Definition and Meaning of 2012 Forms

2012 forms refer to a variety of documents used primarily in the context of United States taxes and governmental filings that were applicable for the tax year 2012. These include federal income tax forms, state-specific forms, and certain financial disclosures required by the IRS or other regulatory bodies.

Common Types of 2012 Forms

- Form 1040: A comprehensive form used by taxpayers to file their annual income tax return with the IRS. It includes fields for various sources of income, deductions, credits, and tax calculations.

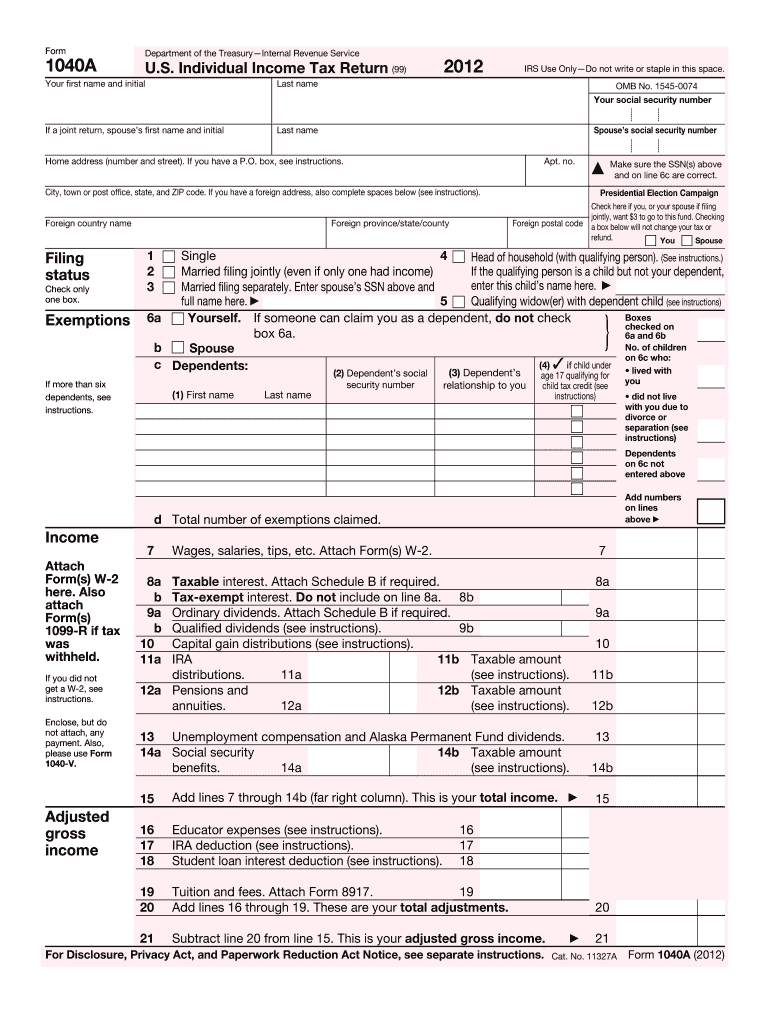

- Form 1040A: A simplified version for individuals with straightforward financial situations, allowing for reporting of income, deductions, and credits without needing the more detailed Form 1040.

- Form W-2: Document provided by employers to employees summarizing earnings and withholdings for the year.

Usage Context

Each form serves distinct purposes, from reporting income tax to documenting employee earnings. They must align with specific IRS instructions tailored for the forms issued in 2012, addressing nuances relevant to that tax year.

How to Use the 2012 Forms

When using 2012 forms, understanding their structure and requirements is crucial for accurate completion and filing.

Key Steps for Utilization

- Identify the Correct Form: Determine the appropriate form based on your financial activities and income sources from 2012.

- Gather Required Information: Collect all necessary documents, such as W-2s, 1099s, and receipts for deductible expenses.

- Follow Form Instructions: Each form includes detailed instructions on how to fill it out, including line-by-line descriptions.

- Calculate Total Income and Deductions: Ensure accurate calculations for total income, allowable deductions, and credits.

Common Mistakes to Avoid

- Errors in arithmetic calculations can lead to inaccuracies.

- Missing documentation can delay processing or result in audits.

- Incorrect filing can result in penalties or interest charges.

Steps to Complete the 2012 Forms

Filing 2012 forms correctly is imperative to ensure compliance and avoid penalties.

Detailed Procedure

- Read Instructions Carefully: Access the IRS form instructions, which provide detailed guidance on each section of the form.

- Fill in Personal Information: Ensure the accuracy of personal information, including name, Social Security number, and filing status.

- Record Income and Deductions: Enter all sources of income and eligible deductions, referencing supporting documentation.

- Double Check Figures: Review all entries and calculations to confirm accurate totals.

- Sign and Date the Form: Ensure the form is signed; an unsigned form is considered incomplete.

- Attach Required Schedules and Statements: Append any additional documentation needed to substantiate entries on the form.

Submission Guidelines

- Electronically: Use e-filing services for prompt submission and acknowledgment.

- Via Mail: If mailing, send to the IRS address specified in the form instructions for 2012.

Who Typically Uses the 2012 Forms

The usage of 2012 forms spans a broad range of filers, but typical users include:

Common User Groups

- Individual Taxpayers: Report personal income, deductions, and credits for the year 2012.

- Business Owners: File corporate taxes or Schedules associated with business income and expenses.

- Retirees: Report any distributions from IRAs or pensions.

Special Considerations

- Students: May file for education-related deductions or credits.

- Self-Employed: Typically use the Schedule C or C-EZ to report business income.

Legal Use of the 2012 Forms

To ensure compliance with IRS regulations, legal use of the 2012 forms is mandatory.

Legal Framework

- Tax Reporting: Forms are used to report taxable income and calculate tax liability under U.S. tax laws for 2012.

- Documentation: Correct completion and timely submission are legally binding, signifying accurate representation of finances.

Legal Penalties

- Failure to File: Results in penalties and interest on unpaid amounts.

- Misrepresentation: Can lead to fines or criminal charges for tax evasion.

Important Terms Related to 2012 Forms

Understanding key terminology is essential for navigating the forms effectively.

Glossary of Terms

- Adjusted Gross Income (AGI): Total income minus specific adjustments; crucial for determining tax liability.

- Credits: Reductions from total tax due, including education or earned income credits.

- Exemptions: Deductions allowed for taxpayers and dependents.

Implications of Terms

- Comprehension of these terms impacts the interpretation of your fiscal responsibilities and opportunities for deductions or credits.

IRS Guidelines for 2012 Forms

The IRS provides comprehensive instructions and guidelines for completing and submitting 2012 forms.

IRS Publications

- Publication 17: Offers an in-depth guide to individual federal income tax, including credits, deductions, and filing statuses.

- Publication 54: Designed for taxpayers living abroad, details income earned outside the United States and its implications.

Updates and Revisions

- Ensure familiarity with any changes or amendments to IRS instructions that could affect filing accuracy for 2012.

Examples of Using the 2012 Forms

Practical examples illustrate common uses and aid in understanding the application of 2012 forms.

Individual Filing Scenarios

- Single Filers: Use Form 1040A for a simpler filing if no itemized deductions are applicable.

- Joint Filers: Married couples can jointly file for combined income and shared deductions.

Business Contexts

- Small Business Owners: Utilize Schedule C for reporting business profits and losses, ensuring deductions for operational expenses are maximized.

These insights into the 2012 forms provide foundational knowledge for any taxpayer or business entity navigating tax filing for the 2012 fiscal year, emphasizing thorough preparation and precision in documentation.