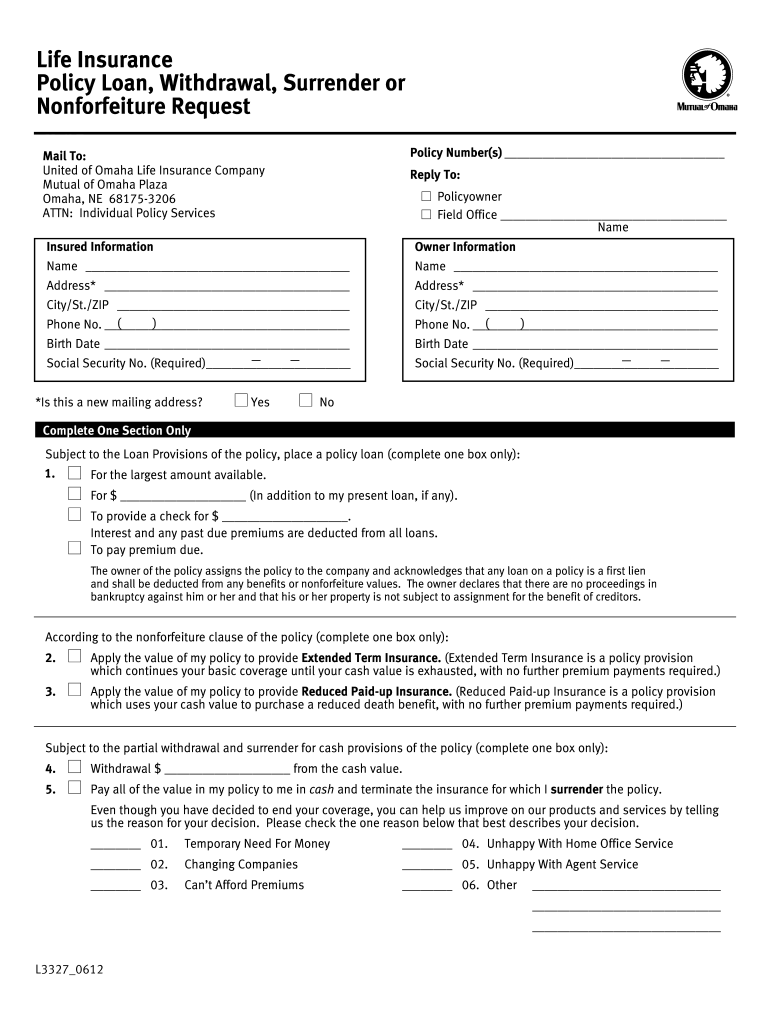

Definition and Purpose of the Mutual of Omaha Surrender Form

The Mutual of Omaha surrender form is a specialized document utilized by policyholders wishing to terminate their life insurance policy and receive the cash value. This form is essential in formalizing the surrender process, ensuring that all legal and procedural requirements are met. The life insurance policyholder must complete it accurately to avoid delays or complications in receiving their entitled benefits. Key components of this form include personal identification details, policy specifics, and necessary authorizations.

Key Components of the Form

- Policyholder Information: This section requires the policy owner's name, address, and contact information, ensuring proper identification.

- Policy Details: It's crucial to provide accurate policy numbers and types, allowing the insurance company to locate the relevant account quickly.

- Surrender Options: The form outlines various options available upon policy surrender, including immediate cash payouts or rollovers into other financial products.

Filling Out the Mutual of Omaha Surrender Form

Properly completing the Mutual of Omaha surrender form involves several steps to ensure accuracy and compliance with policy provisions.

Step-by-Step Instructions

- Gather Required Information: Collect all relevant documents, including the life insurance policy, identification, and any previous correspondence with Mutual of Omaha.

- Complete the Form: Fill in all requested information, ensuring that the details about the policyholder and the policy are correct.

- Choose Surrender Options: Indicate your preferred option for receiving the cash value, such as a lump sum or another financial rollover.

- Review for Accuracy: Before submitting, check for any errors or omissions. Inaccurate information can lead to delays in processing your request.

- Sign and Date the Form: The policyholder must sign and date the document to validate the request officially.

Common Requirements for Surrendering a Policy

Certain prerequisites need fulfillment before submitting a Mutual of Omaha surrender form.

Essential Requirements

- Minimum Policy Duration: Policies often require a minimum period to be in effect before any surrender can occur.

- Outstanding Loans: If there are outstanding loans against the policy, the cash value may be reduced by that amount.

- Verification of Identity: Policyholders may need to provide identification to confirm their identity when submitting the form.

- Review of Beneficiary Designations: Ensure that the beneficiary designations align with the policy surrender, as the value may impact those designations.

Tax Implications of Policy Surrender

Understanding tax implications is crucial when surrendering a policy. Surrenders may affect your tax situation, making it essential to consult a tax advisor.

Key Tax Considerations

- Taxable Gain: The cash value received may be taxable if it exceeds the total premiums paid into the policy.

- Non-Qualified Policies: If the policy is a non-qualified life insurance, any gains could incur income tax liabilities.

- Community Property Laws: Policy surrenders in community property states may require additional consideration of joint ownership and potential taxation.

Additional Considerations when Submitting the Form

Certain factors could influence the surrender of a life insurance policy, and policyholders must take these into account.

Factors to Keep in Mind

- Market Conditions: Assess the current financial market; surrendering may not be beneficial if investment returns are more favorable than the cash surrender option.

- Alternative Solutions: Explore alternatives to surrendering, such as taking a loan against the policy or converting it into a different insurance product.

- Future Financial Needs: Consider long-term financial goals when deciding to surrender a policy, as losing insurance coverage may impact inheritance or final expenses.

Renewing or Converting Policies Instead of Surrendering

For some policyholders, renewing or converting insurance policies may offer more advantageous options than complete surrender.

Considerations for Renewal or Conversion

- Convertible Policies: If eligible, converting a term policy to a permanent one could provide continued coverage without losing benefits.

- Renewal Options: Review renewal terms for continued coverage, potentially at adjusted premiums based on age and health changes.

- Professional Guidance: Consulting with an insurance agent can provide insights into whether renewal or conversion is a more viable option than surrendering.

Conclusion on the Surrender Process

Deciding to surrender a life insurance policy through the Mutual of Omaha surrender form is significant and requires careful consideration. Understanding the necessary steps, tax implications, and alternative options will enable policyholders to make informed decisions to align with their financial goals.