Related links

39-22-109 - Colorado-Source Income | State Regulations

Therefore, a Nonresident individual partner of such a partnership is not subject to Colorado income tax on their distributive share of such partnership income.

Learn more

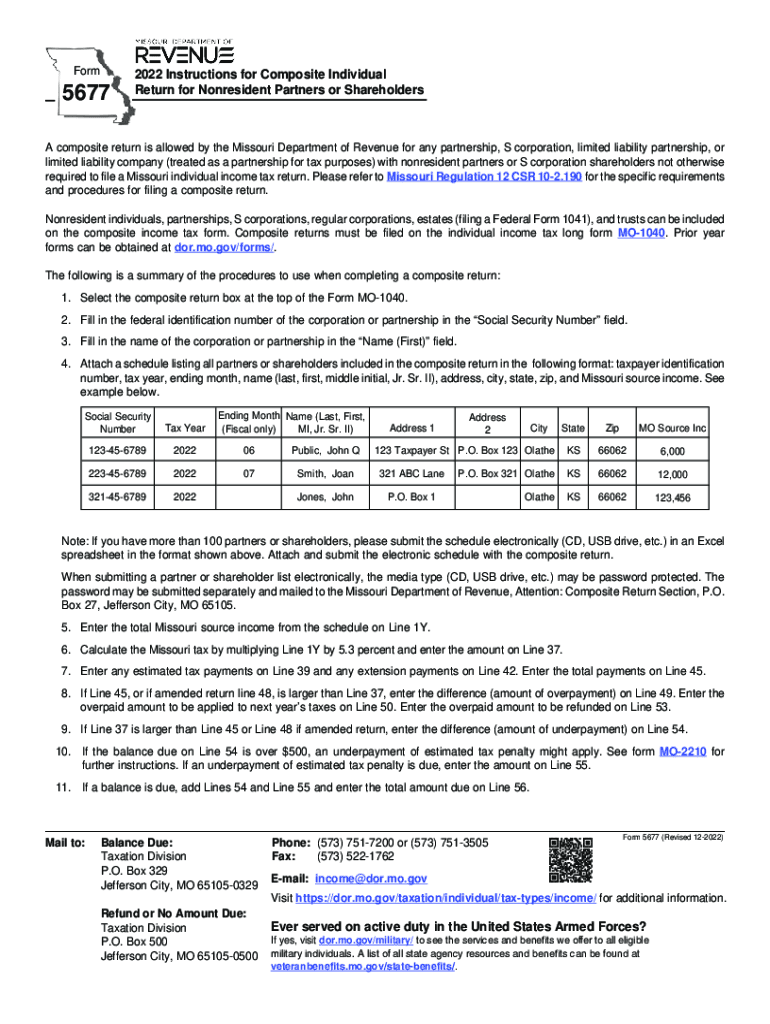

Nonresident Partners Shareholders

A partnership or S corporation may file a composite income tax return for its nonresident partners or shareholders, as a simplified way of paying the income

Learn more

The State of the Colorado River Ecosystem in Grand Canyon

by S Links Library of Congress Cataloging-in-Publication Data. The state of the Colorado River ecosystem in Grand Canyon : a report of the Grand Canyon Monitoring and

Learn more