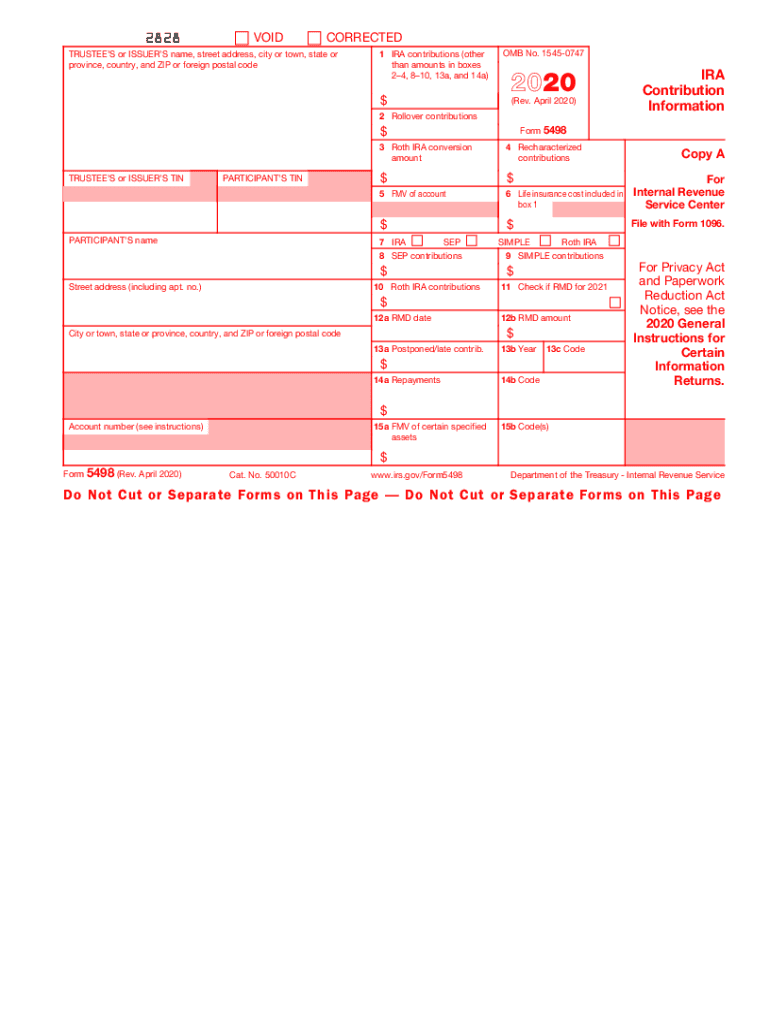

Definition and Purpose of Form 5498

Form 5498 is a tax document used by financial institutions to report contributions to individual retirement arrangements (IRAs) to the Internal Revenue Service (IRS). This form plays a vital role in tracking contributions, rollovers, conversions, and required minimum distributions (RMDs) for all IRA accounts. Each type of contribution or rollover has specific coding to ensure accurate reporting, making it an essential component of tax preparation and compliance for both IRA account holders and their trustees.

Key Elements of Form 5498

- IRA Contribution Information: This section captures details about regular contributions, including the total amount contributed to traditional, Roth, SEP, or SIMPLE IRAs.

- Rollover Contributions: Information about rollovers from other retirement plans, such as 401(k)s, into an IRA, ensuring correct tax treatment.

- Fair Market Value (FMV): The FMV of the IRA at the end of the year, crucial for calculating RMDs for participants aged 72 or older.

- Recharacterizations: Any fund recharacterizations must be reported, involving the transfer of funds between traditional and Roth IRAs under certain conditions.

Steps to Complete Form 5498

- Gather Necessary Documentation: Ensure all transaction records, contribution amounts, and rollover details are available.

- Enter Participant Information: Fill in the IRA holder’s name, address, and taxpayer identification number (TIN).

