Related links

New York City Property Taxes and Appeals

by P Marino 2020 Over $28 billion in taxes were collected from New York City property owners in. 2019,1 and for many property owners, real estate taxes are

Learn more

SECURITIES OFFERING REFORM

Jul 19, 2005 A. Communications Requirements Prior to Todays Rules and Amendments. B. Need for Modernization of Communications Requirements.

Learn more

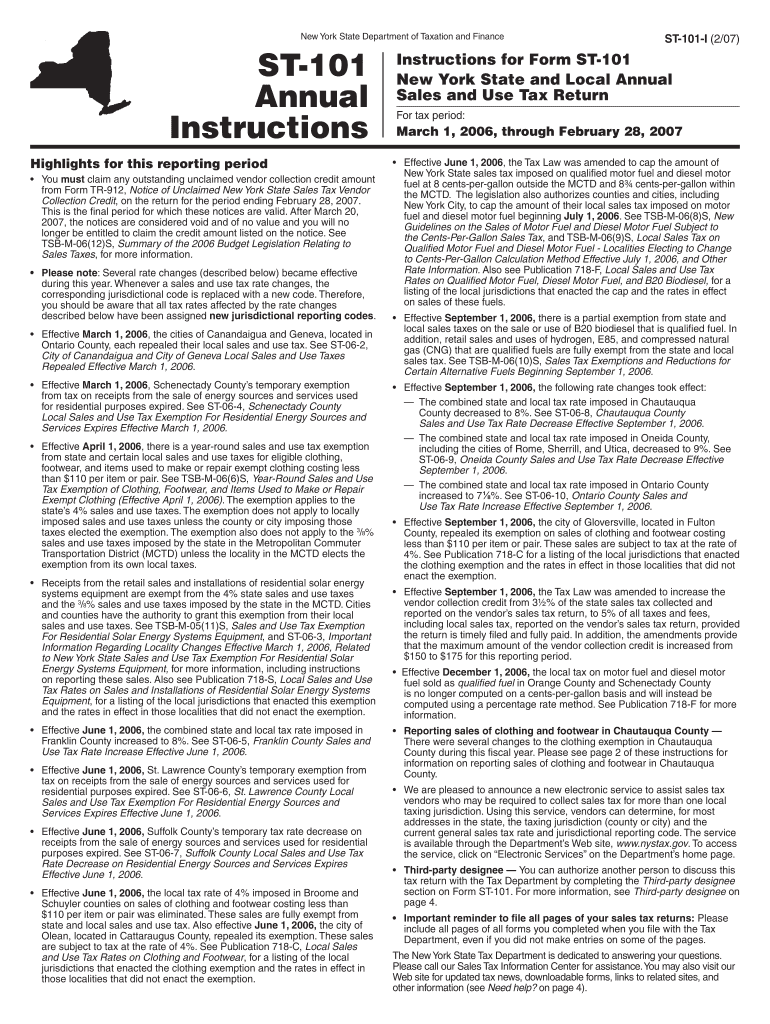

ST-101 Annual Instructions - Tax.NY.gov.

New. Wayne County Effective March 1, 2020, Wayne County repealed their local sales and use tax exemption for clothing and footwear.

Learn more