Type text, add images, blackout confidential details, add comments, highlights and more.

02. Sign it in a few clicks

Draw your signature, type it, upload its image, or use your mobile device as a signature pad.

03. Share your form with others

Send it via email, link, or fax. You can also download it, export it or print it out.

How to use or fill out 2019 W-011 Form WT-11 Nonresident Entertainer Withholding Report with DocHub

Ease of Setup

DocHub User Ratings on G2

Ease of Use

DocHub User Ratings on G2

Click ‘Get Form’ to open the 2019 W-011 Form WT-11 in our editor.

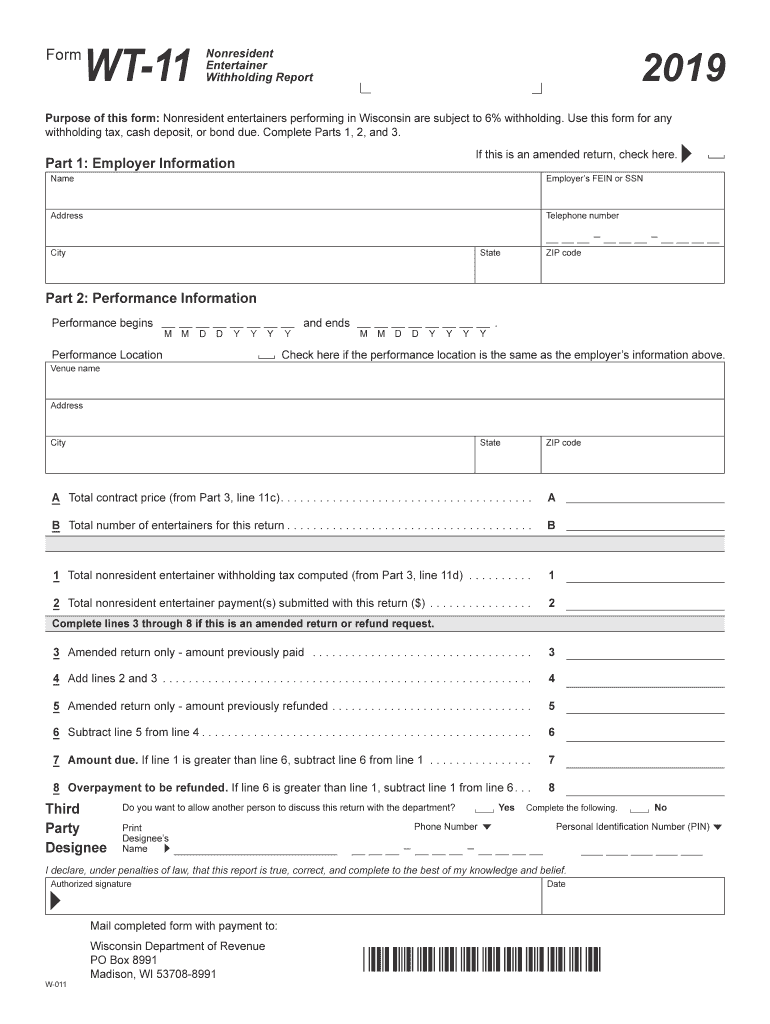

Begin with Part 1: Employer Information. Fill in the employer's name, FEIN or SSN, address, telephone number, city, state, and ZIP code.

Proceed to Part 2: Performance Information. Enter the performance start and end dates, venue name, and address. If the performance location matches the employer's information, check the corresponding box.

Complete the financial details by filling in total contract price and total number of entertainers for this return. Ensure you accurately compute withholding tax based on provided guidelines.

In Part 3: Nonresident Entertainer Information, provide details for each entertainer including stage name, legal name, FEIN/SSN, and whether withholding is required.

Review all entries for accuracy before saving your completed form. Use our platform’s features to sign and distribute your document as needed.

Start using our editor today to fill out your forms online for free!

Fill out 2019 W-011 Form WT-11 Nonresident Entertainer Withholding Report online It's free

See more 2019 W-011 Form WT-11 Nonresident Entertainer Withholding Report versions

We've got more versions of the 2019 W-011 Form WT-11 Nonresident Entertainer Withholding Report form. Select the right 2019 W-011 Form WT-11 Nonresident Entertainer Withholding Report version from the list and start editing it straight away!

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.