it 182

Tax Symposium: Passive Activity Losses and Credits

by LD Bailey 1988 In making this computation, a taxpayer should recognize that net portfolio income or loss is not treated as income or loss from a passive activity. Also, the

Learn more

Indoor Air Vapor Intrusion Mitigation Approaches

If passive techniques are insufficient to limit risk or haz- ard, more active techniques may be used to prevent the entry of vapor contaminants into a building.

Learn more

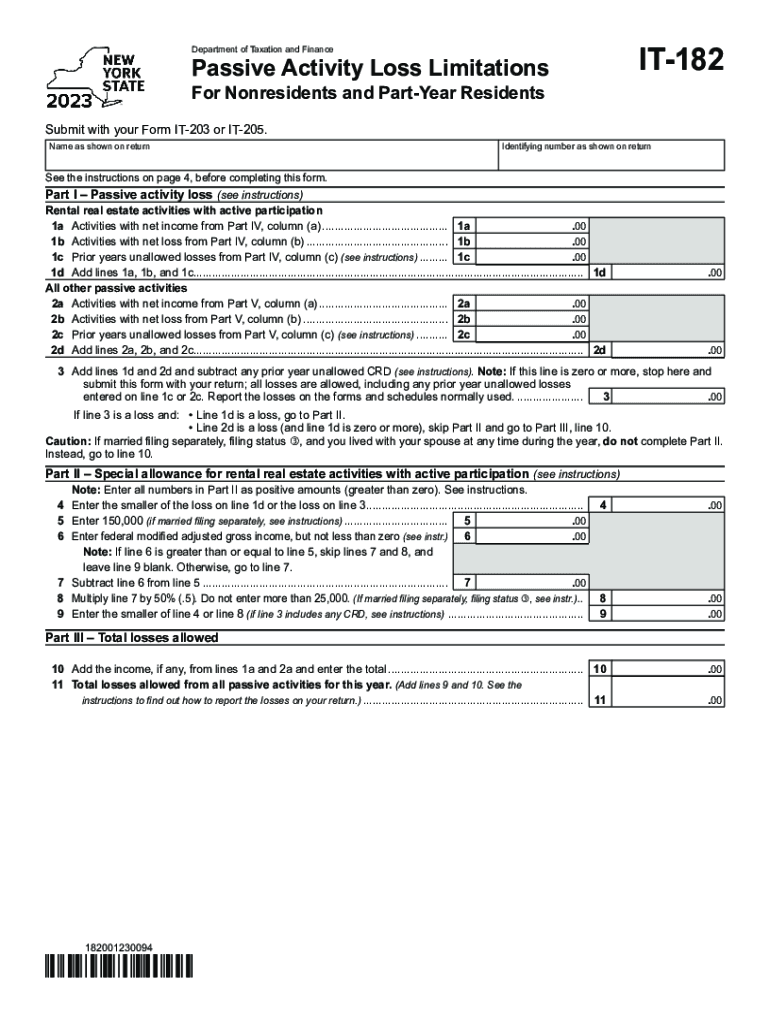

Form IT-182 Passive Activity Loss Limitations Tax Year 2024

Form IT-182, Passive Activity Loss Limitations, to report the amount of allowed passive activity losses from New York sources for the current tax year. It

Learn more