Definition and Meaning

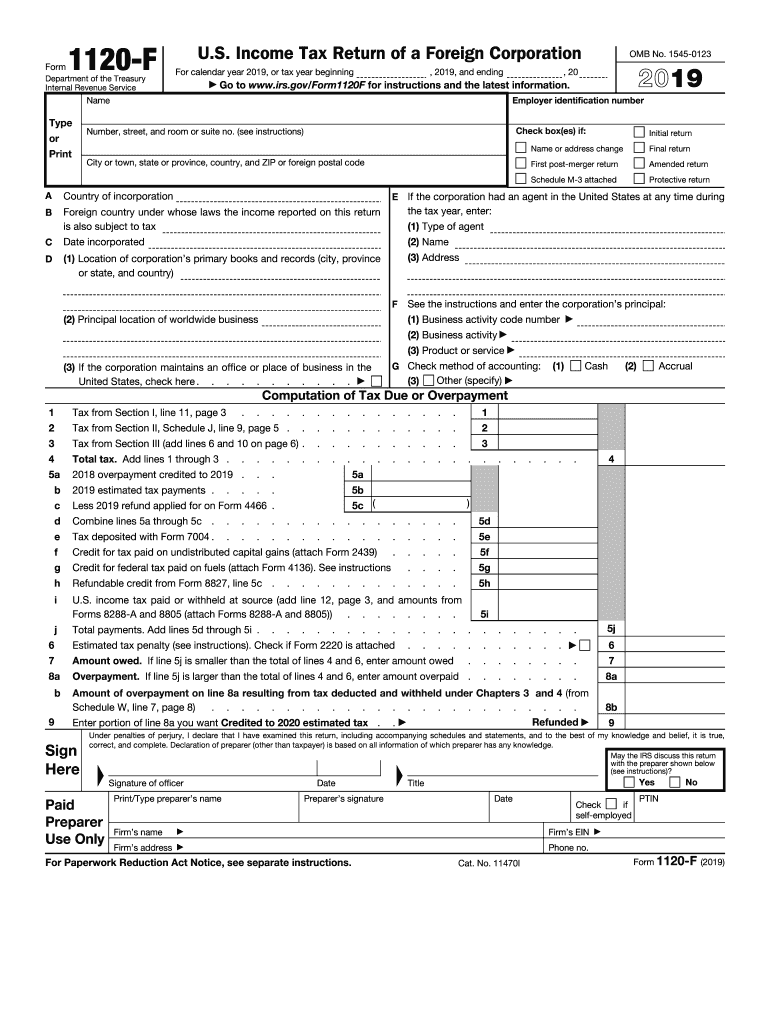

Form 1120-F, officially known as the U.S. Income Tax Return of a Foreign Corporation, serves as an essential tax form for foreign corporations conducting business in the United States. These corporations are required to report their U.S. income, expenses, and tax liabilities using this form. The primary purpose of the form is to account for income effectively connected with the conduct of a trade or business in the U.S. and income sourced from U.S. operations. Providing detailed sections for income, deductions, and branch taxes, the form guides corporations in meeting tax obligations efficiently while ensuring compliance with U.S. tax laws.

Key Elements of Form 1120-F

The structure of Form 1120-F includes several critical elements that need comprehensive attention:

- Income Reporting: Corporations report all types of income, including gross receipts, sales, dividends, interest, and royalties, broadly categorized in sections for effectively connected income and non-effectively connected income.

- Deductions and Credits: This includes applicable business expenses that are deductible, such as wages, rent, and office supplies, alongside crucial credits like foreign tax credits that contribute to lowering the U.S. tax liability.

- Branch Profits Tax: Foreign corporations are subject to an additional 30% tax on any withdrawal of U.S. profits not reinvested back into U.S. operations, though some treaties may mitigate this rate.

- Balance Sheets and Schedules: Precise disclosures of the corporation's balance sheet data, including assets, liabilities, and shareholder equity, are required, providing a snapshot of financial health.

Steps to Complete Form 1120-F

Completing Form 1120-F effectively demands adherence to several critical steps:

- Gather Required Documentation: Obtain all necessary financial records, such as income statements, balance sheets, and documentation of U.S. business activities.

- Determine Taxable Income: Accurately calculate both effectively connected income and U.S. source income under existing tax regulations.

- Calculate Deductions and Credits: Identify allowable deductions and calculate foreign taxes that may qualify for credits to reduce tax obligations.

- Fill Out Business Information: Complete section identifying the corporation, including name, address, EIN, and NAICS code to classify its primary business activity.

- Prepare Balance Sheet: Accurately document assets, liabilities, and equity as per the reporting requirements at the close of the tax year.

- Verify and Validate Information: Thoroughly review each section for completeness and accuracy before submission.

How to Obtain Form 1120-F

Corporations can access Form 1120-F through various methods:

- IRS Website: The form is available for download on the IRS official website, allowing for immediate access.

- Tax Preparation Software: Many tax software solutions, such as TurboTax or QuickBooks, include this form, offering easy integration into the overall tax preparation process.

- Tax Professional Services: Many accounting firms keep physical copies and can provide assistance in obtaining and completing the form.

Important Terms Related to Form 1120-F

Understanding specific jargon is crucial for navigating Form 1120-F:

- Effectively Connected Income (ECI): Income directly linked to a U.S. business operation, often taxed on a net basis after allowable deductions.

- Branch Profits Tax (BPT): An additional U.S. tax imposed on foreign corporations withdrawing profits from their U.S. operations.

- Source of Income: The origin of income based on geographical or operational derivations, distinguishing between U.S. and foreign sources.

IRS Guidelines

The IRS provides comprehensive guidelines on how to manage Form 1120-F filings:

- Filing Thresholds: Corporations must meet certain income thresholds to file and should review IRS publications for specifics.

- Regulations on Deductions: Detailed policies define permissible deductions and emphasize keeping thorough documentation to substantiate claims.

- Treaty Benefits: Instructions incorporate claiming treaty-based tax rate reductions, requiring a careful analysis of applicable treaty stipulations in IRS publications.

Filing Deadlines and Important Dates

Foreign corporations need to carefully note the deadlines associated with Form 1120-F:

- Annual Filing: Generally due 15 days following the 6th month after the close of the taxable year, distinct from typical domestic filing timelines.

- Extension Requests: Extensions can be filed using Form 7004, granting up to six additional months if approved by the IRS.

Penalties for Non-Compliance

Failure to comply with the requirements of Form 1120-F can lead to significant penalties:

- Late Filing Fees: Corporations face financial penalties for overdue submissions, with potential interest accruing on unpaid taxes.

- Accuracy-Related Penalties: Inaccuracies or fraud lead to substantial fines, underscoring the importance of ensuring accurate and truthful reporting.

- Withholding Missteps: Failure to adhere to withholding regulations on U.S. source income, especially related to treaty benefits, entails further governmental penalties.