Definition & Meaning

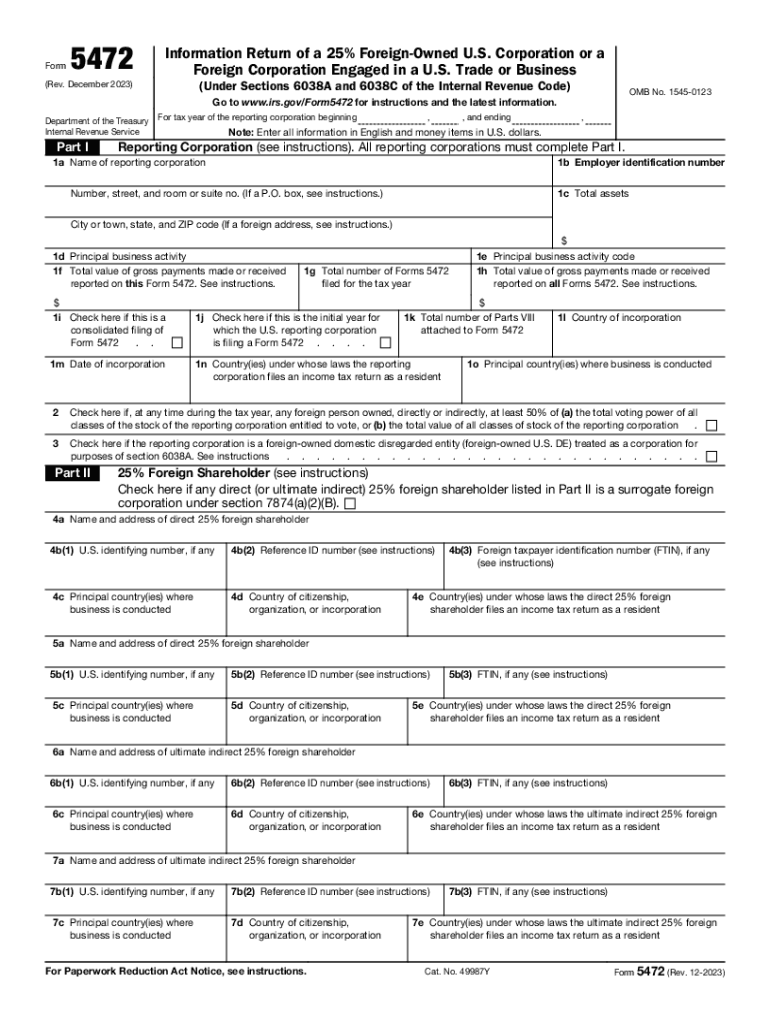

Form 5472 is an informational document mandated by the IRS for U.S. corporations that have at least 25% foreign ownership or for foreign corporations engaged in a U.S. trade or business. The form requires detailed disclosures about financial transactions and ownership structures related to these entities. It is a critical tool used to ensure adherence to tax regulations outlined in Sections 6038A and 6038C of the Internal Revenue Code.

Importance of Accurate Reporting

- Prevents tax evasion by ensuring all substantial foreign transactions are reported.

- Assists IRS in monitoring foreign influence on U.S. enterprises.

- Facilitates transparency in cross-border financial activities.

Key Elements of the Form 5472

Form 5472 encompasses various components that mandate reporting specifics about the corporation’s involvement with foreign entities.

Required Information

- Identification details of the reporting corporation.

- Owner and shareholder information, particularly those with substantial foreign interests.

- Monetary transactions between the corporation and its foreign shareholders or associated parties.

Examples of Transactions

- Sales and purchases of products or services between the U.S. corporation and its foreign affiliates.

- Loans and payments such as royalties, rents, or interest.

Steps to Complete the Form 5472

Filling out Form 5472 accurately is essential for compliance with IRS requirements.

-

Gather Necessary Information:

- Corporate details, including names and addresses of foreign owners.

- Transaction records with related foreign parties during the tax year.

-

Complete the Form:

- Fill in parts detailing financial dealings, including specific transaction descriptions and monetary values.

-

Review for Accuracy:

- Double-check all entries to avoid errors that may trigger penalties.

-

Submit with Form 1120 or 1120-F:

- Typically, Form 5472 should be submitted alongside the corporation's annual tax return.

Filing Deadlines / Important Dates

Form 5472 should align with the filing schedule of the corporation's tax return, generally due on the 15th day of the fourth month after the corporation's financial year ends.

Extensions

- An automatic extension can be obtained by filing Form 7004, extending deadline alignment with extended tax return dates.

Penalties for Non-Compliance

Failure to file Form 5472 timely or accurately can lead to significant penalties.

Consequences

- Minimum penalty of $25,000 for each required form that is not filed by the due date.

- Additional penalties can accrue for continued non-compliance.

Who Typically Uses the Form 5472

The form is predominantly used by:

Eligible Corporations

- U.S. corporations with foreign shareholdings exceeding 25%.

- Foreign corporations conducting active business operations within the U.S.

Business Entity Types (LLC, Corp, Partnership)

Different business structures may have varied requirements regarding Form 5472.

Corporations

- Most common filers due to direct implications of foreign ownership.

Partnerships and LLCs

- Generally exempt unless structured in a specific manner engaging substantial foreign interest reporting criteria.

IRS Guidelines

IRS guidelines for Form 5472 provide critical instructions to ensure compliance.

Compliance Tips

- Thorough record-keeping to substantiate all reported transactions.

- Regular updates on IRS changes to Form 5472 requirements and procedures.

How to Obtain the Form 5472

Accessing Form 5472 can be done through various methods:

Online Access

- Download directly from the IRS website or utilize authorized tax preparation software platforms.

Physical Copies

- Order from the IRS by requesting a mailed version if digital access is not feasible.

Examples of Using the Form 5472

Examples of situations necessitating Form 5472:

- U.S. Retail Chain with Foreign Parent Corporation: Transactions involving international sourcing and service payments documented annually.

- Manufacturing Firm with Foreign Subsidiaries: Recording cross-border sales and licensing agreements.