- Report Contributions and Rollovers: Accurately enter data for all contributions and rollovers throughout the year.

- Calculate FMV: Compute the IRA's FMV as of December 31. This provides the basis for determining RMDs.

- Validation and Verification: Double-check all entries for accuracy before submission to the IRS.

How to Use Form 5498

Form 5498 is primarily used to validate the contributions made to IRAs and to ensure that individuals comply with IRS regulations concerning retirement accounts. IRA account holders should review this form carefully each year to confirm their contributions and investment choices are accurately reported. It is important for them to retain Form 5498 for their records and use its data when preparing their personal federal and state tax returns. This form is sent to both the individual and the IRS; however, individuals do not need to file it with their tax return.

How to Obtain Form 5498

IRA custodians, such as banks or other financial institutions, are responsible for issuing Form 5498. It is typically sent to IRA holders by May 31 of each year. Account holders can expect to receive it via mail, or they can access it through their financial institution’s online platform if they have opted for electronic delivery. If a taxpayer does not receive the form, they should contact their financial institution to request a copy.

Who Typically Uses Form 5498

Form 5498 is used both by individuals who own an IRA and by the financial institutions that manage these accounts. Account holders need to reference this document to verify contributions and ensure they comply with IRS rules. IRS uses this form to monitor contributions, rollovers, and RMDs, ensuring individuals do not exceed contribution limits or neglect to take mandatory distributions.

Example of Using Form 5498

Consider a taxpayer who has both a traditional and a Roth IRA. He contributes to both annually and transfers funds from his employer's 401(k) into his traditional IRA. Form 5498 will report all these transactions, allowing him to verify accuracy and address any discrepancies with his financial institution before using the information to prepare his tax return.

IRS Guidelines and Compliance

The IRS guidelines for Form 5498 establish comprehensive rules for reporting all types of IRA contributions, distributions, and account values. Financial institutions must submit this information accurately by the deadline to the IRS and provide copies to account holders. Non-compliance, such as failure to file or errors in the reported information, can result in penalties for both financial institutions and individuals.

Filing Deadlines and Important Dates

The critical filing deadline for Form 5498 is May 31, the date by which financial institutions must furnish a copy to the taxpayer and file with the IRS. Any contributions made to an IRA between January 1 and April 15 that are designated for the previous tax year must also be included. The extended deadline accommodates the tax filing season for individuals, allowing ample time to report accurate figures.

Required Documents for Completing Form 5498

When filling out Form 5498, financial institutions require detailed transaction histories of contributions, rollovers, and conversions made into IRAs. This includes documentation supporting FMV calculations for the year-end. Account holders should keep copies of contribution confirmations, rollover notices, and financial statements that show year-end values.

Software Compatibility and Electronic Filing

While Form 5498 is primarily distributed by financial institutions, tax software like TurboTax or QuickBooks can simplify tracking IRA contributions by integrating its data. Such software helps individuals manage tax filings by pulling information directly from financial institutions when authorized, ensuring that all reports are accurate and comprehensive.

Penalties for Non-Compliance

Failure to accurately complete Form 5498 or submit it to the IRS on time can result in penalties for financial institutions. These penalties can be significant and also apply if the form is not delivered to the IRA account holder. Financial entities must adhere strictly to IRS guidelines to avoid these penalties, reinforcing the importance of accuracy and timely reporting.

Digital vs. Paper Version of Form 5498

Because of the growing importance of digital documentation, many financial institutions offer the option to receive Form 5498 electronically. This approach allows for faster delivery, easy archiving, and a reduction in physical paperwork. Account holders should ensure that they maintain both digital and paper copies of the form for their records, regardless of their delivery preference.

Conclusion

Form 5498 serves as a comprehensive report on IRA contributions and related transactions, significantly aiding individuals in retirement planning and tax compliance. Financial institutions must ensure accurate completion and timely submission of this form to both the IRS and the account holder to avoid penalties and uphold the integrity of retirement account reporting.