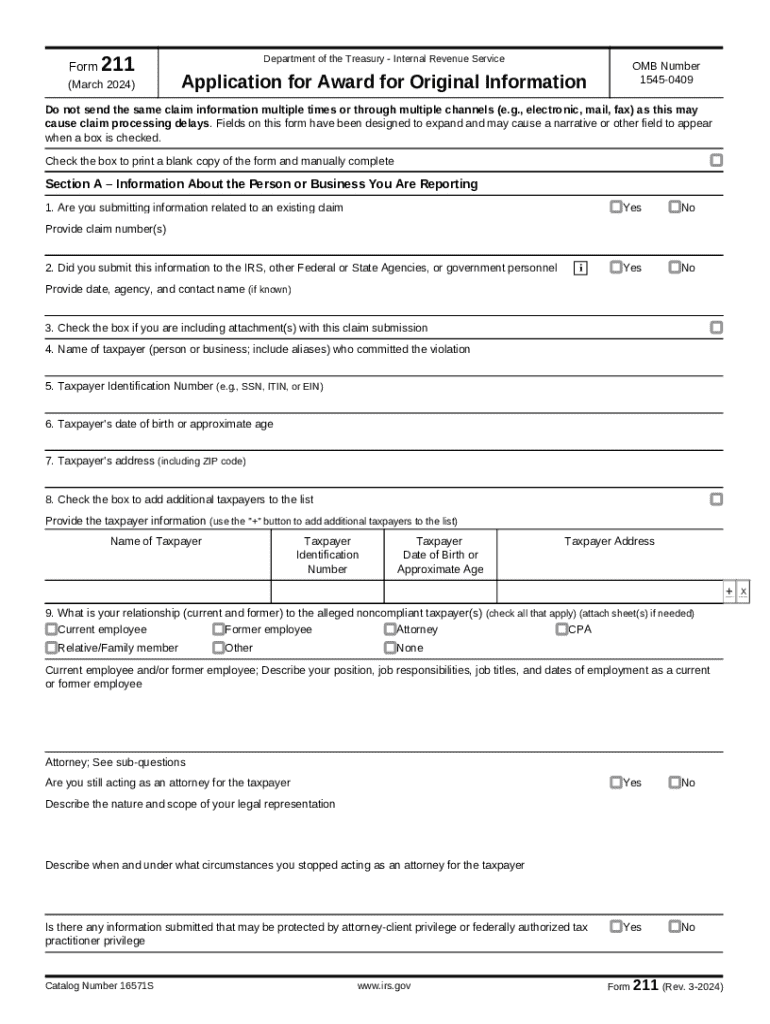

How to Use Form 211 (Rev 3-2024)

To effectively use Form 211, begin by gathering detailed information about the tax violation you intend to report and any evidence that supports your claim. The form requires the completion of various sections, including personal information, specifics of the alleged violation, and details about the taxpayer involved. Adhering to the IRS instructions ensures that the application is completed accurately, which is crucial for safeguarding potential eligibility for an award.

Steps to Complete Form 211 (Rev 3-2024)

-

Enter Personal Information: Include your full name, address, and contact information. This ensures the IRS can reach you if needed.

-

Outline the Violation: Describe the nature of the tax violation in detail. Provide specifics such as the type of violation, the financial impact, and how the information was obtained.

-

Taxpayer Details: Include identifying details about the taxpayer alleged to be in violation—such as their name, address, and taxpayer identification number if known.

-

Evidence Submission: Attach all relevant documents supporting your claim. Evidence might include financial statements, emails, contracts, or other pertinent records.

-

Read and Sign: Thoroughly read the declarations provided and sign the form to affirm the accuracy of your submission.

Important Terms Relating to Form 211

-

Whistleblower: An individual who reports misconduct, commonly related to financial or regulatory noncompliance.

-

Tax Violation: Any breach of IRS tax laws, which can involve evasion, fraud, or underreporting income.

-

Award Percentage: The percentage of collected amounts the whistleblower may receive as a reward, which can differ based on the case’s outcome.

Eligibility Criteria for Using Form 211

Individuals aiming to submit Form 211 must provide original information that can lead to recovering taxes, penalties, and interest. The claimant must comply with all confidentiality rules and should not file duplicate claims, which can invalidate the application. The IRS examines the credibility and relevancy of the provided information to assess eligibility for an award.

Legal Use of Form 211

Submitting Form 211 involves understanding legal implications concerning confidentiality and privilege. It is imperative for informants to ensure that the information provided does not breach any legal obligations or contracts to which they are bound. Legal counsel is often advisable to navigate these complexities, ensuring compliance with IRS regulations and protections afforded to whistleblowers.

Filing Deadlines and Important Dates

There are no specified deadlines for submitting Form 211; however, timely submission is beneficial, especially when cases involve statute limitations on tax audits or collections. Prospective informants are encouraged to submit information promptly to ensure that it is actionable by the IRS within such time constraints.

Form Submission Methods

Form 211 can be filed directly with the IRS by mail. At present, online or electronic filing options are not available for this form. To ensure proper submission, send the completed documents by postal service to the designated IRS office address as instructed in the form’s guidelines. Confirming receipt through certified mail can provide added assurance that the IRS has received your application.

IRS Guidelines for Form 211

The IRS offers specific guidelines for completing Form 211, intending to facilitate a well-structured whistleblower process. These instructions cover how to present the information accurately, ethical considerations, and disclosing all pertinent facts related to any tax violations. Informants are advised to familiarize themselves with these guidelines to maximize the effectiveness of their submission.