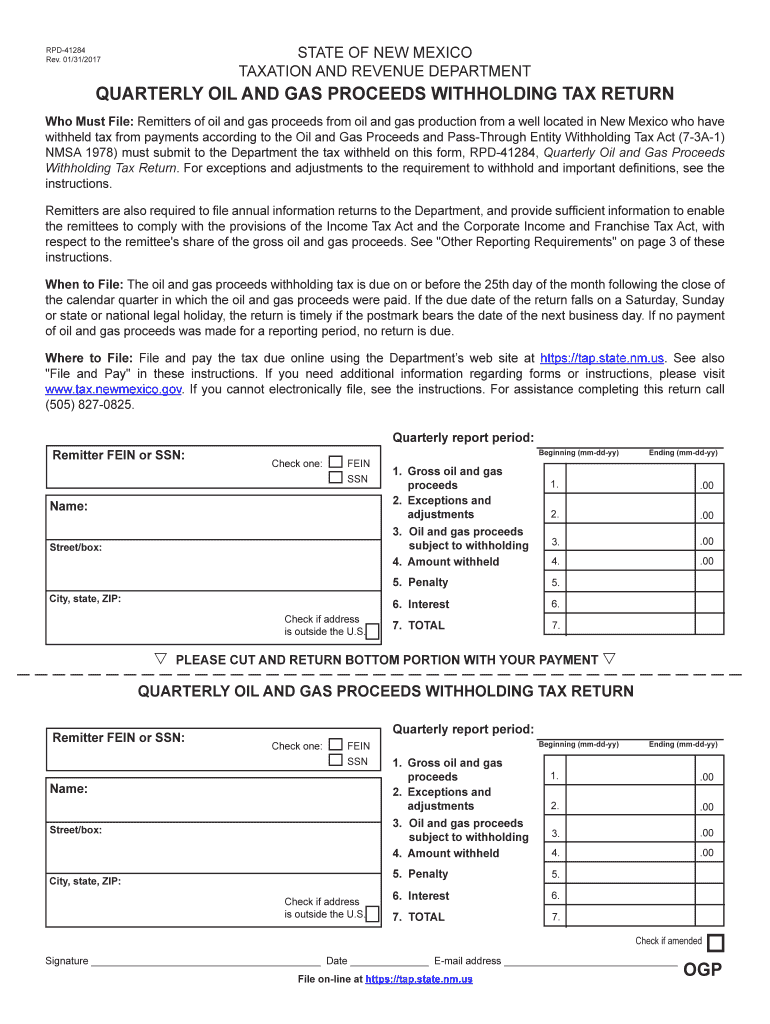

rpd 41284

Form 1065 - U.S. Return of Partnership Income

Information Statement of Section 1446 Withholding Tax, filed for this partnership. d Oil, gas, and geothermal propertiesgross income .

Learn more

26 U.S. Code 1446 - Withholding of tax on foreign partners

The partnership shall be allowed a deduction for depletion with respect to oil and gas wells but the amount of such deduction shall be determined without regard

Learn more

Oil Gas Severance Tax | Withholding Information

This form lists your gross income which you must use to calculate your severance tax and the amount the producer has withheld and paid to the state.

Learn more